please answer the following blank sheet, this is seconde year uni question

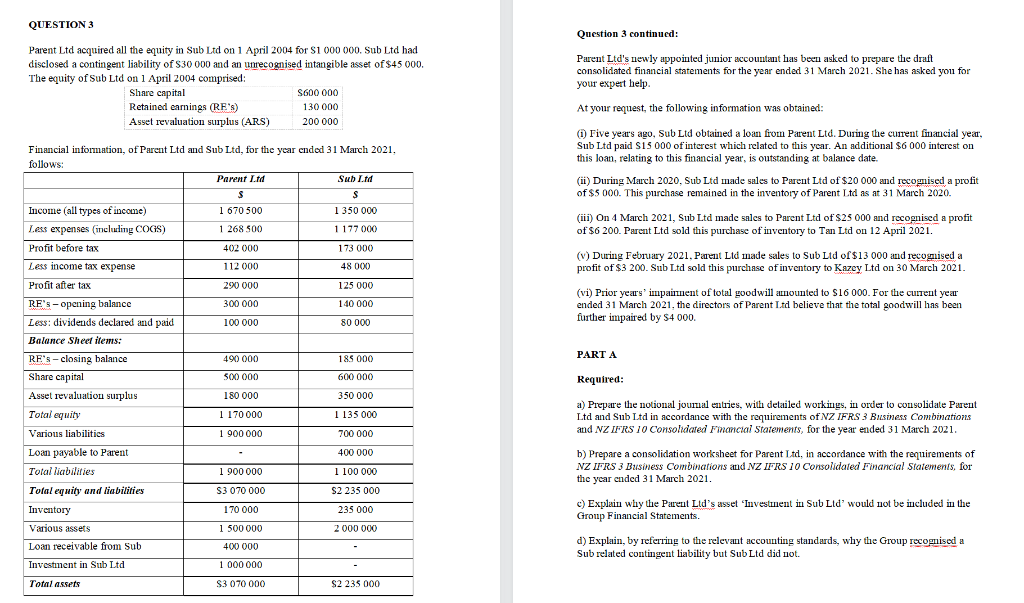

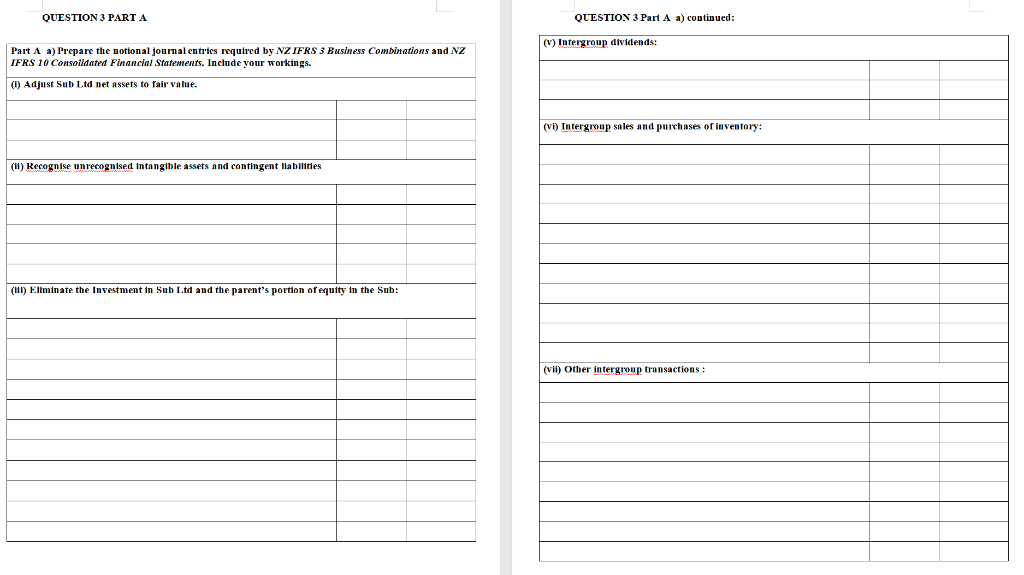

QUESTION 3 Parent Ltd acquired all the equity in Sub Ltd on 1 April 2004 for $1 000 000. Sub Ltd had disclosed a contingent liability of $30 000 and an unrecognised intangible asset of $45 000. The equity of Sub Ltd on 1 April 2004 comprised: Share capital $600 000 Retained earnings (RE's) 130 000 Asset revaluation surplus (ARS) 200 000 Financial information, of Parent Ltd and Sub Ltd, for the year ended 31 March 2021. follows: Parent Ltd $ Sub Ltd $ Income (all types of income) 1 670 500 1 350 000 1177 000 Less expenses (including COGS) 1 268 500 Profit before tax 402 000 173 000 Less income tax expense 112 000 48 000 Profit after tax 290 000 125 000 RE's-opening balance 300 000 140 000 Less: dividends declared and paid 100 000 80 000 Balance Sheet items: RE's closing balance 490 000 185 000 Share capital 500 000 600 000 180 000 350 000 Asset revaluation surplus Total equity 1 170 000 1 135 000 Various liabilities 1900 000 700 000 Loan payable to Parent 400 000 Total liabilities 1900 000 1 100 000 Total equity and liabilities Inventory $3 070 000 170 000 $2 235 000 235 000 Various assets 1 500 000 2 000 000 Loan receivable from Sub 400 000 Investment in Sub Ltd 1 000 000 - Total assets $3 070 000 $2 235 000 Question 3 continued: Parent Ltd's newly appointed junior accountant has been asked to prepare the draft consolidated financial statements for the year ended 31 March 2021. She has asked you for your expert help. At your request, the following information was obtained: (1) Five years ago, Sub Ltd obtained a loan from Parent Ltd. During the current financial year, Sub Ltd paid $15 000 of interest which related to this year. An additional $6 000 interest on this loan, relating to this financial year, is outstanding at balance date. (ii) During March 2020, Sub Ltd made sales to Parent Ltd of $20 000 and recognised a profit of $5 000. This purchase remained in the inventory of Parent Ltd as at 31 March 2020. (iii) On 4 March 2021, Sub Ltd made sales to Parent Ltd of $25 000 and recognised a profit of $6 200. Parent Ltd sold this purchase of inventory to Tan Ltd on 12 April 2021. (v) During February 2021, Parent Ltd made sales to Sub Ltd of $13 000 and recognised a profit of $3 200. Sub Ltd sold this purchase of inventory to Kazey Ltd on 30 March 2021. (vi) Prior years' impainment of total goodwill amounted to $16 000. For the current year ended 31 March 2021, the directors of Parent Ltd believe that the total goodwill has been further impaired by $4 000. PART A Required: a) Prepare the notional joumal entries, with detailed workings, in order to consolidate Parent Ltd and Sub Ltd in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021 b) Prepare a consolidation worksheet for Parent Ltd, in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021. c) Explain why the Parent Ltd's asset 'Investment in Sub Ltd' would not be included in the Group Financial Statements. d) Explain, by referring to the relevant accounting standards, why the Group recognised a Sub related contingent liability but Sub Ltd did not. QUESTION 3 PART A Part A a) Prepare the notional journal entries required by NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements. Include your workings. (1) Adjust Sub Ltd net assets fair value. (1) Recognise unrecognised intangible assets and contingent liabilities (11) Eliminate the Investment in Sub Ltd and the parent's portion of equity in the Sub: QUESTION 3 Part A a) continued: (v) Intergroup dividends: (vi) Intergroup sales and purchases of inventory: (vii) Other intergroup transactions: QUESTION 3 Parent Ltd acquired all the equity in Sub Ltd on 1 April 2004 for $1 000 000. Sub Ltd had disclosed a contingent liability of $30 000 and an unrecognised intangible asset of $45 000. The equity of Sub Ltd on 1 April 2004 comprised: Share capital $600 000 Retained earnings (RE's) 130 000 Asset revaluation surplus (ARS) 200 000 Financial information, of Parent Ltd and Sub Ltd, for the year ended 31 March 2021. follows: Parent Ltd $ Sub Ltd $ Income (all types of income) 1 670 500 1 350 000 1177 000 Less expenses (including COGS) 1 268 500 Profit before tax 402 000 173 000 Less income tax expense 112 000 48 000 Profit after tax 290 000 125 000 RE's-opening balance 300 000 140 000 Less: dividends declared and paid 100 000 80 000 Balance Sheet items: RE's closing balance 490 000 185 000 Share capital 500 000 600 000 180 000 350 000 Asset revaluation surplus Total equity 1 170 000 1 135 000 Various liabilities 1900 000 700 000 Loan payable to Parent 400 000 Total liabilities 1900 000 1 100 000 Total equity and liabilities Inventory $3 070 000 170 000 $2 235 000 235 000 Various assets 1 500 000 2 000 000 Loan receivable from Sub 400 000 Investment in Sub Ltd 1 000 000 - Total assets $3 070 000 $2 235 000 Question 3 continued: Parent Ltd's newly appointed junior accountant has been asked to prepare the draft consolidated financial statements for the year ended 31 March 2021. She has asked you for your expert help. At your request, the following information was obtained: (1) Five years ago, Sub Ltd obtained a loan from Parent Ltd. During the current financial year, Sub Ltd paid $15 000 of interest which related to this year. An additional $6 000 interest on this loan, relating to this financial year, is outstanding at balance date. (ii) During March 2020, Sub Ltd made sales to Parent Ltd of $20 000 and recognised a profit of $5 000. This purchase remained in the inventory of Parent Ltd as at 31 March 2020. (iii) On 4 March 2021, Sub Ltd made sales to Parent Ltd of $25 000 and recognised a profit of $6 200. Parent Ltd sold this purchase of inventory to Tan Ltd on 12 April 2021. (v) During February 2021, Parent Ltd made sales to Sub Ltd of $13 000 and recognised a profit of $3 200. Sub Ltd sold this purchase of inventory to Kazey Ltd on 30 March 2021. (vi) Prior years' impainment of total goodwill amounted to $16 000. For the current year ended 31 March 2021, the directors of Parent Ltd believe that the total goodwill has been further impaired by $4 000. PART A Required: a) Prepare the notional joumal entries, with detailed workings, in order to consolidate Parent Ltd and Sub Ltd in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021 b) Prepare a consolidation worksheet for Parent Ltd, in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021. c) Explain why the Parent Ltd's asset 'Investment in Sub Ltd' would not be included in the Group Financial Statements. d) Explain, by referring to the relevant accounting standards, why the Group recognised a Sub related contingent liability but Sub Ltd did not. QUESTION 3 PART A Part A a) Prepare the notional journal entries required by NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements. Include your workings. (1) Adjust Sub Ltd net assets fair value. (1) Recognise unrecognised intangible assets and contingent liabilities (11) Eliminate the Investment in Sub Ltd and the parent's portion of equity in the Sub: QUESTION 3 Part A a) continued: (v) Intergroup dividends: (vi) Intergroup sales and purchases of inventory: (vii) Other intergroup transactions