Please calculate the cost of capital (WACC) and price per share. Remember that in your calculations, beta is truly a matter of expectations rather than history and the selection of a risk-free rate of return should be consistent with the remaining life of the asset being valued.

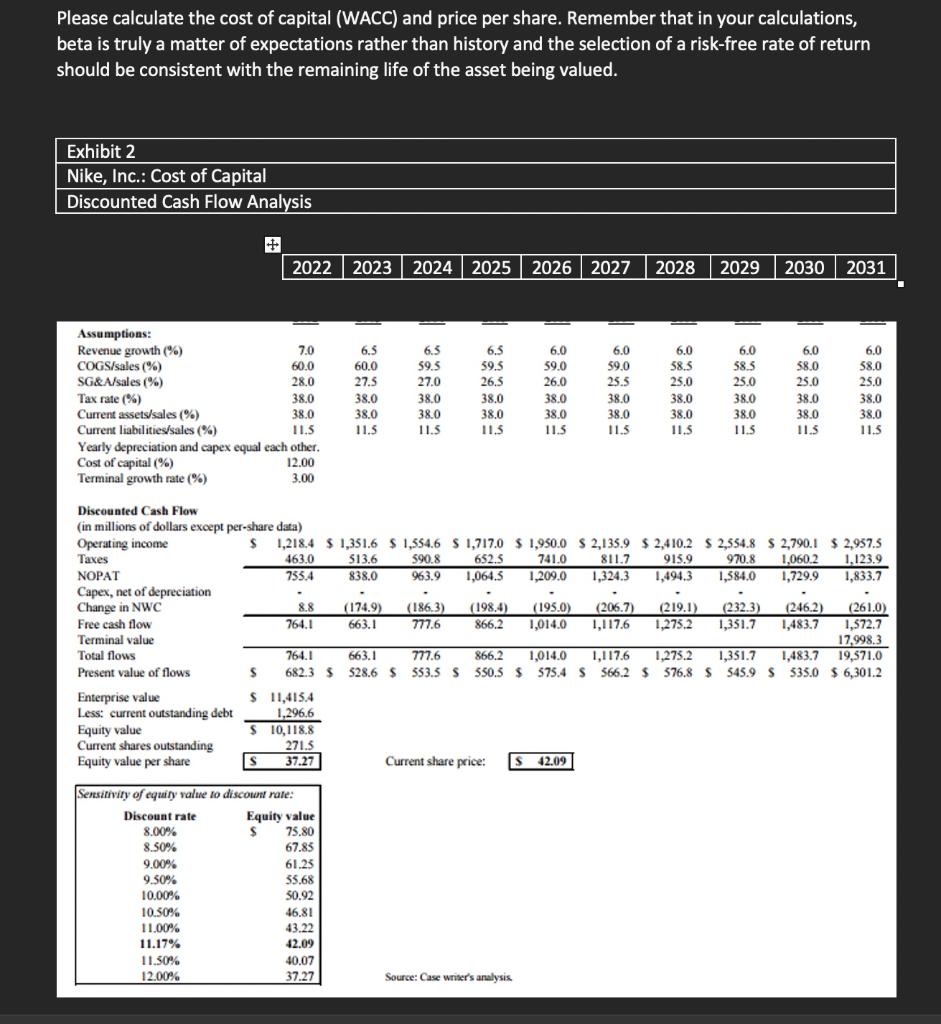

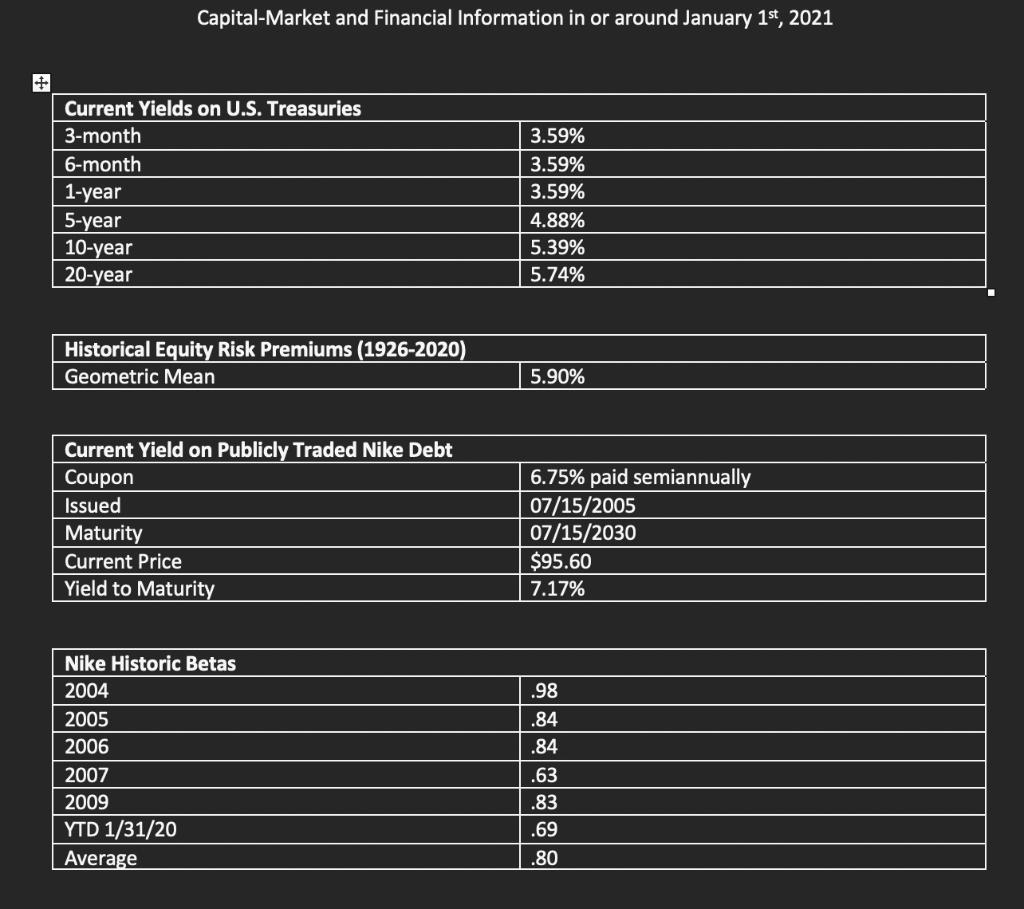

In January 31st 2021, Kimi Ford, a portfolio manager at NorthPoint Group, a mutual-fund management firm, pored over analysts' write-ups of Nike, Inc., the athletic manufacturer. Nike's share price had declined significantly from the beginning of the year. Ford was considering buying some shares for the fund she managed, the NorthPoint Large-Cap Fund, which invested mostly in Fortune 500 companies, with an emphasis on value investing. Its top holdings included ExxonMobil, General Motors, McDonald's, 3M, and other large-cap, generally old-economy stocks. While the stock market had declined over the last 18 months, the NorthPoint Large-Cap Fund had performed extremely well. In 2019, the fund earned a return of 20.7%, even as the S&P 500 fell 10.1%. At the end of June 2020, the fund's year-to-date returns stood at 6.4% versus -7.3% for the S&P 500. Only a week earlier, in January 20, 2021, Mike had held an analysts' meeting to disclose its fiscal-year 2020 results. The meeting, however, had another purpose: Nike management wanted to communicate a strategy for revitalizing the company. Since 2017, its revenues had plateaued at around $9 billion, while net income had fallen from almost $800 million to $580 million. Nike's market share in U.S. athletic shoes had fallen from 48%, in 2016, to 42% in 2019. In addition, recent supply-chain issues and the adverse effect of a strong dollar had negatively affected revenue. At the meeting, management revealed plans to address both top-line growth and operating performance. To boost revenue, the company would develop more athletic-shoe products in the midpriced segment-a segment that Nike had overlooked in recent years. Nike also planned to push its apparel line, which, under the recent leadership of industry veteran Mindy Grossman, had performed extremely well. On the cost side, Nike would exert more effort to expense control. Finally, company executives reiterated their long-term revenue-growths targets of 8% to 10% and earnings-growth targets above 15%. Analysts' reactions were mixed. Some thought the financial targets were too aggressive; others