Please answer please

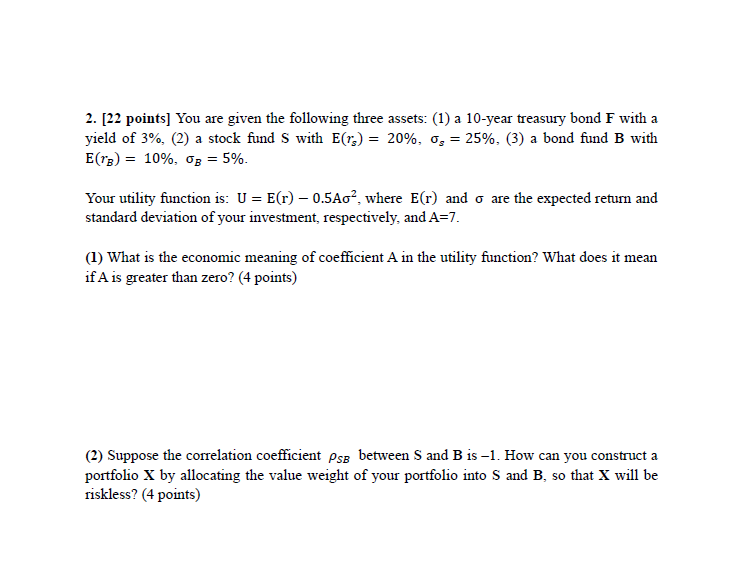

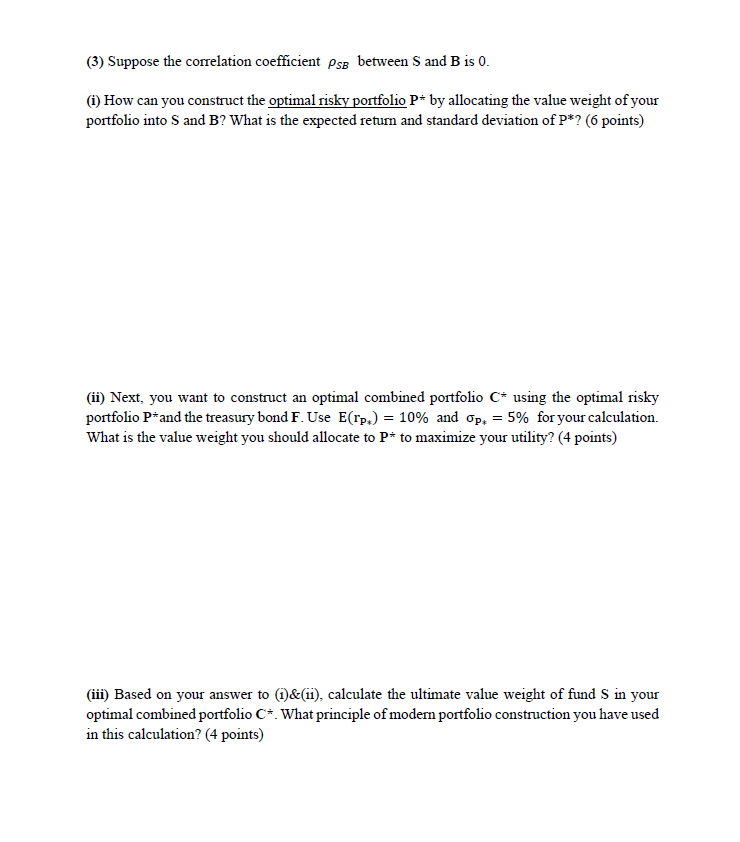

2. [22 points] You are given the following three assets: (1) a 10-year treasury bond F with a yield of 3%, (2) a stock fund S with E(rs) = 20%, 03 = 25%, (3) a bond fund B with E(rs) = 10%, og = 5%. Your utility function is: U = E(r) 0.5A0, where E(r) and o are the expected return and standard deviation of your investment, respectively, and A=7. (1) What is the economic meaning of coefficient A in the utility function? What does it mean if A is greater than zero? (4 points) (2) Suppose the correlation coefficient pse between S and B is -1. How can you construct a portfolio X by allocating the value weight of your portfolio into S and B, so that X will be riskless? (4 points) (3) Suppose the correlation coefficient pse between S and B is 0. (1) How can you construct the optimal risky portfolio P* by allocating the value weight of your portfolio into S and B? What is the expected return and standard deviation of P*? (6 points) (ii) Next, you want to construct an optimal combined portfolio C* using the optimal risky portfolio P and the treasury bond F. Use E(rp:) = 10% and Op+ = 5% for your calculation. What is the value weight you should allocate to P* to maximize your utility? (4 points) (iii) Based on your answer to (1)&(11), calculate the ultimate value weight of funds in your optimal combined portfolio C*. What principle of modern portfolio construction you have used in this calculation? (4 points) 2. [22 points] You are given the following three assets: (1) a 10-year treasury bond F with a yield of 3%, (2) a stock fund S with E(rs) = 20%, 03 = 25%, (3) a bond fund B with E(rs) = 10%, og = 5%. Your utility function is: U = E(r) 0.5A0, where E(r) and o are the expected return and standard deviation of your investment, respectively, and A=7. (1) What is the economic meaning of coefficient A in the utility function? What does it mean if A is greater than zero? (4 points) (2) Suppose the correlation coefficient pse between S and B is -1. How can you construct a portfolio X by allocating the value weight of your portfolio into S and B, so that X will be riskless? (4 points) (3) Suppose the correlation coefficient pse between S and B is 0. (1) How can you construct the optimal risky portfolio P* by allocating the value weight of your portfolio into S and B? What is the expected return and standard deviation of P*? (6 points) (ii) Next, you want to construct an optimal combined portfolio C* using the optimal risky portfolio P and the treasury bond F. Use E(rp:) = 10% and Op+ = 5% for your calculation. What is the value weight you should allocate to P* to maximize your utility? (4 points) (iii) Based on your answer to (1)&(11), calculate the ultimate value weight of funds in your optimal combined portfolio C*. What principle of modern portfolio construction you have used in this calculation? (4 points)