Please answer all the questions

The questions:

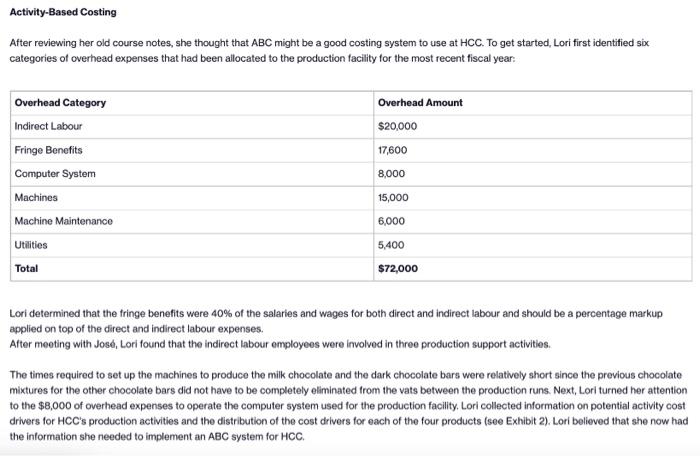

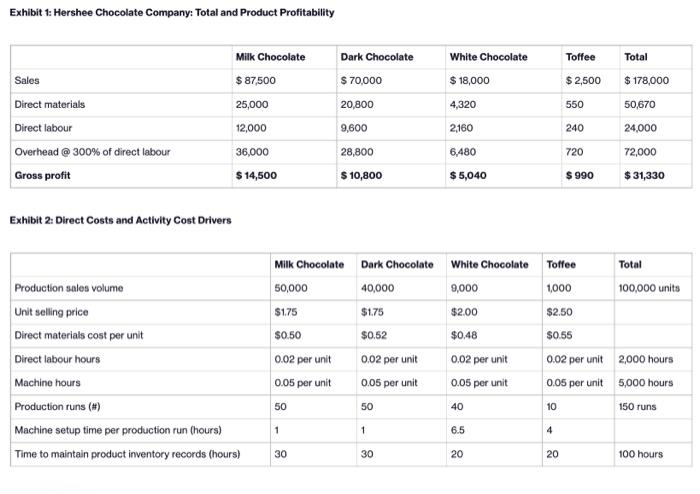

Lori Hershee, controller of her family's business, Hershee Chocolate Company (HCC), was concerned about the financial results for the most recent fiscal year. For years, HCC focused on producing only two products: milk chocolate bars and dark chocolate bars. The white chocolate bars could be sold at higher prices compared to the milk chocolate and dark chocolate bars. Lori had reviewed the most recent financial results and was disappointed. While the white chocolate and toffee bars seemed to be more profitable than the two original chocolate bars, the company's overall profitability was down. Jos Gonzalez, the production manager, had approached Lori concerned with the current state of the production facilities. Production of the white chocolate bars required the production employees to have to stop production, empty the vats of chocolate from the previous production runs, thoroughly clean the vats, and then start the production of the white chocolate bars. The recent addition of the toffee bars to the product line added further demands on production, with additional setups and longer setup times required because of the toffee centres that also had to be added. HCC produced all of its chocolate bars in a single production facility. Each product had a bil of materials that identified the quantity and cost of direct materials required. This information was used to calculate the direct labour expenses for each of the four products. All of the production facility's indirect expenses were aggregated at the production facility level and allocated to each product based on their direct labour expenses. Currently, the overhead rate was 300% of direct labour expenses. Prior to the introduction of the white chocolate and toffee bars, the overhead rate was only 200%. After reviewing her old course notes, she thought that ABC might be a good costing system to use at HCC. To get started, Lori first identified six categories of overhead expenses that had been allocated to the production facility for the most recent fiscal year: Lori determined that the fringe benefits were 40% of the salaries and wages for both direct and indirect labour and should be a percentage markup applied on top of the direct and indirect labour expenses. After meeting with Jose, Lori found that the indirect labour employees were imvolved in three production support activities. The times required to set up the machines to produce the milk chocolate and the dark chocolate bars were relatively short since the provious chocolate mixtures for the other chocolate bars did not have to be completely eliminated from the vats between the production runs. Next, Lori turned her attention to the $8,000 of overhead expenses to operate the computer system used for the production facility. Lori collected information on potential activity cost drivers for HCC's production activities and the distribution of the cost drivers for each of the four products (see Exhibit 2). Lori believed that she now had the information she needed to implement an ABC system for HCC. Exhibit 1: Hershee Chocolate Company: Total and Product Profitability Exhibit 2: Direct Costs and Activity Cost Drivers Answer all of the following questions: As part of the HCC accounting team, Lori has asked you to complete the following tasks: 1. Discuss the current costing practices used by HCC to allocate overhead costs to each of the four products, including whether it is an appropriate costing method now that HCC has increased the number of different chocolate bars. [0.5 marks] 2. Determine the activity cost rate for each of the four production activities (i.e., scheduling and supporting the production runs, machine setups, maintaining product inventory records, and running the machines), based on the overhead resources that each activity consumes. Provide the four activity costs separately and include their detailed calculations to show your intermediary steps (in particular, the volumes of the four activity cost drivers). [2 marks] 3. Revise HCC's Total and Product Profitability statement presented in Exhibit 1 using the new ABC system. In your revised profitability statement, make sure to include separate line items for each of the overhead activity costs allocated to oach product. [2 marks] 4. Calculate the gross profit margin (in % ) for each product under the current costing system and the ABC system. Comment on the profitability of each chocolate bar under the ABC system and how it differs from the current gross profit margin (in % ). [1.5 marks]