saw significant growth opportunities in apparel and in Nike's international businesses. Kimi Ford read all the analysts' reports that she could find about the January 31st meeting, but the reports gave her no clear guidance: a Lehman Brothers report recommended a strong buy, while UBS Warburg and CSFB analysts expressed misgivings about the company and recommended a hold. Ford decided instead to develop her own discounted cash flow forecast to come to a clearer conclusion. Her forecast showed that, at a discount rate of 12%, Nike was overvalued at its current share price of $42.09. However, she had done a quick sensitivity analysis and revealed Nike was undervalued at discount rates below 11.17%. Because she was about to go into a meeting, she needs an analyst to estimate Nike's cost of capital and price per share. a Please calculate the cost of capital (WACC) and price per share. Remember that in your calculations, beta is truly a matter of expectations rather than history and the selection of a risk-free rate of return should be consistent with the remaining life of the asset being valued. Exhibit 2 Nike, Inc.: Cost of Capital Discounted Cash Flow Analysis 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 6.3 59.5 6.3 59.5 Assumptions: Revenue growth (%) 7.0 COGS/sales (%) 60.0 SG&A/sales (%) ) 28.0 Tax rate (%) tax rate (%) 38.0 Current assets/sales (%) 38.0 Current liabilities/sales (%) 11.5 Yearly depreciation and capex equal each other. Cost of capital (% 12.00 Terminal growth rate (%) 3.00 6.5 60.0 27.5 38.0 38.0 11.5 27.0 6.0 59.0 26.0 38.0 38.0 11.5 26.5 38.0 38.0 11.5 6.0 59.0 25.5 38.0 38.0 11.5 6.0 58.5 25.0 38,0 38.0 11.5 6.0 58.5 25.0 38.0 38.0 11.3 6.0 58.0 25.0 38.0 38.0 11.5 6.0 58.0 25.0 38.0 38.0 38.0 38.0 11.5 11.5 590.8 Discounted Cash Flow (in millions of dollars except per-share data) Operating income s 1,218.4 $1,351.6 $ 1,554.6 S 1,717,0 $ 1,950.0 S 2,135.9 $ 2.410.2 $2,554.8 $ 2,790.1 $2,957.5 Taxes 463.0 513.6 $ 652.5 NODA 741.0 811.7 915.9 970,8 1,0602 1.123.9 NOPAT 735.4 838.0 963.9 1,064.3 1,209,0 1.324.3 1,494,3 1,584.0 1,729.9 1,833.7 Capex, net of depreciation Change in NWC 8.8 (174.9) (1863) (198,4) (195.0) (206.7) (219.1) (232.3) (246.2) (261.0) Free cash flow 764.1 663.1 777.6 866.2 1,014.0 1,117.6 1,273.2 1,351.7 1,483.7 1,572.7 Terminal value 17,998.3 Total flows 764.1 663.1 777.6 866.2 1,014.0 1,117.6 1,275.2 1,351.7 1,483.7 19,571.0 Present value of flows $ 682.3 $ $28.6 $ 353.3 $ 550.5 $ $75.4 S 566.2 $ 576.8 $ 545.9 S 335.0 $ 6,301.2 Enterprise value $ 11,415.4 Less: current outstanding debt 1.296.6 Equity value $ 10,118.8 Current shares outstanding 271.5 Equity value per share s 37.27 Current share price: : S42.09 Sensitivity of equity value to discount rate: Discount rate Equity value 8.00% $ 75.80 8.50% 67.85 9.00% 61.25 9.50% 35.68 10.00% 0.94 $0.92 10.50% 46.81 11.00% 11.17% 42.09 11.50% 40.07 12.00% 37.27 43.22 Source: Case writer's analysis : Capital-Market and Financial Information in or around January 1st, 2021 + Current Yields on U.S. Treasuries 3-month 6-month 1-year 5-year 10-year 20-year 3.59% 3.59% 3.59% 4.88% 5.39% 5.74% Historical Equity Risk Premiums (1926-2020) Geometric Mean 5.90% Current Yield on Publicly Traded Nike Debt Coupon Issued Maturity Current Price Yield to Maturity 6.75% paid semiannually 07/15/2005 07/15/2030 $95.60 7.17% TT Nike Historic Betas 2004 2005 2006 2007 2009 YTD 1/31/20 Average .98 .84 .84 .63 .83 .69 .80 Formulas: Pa = 14 + Bal Im - pt) = Where: If Risk free rate Ba = Beta of the security I'm Expected market return = The market risk premium is the market return minus the risk free rate WACC = WCSR s +R (1-Tx) + WpRp = CSCS D D Remember that the cost of debt is the YTM PV = Cash Flows / (1+WACC)^t Enterprise Value: Total Value of the Company Price per share: PV of future free cash flows (including terminal value) / current share outstanding In January 31st 2021, Kimi Ford, a portfolio manager at NorthPoint Group, a mutual-fund management firm, pored over analysts' write-ups of Nike, Inc., the athletic manufacturer. Nike's share price had declined significantly from the beginning of the year. Ford was considering buying some shares for the fund she managed, the NorthPoint Large-Cap Fund, which invested mostly in Fortune 500 companies, with an emphasis on value investing. Its top holdings included ExxonMobil, General Motors, McDonald's, 3M, and other large-cap, generally old-economy stocks. While the stock market had declined over the last 18 months, the NorthPoint Large-Cap Fund had performed extremely well. In 2019, the fund earned a return of 20.7%, even as the S&P 500 fell 10.1%. At the end of June 2020, the fund's year-to-date returns stood at 6.4% versus -7.3% for the S&P 500. Only a week earlier, in January 20, 2021, Mike had held an analysts' meeting to disclose its fiscal-year 2020 results. The meeting, however, had another purpose: Nike management wanted to communicate