Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please answer the second problem. The first question is just included for the required context for the second one. Consider a primary mortgage market lender

Please answer the second problem. The first question is just included for the required context for the second one.

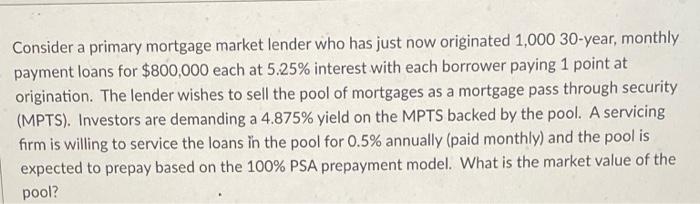

Consider a primary mortgage market lender who has just now originated 1,00030 -year, monthly payment loans for $800,000 each at 5.25% interest with each borrower paying 1 point at origination. The lender wishes to sell the pool of mortgages as a mortgage pass through security (MPTS). Investors are demanding a 4.875% yield on the MPTS backed by the pool. A servicing firm is willing to service the loans in the pool for 0.5% annually (paid monthly) and the pool is expected to prepay based on the 100% PSA prepayment model. What is the market value of the pool? What gross amount would the mortgage company receive from the origination of the loans and the sale of the MPTS in the previous problem if the expected prepayment was forecast using a 200% PSA prepayment model Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Economic Indicator Handbook How To Evaluate Economic Trends To Maximize Profits And Minimize Losses

Authors: Richard Yamarone

1st Edition

1118204662, 9781118204665