Answered step by step

Verified Expert Solution

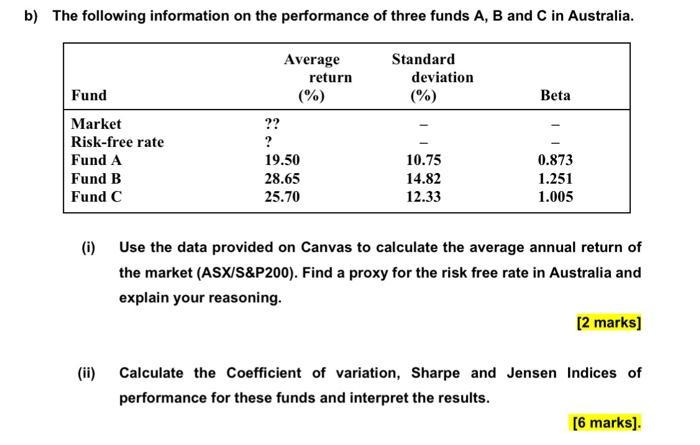

Question

1 Approved Answer

Please do not copy and paste other exiting answer! where mathematical calculations are required, state the equation used and all workings in the answer b)

Please do not copy and paste other exiting answer!

where mathematical calculations are required, state the equation used and all workings in the answer

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modeling Financial Time Series With S PLUS

Authors: Eric Zivot, Jiahui Wang

2nd Edition

0387279652, 0387323481, 9780387279657, 9780387323480