a strategy for revitalizing the company. Since 2017, its revenues had plateaued at around $9 billion, while net income had fallen from almost $800 million to $580 million. Nike's market share in U.S. athletic shoes had fallen from 48%, in 2016, to 42% in 2019. In addition, recent supply-chain issues and the adverse effect of a strong dollar had negatively affected revenue. At the meeting, management revealed plans to address both top-line growth and operating performance. To boost revenue, the company would develop more athletic-shoe products in the midpriced segment-a segment that Nike had overlooked in recent years. Nike also planned to push its apparel line, which, under the recent leadership of industry veteran Mindy Grossman, had performed extremely well. On the cost side, Nike would exert more effort to expense control. Finally, company executives reiterated their long-term revenue-growths targets of 8% to 10% and earnings-growth targets above 15%. Analysts' reactions were mixed. Some thought the financial targets were too aggressive; others saw significant growth opportunities in apparel and in Nike's international businesses. Kimi Ford read all the analysts' reports that she could find about the January 31st meeting, but the reports gave her no clear guidance: a Lehman Brothers report recommended a strong buy, while UBS Warburg and CSFB analysts expressed misgivings about the company and recommended a hold. Ford decided instead to develop her own discounted cash flow forecast to come to a clearer conclusion. Her forecast showed that, at a discount rate of 12%, Nike was overvalued at its current share price of $42.09. However, she had done a quick sensitivity analysis and revealed Nike was undervalued at discount rates below 11.17%. Because she was about to go into a meeting, she needs an analyst to estimate Nike's cost of capital and price per share. a Please calculate the cost of capital (WACC) and price per share. Remember that in your calculations, beta is truly a matter of expectations rather than history and the selection of a risk-free rate of return should be consistent with the remaining life of the asset being valued. Exhibit 2 Nike, Inc.: Cost of Capital Discounted Cash Flow Analysis 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 6.3 59.5 6.3 59.5 Assumptions: Revenue growth (%) 7.0 COGS/sales (%) 60.0 SG&A/sales (%) ) 28.0 Tax rate (%) tax rate (%) 38.0 Current assets/sales (%) 38.0 Current liabilities/sales (%) 