Answered step by step

Verified Expert Solution

Question

1 Approved Answer

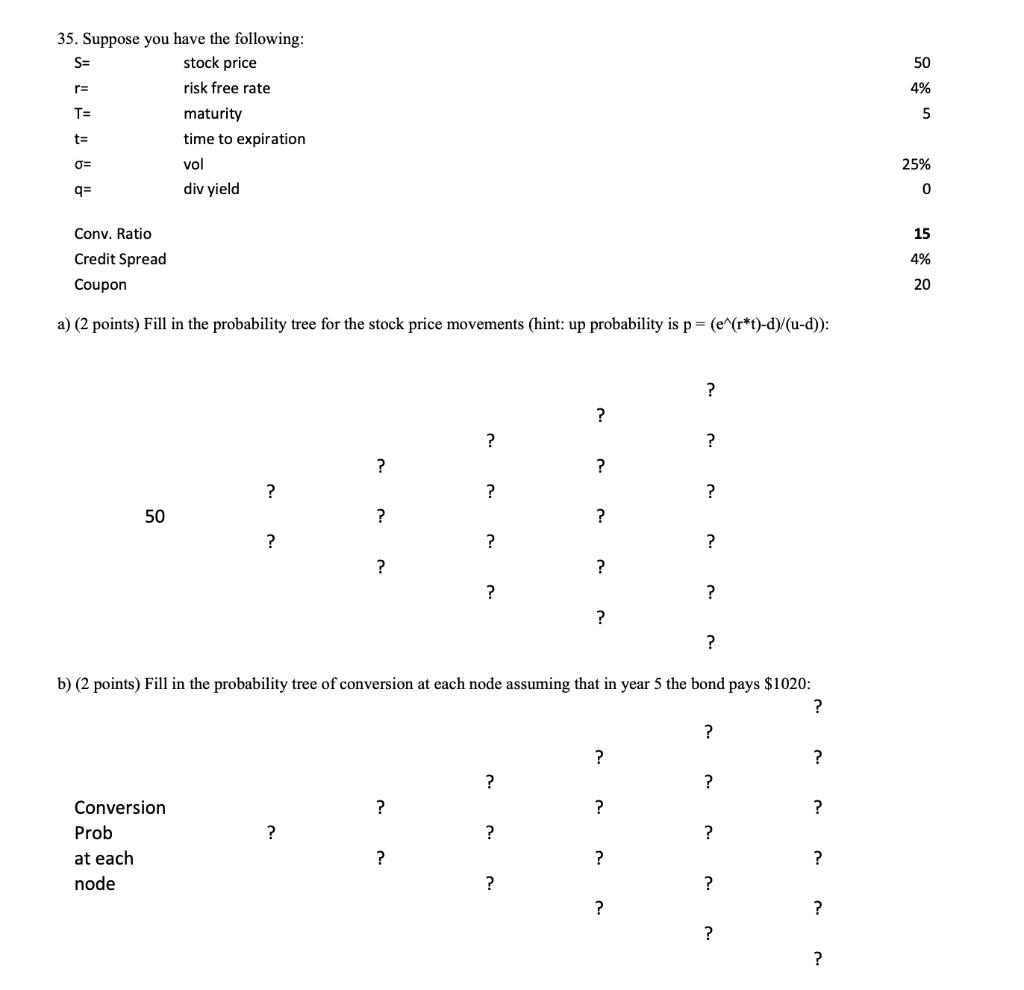

PLEASE ANSWER WITH EXPLANATION 50 4% 35. Suppose you have the following: S= stock price r= risk free rate T= maturity t= time to expiration

PLEASE ANSWER WITH EXPLANATION

50 4% 35. Suppose you have the following: S= stock price r= risk free rate T= maturity t= time to expiration vol q= div yield 5 0= 25% 0 15 Conv. Ratio Credit Spread Coupon 4% 20 a) (2 points) Fill in the probability tree for the stock price movements (hint: up probability is p=(e^(r*t)-d)/(u-d)): ? ? ? ? ? ? ? ? ? 50 ? ? ? ? ? ? ? ? ? ? ? b) (2 points) Fill in the probability tree of conversion at each node assuming that in year 5 the bond pays $1020: ? ? ? ? ? ? Conversion ? ? ? Prob ? ? ? at each ? ? ? node ? ? ? ? ? ? 50 4% 35. Suppose you have the following: S= stock price r= risk free rate T= maturity t= time to expiration vol q= div yield 5 0= 25% 0 15 Conv. Ratio Credit Spread Coupon 4% 20 a) (2 points) Fill in the probability tree for the stock price movements (hint: up probability is p=(e^(r*t)-d)/(u-d)): ? ? ? ? ? ? ? ? ? 50 ? ? ? ? ? ? ? ? ? ? ? b) (2 points) Fill in the probability tree of conversion at each node assuming that in year 5 the bond pays $1020: ? ? ? ? ? ? Conversion ? ? ? Prob ? ? ? at each ? ? ? nodeStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Regulation A+ And Other Alternatives To A Traditional IPO Financing Your Growth Business Following The JOBS Act

Authors: David N. Feldman

1st Edition

1119416159,1119416124