Answered step by step

Verified Expert Solution

Question

1 Approved Answer

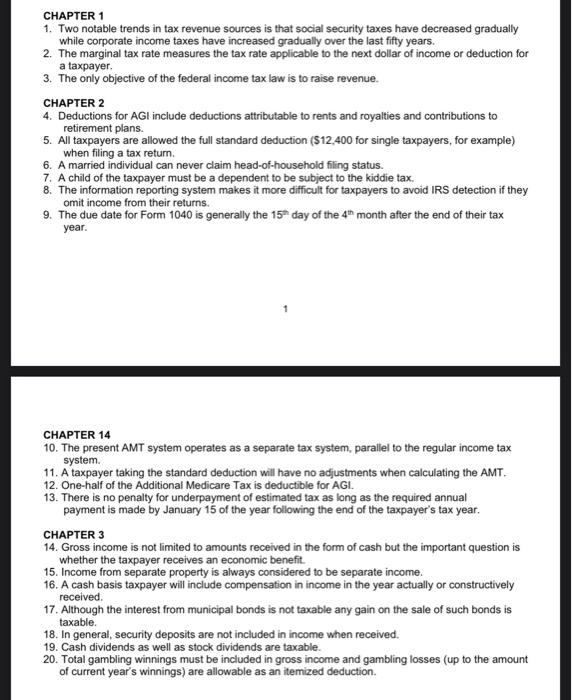

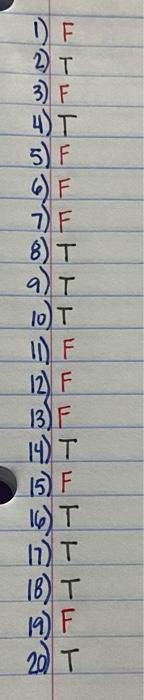

please check all of my work CHAPTER 1 1. Two notable trends in tax revenue sources is that social security taxes have decreased gradually while

please check all of my work

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Exploring Strategic Change

Authors: Julia Balogun, Veronica Hope Hailey, Stafanie Gustafsson

4th Edition

0273778919, 9780273778912