11.5 Yearly depreciation and capex equal each other. Cost of capital (% 12.00 Terminal growth rate (%) 3.00 6.5 60.0 27.5 38.0 38.0 11.5 27.0 6.0 59.0 26.0 38.0 38.0 11.5 26.5 38.0 38.0 11.5 6.0 59.0 25.5 38.0 38.0 11.5 6.0 58.5 25.0 38,0 38.0 11.5 6.0 58.5 25.0 38.0 38.0 11.3 6.0 58.0 25.0 38.0 38.0 11.5 6.0 58.0 25.0 38.0 38.0 38.0 38.0 11.5 11.5 590.8 Discounted Cash Flow (in millions of dollars except per-share data) Operating income s 1,218.4 $1,351.6 $ 1,554.6 S 1,717,0 $ 1,950.0 S 2,135.9 $ 2.410.2 $2,554.8 $ 2,790.1 $2,957.5 Taxes 463.0 513.6 $ 652.5 NODA 741.0 811.7 915.9 970,8 1,0602 1.123.9 NOPAT 735.4 838.0 963.9 1,064.3 1,209,0 1.324.3 1,494,3 1,584.0 1,729.9 1,833.7 Capex, net of depreciation Change in NWC 8.8 (174.9) (1863) (198,4) (195.0) (206.7) (219.1) (232.3) (246.2) (261.0) Free cash flow 764.1 663.1 777.6 866.2 1,014.0 1,117.6 1,273.2 1,351.7 1,483.7 1,572.7 Terminal value 17,998.3 Total flows 764.1 663.1 777.6 866.2 1,014.0 1,117.6 1,275.2 1,351.7 1,483.7 19,571.0 Present value of flows $ 682.3 $ $28.6 $ 353.3 $ 550.5 $ $75.4 S 566.2 $ 576.8 $ 545.9 S 335.0 $ 6,301.2 Enterprise value $ 11,415.4 Less: current outstanding debt 1.296.6 Equity value $ 10,118.8 Current shares outstanding 271.5 Equity value per share s 37.27 Current share price: : S42.09 Sensitivity of equity value to discount rate: Discount rate Equity value 8.00% $ 75.80 8.50% 67.85 9.00% 61.25 9.50% 35.68 10.00% 0.94 $0.92 10.50% 46.81 11.00% 11.17% 42.09 11.50% 40.07 12.00% 37.27 43.22 Source: Case writer's analysis : Capital-Market and Financial Information in or around January 1st, 2021 + Current Yields on U.S. Treasuries 3-month 6-month 1-year 5-year 10-year 20-year 3.59% 3.59% 3.59% 4.88% 5.39% 5.74% Historical Equity Risk Premiums (1926-2020) Geometric Mean 5.90% Current Yield on Publicly Traded Nike Debt Coupon Issued Maturity Current Price Yield to Maturity 6.75% paid semiannually 07/15/2005 07/15/2030 $95.60 7.17% TT Nike Historic Betas 2004 2005 2006 2007 2009 YTD 1/31/20 Average .98 .84 .84 .63 .83 .69 .80 Formulas: Pa = 14 + Bal Im - pt) = Where: If Risk free rate Ba = Beta of the security I'm Expected market return = The market risk premium is the market return minus the risk free rate WACC = WCSR s +R (1-Tx) + WpRp = CSCS D D Remember that the cost of debt is the YTM PV = Cash Flows / (1+WACC)^t Enterprise Value: Total Value of the Company Price per share: PV of future free cash flows (including terminal value) / current share outstanding