Answered step by step

Verified Expert Solution

Question

1 Approved Answer

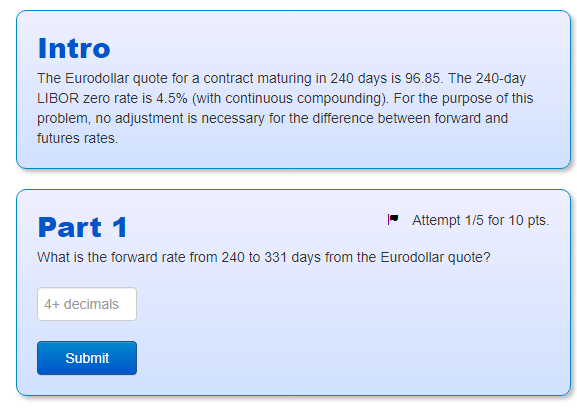

please answer carefully people got it wrong often. thanks :) Intro The Eurodollar quote for a contract maturing in 240 days is 96.85 . The

please answer carefully people got it wrong often. thanks :)

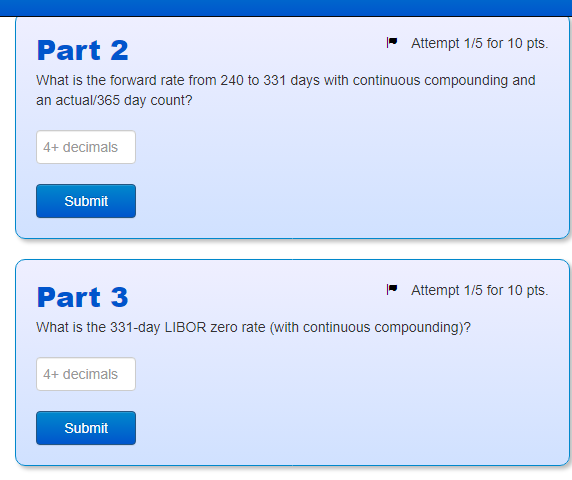

Intro The Eurodollar quote for a contract maturing in 240 days is 96.85 . The 240-day LIBOR zero rate is 4.5% (with continuous compounding). For the purpose of this problem, no adjustment is necessary for the difference between forward and futures rates. Part 1 - Attempt 1/5 for 10 pts. What is the forward rate from 240 to 331 days from the Eurodollar quote? What is the forward rate from 240 to 331 days with continuous compounding and an actual/365 day count? Part 3 Attempt 1/5 for 10pts. What is the 331-day LIBOR zero rate (with continuous compounding)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The AMA Handbook Of Financial Risk Management

Authors: John J. Hampton

1st Edition

0814417442, 978-0814417447