Answered step by step

Verified Expert Solution

Question

1 Approved Answer

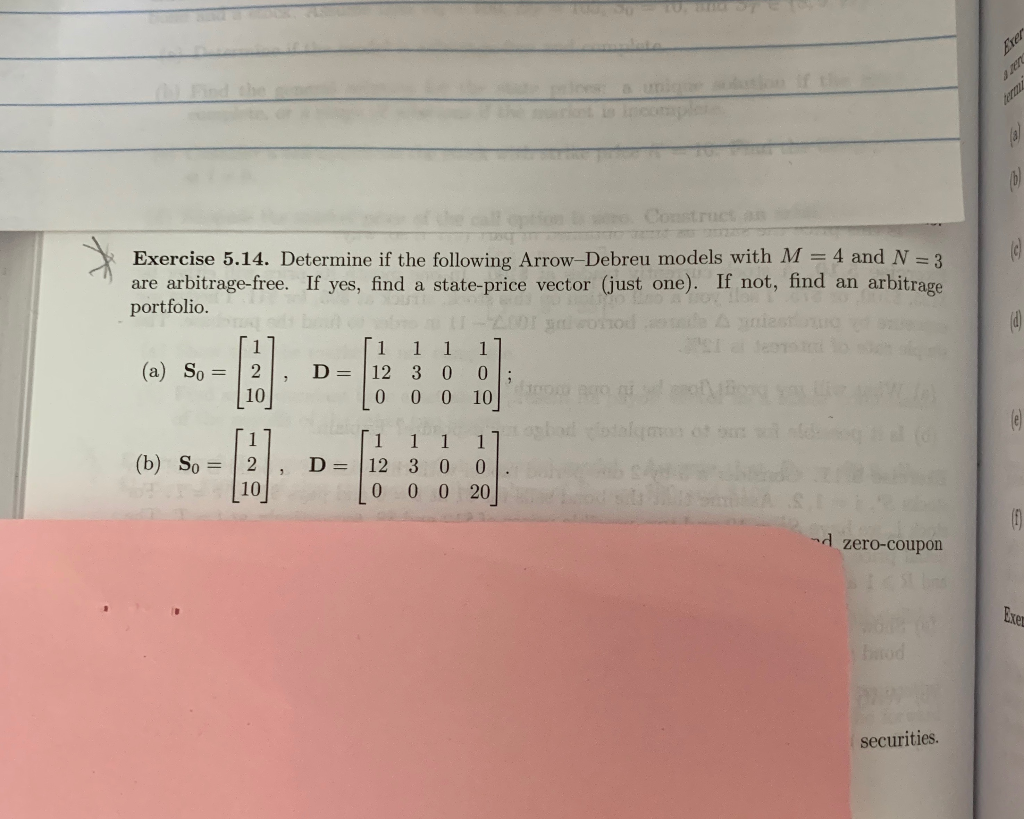

Please explain as much as you can. Textbook: Financial Mathematics A comprehensive Treatment by Giuseppe Campolieti page 202, Exercise 5.14 Exercise 5.14. Determine if the

Please explain as much as you can.

Textbook: Financial Mathematics A comprehensive Treatment by Giuseppe Campolieti

page 202, Exercise 5.14

Exercise 5.14. Determine if the following Arrow-Debreu models with M = 4 and N = 3 are arbitrage-free. If yes, find a state-price vector (just one). If not, find an arbitrage portfolio (a) So = ] 2 , [10] D= [1 12 [o 1 1 1] 3 0 0; 0 0 10 (b) So = 2, D= 12 3 0 0 [10] [0 0 0 20] - zero-coupon Exe hod securities. Exercise 5.14. Determine if the following Arrow-Debreu models with M = 4 and N = 3 are arbitrage-free. If yes, find a state-price vector (just one). If not, find an arbitrage portfolio (a) So = ] 2 , [10] D= [1 12 [o 1 1 1] 3 0 0; 0 0 10 (b) So = 2, D= 12 3 0 0 [10] [0 0 0 20] - zero-coupon Exe hod securitiesStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Weathering The Storm A Quick Guide To Safeguarding Your Finances During Economic Recession

Authors: Liam Wilhelm

1st Edition

979-8864393628