Answered step by step

Verified Expert Solution

Question

1 Approved Answer

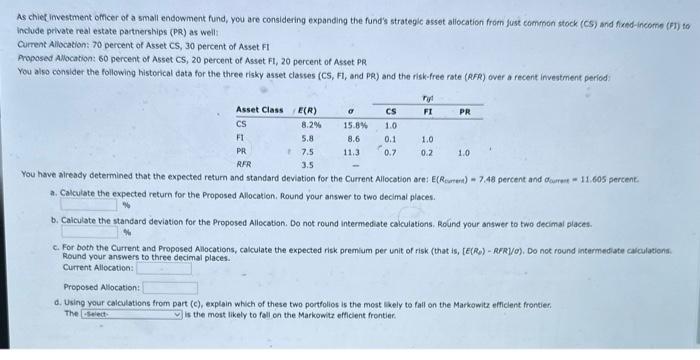

PLEASE ANSWER THESE QUESTIONS As chiecimvestment officer of a small endowment fund, you are considering expanding the fund's strategic asset aliocation from fust cominon stock

PLEASE ANSWER THESE QUESTIONS

As chiecimvestment officer of a small endowment fund, you are considering expanding the fund's strategic asset aliocation from fust cominon stock (Cs) and fined-income (F)) to include private real estate partnerships (PR) as weil: Cument Allocation: 70 percent of Asset CS, 30 percent of Asset FI Aroposed Allocation: 60 percent of Asset CS,20 percent of Asset FI,20 percent of Asset PR You also consider the following histoncal data for the three risky asset classes (CS, F, and PR) and the risk-free rate (RFR) over a fecent investment period: You have already determined that the expected return and standard deviation for the Current Allocation are: E(Rcartent)=7.48 percent and . aurret =11. cos pertent a. Calculate the expected return for the Proposed Allocation. Round your answer to two decimal places. b. Calculate the standard deviation for the Proposed Allocation. Do not round intermediate calculations. Rolind your answer to two decimal places. c. For both the Current and Proposed Allocations, calculate the expected risk premium per unit of risk (that is, [E(RQ)RFR]/), Do nok round intermediate cavculatiens. Round your answers to three decimal places. Current Allocation: Proposed Alsocation: d. Usina your calculations from bart (c), explain which of these two portfolios is the most likely to fall on the Markowitz efficlent frontier. The is the most likely to foll on the Markowitz efficient frontier Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Numerical Methods In Finance

Authors: René Carmona, Pierre Del Moral, Peng Hu, Nadia Oudjane

2012th Edition

3642257453, 978-3642257452