Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please explain how student loans are asset backed securities and how they relate to the photos provided. thanks rn. APTER 7 INTRODUCTION TO ASSET-BACKED SECURITIES

please explain how student loans are asset backed securities and how they relate to the photos provided. thanks

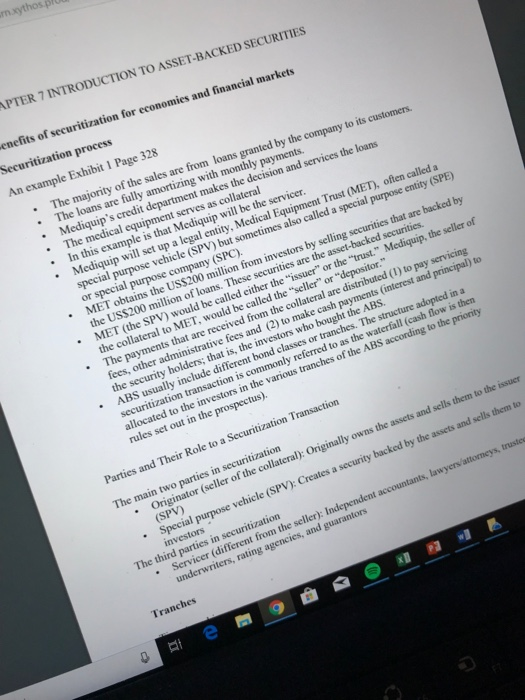

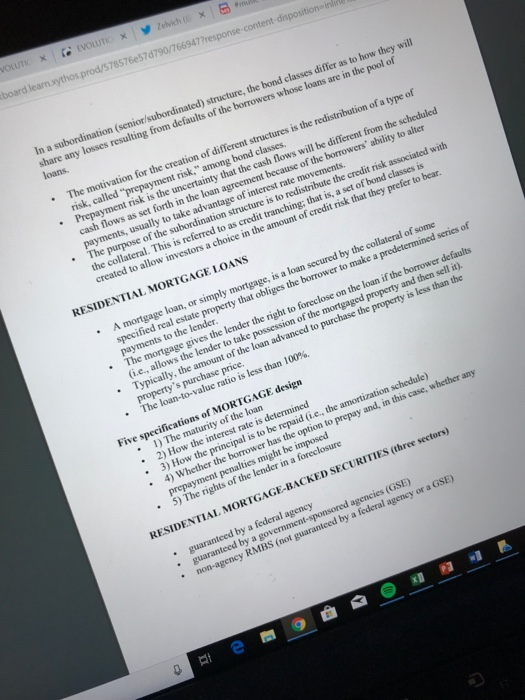

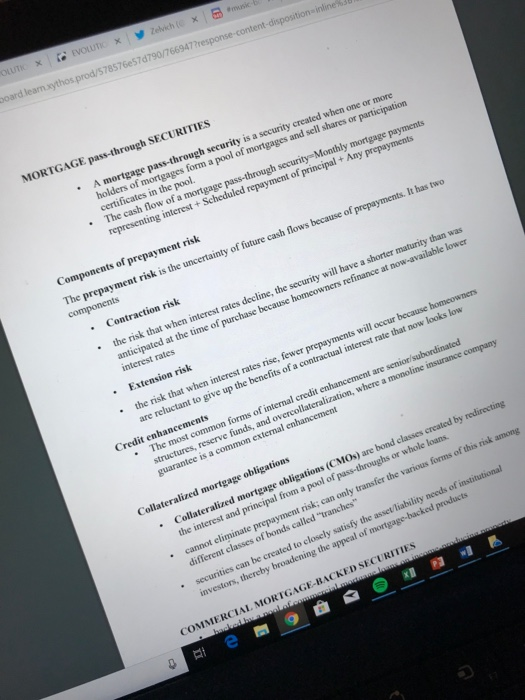

rn. APTER 7 INTRODUCTION TO ASSET-BACKED SECURITIES enefits of securitization for economies and financial markets Securitization process An example Exhibit 1 Page 328 . The majority of the sales are from loans granted by the company to its customers The loans are fully amortizing with monthly payments. Mediquip's credit department makes the decision and services the loans . The medical equipment serves as collateral In this example is that Mediquip will be the servicer. Mediquip will set up a legal entity, Medical Equipment Trust (MET special purpose vehicle (SPV) but sometimes also called a special purpose entity (SPE) se con MET obtains the US$200 million from investors by selling securities that are MET (the SPV) would be called either the "issuer" or the "trust. .Th the US$200 million of loans. These are the asset-backed securities. " Mediquip, the seller of the collateral to MET, would be called the "seller" or "depositor. he payments that are received from the collateral are distributed() to pay fees, other administrative fees and (2) to make cash pa the security and principal) to that is, the investors who bought the ABS ABS usually include different bond classes or t securitization transaction is commonly re allocated to the investors in the various tranches of the ABS ferred to as the waterfall (cash flow is then rules set out in the prospectus). Parties and Their Role to a Securitization Transaction Originator (seller of the collateral): Originally owns the assets and sells them to the issuer Special purpose vehicle (SPV): Creates a security backed by the assets and sells them to The main two parties in securitization The third parties in securitization . Servicer (different from the seller): Independent accountants, lawyers/attorneys, truste underwriters, rating agencies, and guarantors Tranches board le 78576e57d790/766947response-content-disposition in In a subordination (senior/subordinated) structure, the bond classes differ as to how they will share any losses resulting from defaults of the borrowers whose loans are in the pool of The motivation for the creation of different structures is the redistribution of a type of risk, called "prepayment risk." among Prepayment risk cash flows as set forth in the loan agreement because of bond classes. is the uncertainty that the cash flows will be different from the scheduled the borrowers' ability to alter atruerture is to redisibute tditkociated wih the collateral. This is referred to as credit tranching: that is, created to allow investors a choice in the amount a set of bond classes is of credit risk that they prefer to bear. RESIDENTIAL MORTGAGE LOANS mortgage loan, or simply mortgage, is a loan secured by the collateral of some specified real estate property that payments to the lender obliges the borrower to make a predetermined series of er defaults mortgage gives the lender the right to foreclose on the loan if the (i.e., allows the lender to take the The to take possession of the mortgaged property and then sell it). , the amount of the loan advanced to purchase the property is less than the -The loan-to-value ratio is less than 100%. Five specifications of MORTGAGE design 1) The maturity of the loan .2) How the interest rate is determined . 3) How the principal is to be repaid (i.e, the amortization schedule 4) Whether the borrower has the option to prepay and, in this case, whether any .5) The rights of the lender in a foreclosure RESIDENTIAL MORTGAGE-BACKED SECURITIES (three sectors) guaranteed by a federal agency non-agency RMBS (not guaranteed by a federal agency or a GSE) . . MORTGAGE pass-through SECURITIES through security is a security created when one or more holders of mortgages certificates in the pool. form a pool of mortgages and sell shares or participation The cash flow of a mortgage secunty interest + Scheduled repayment of principal+ Any prepayments Components of prepayment risk he prepayment risk is the components uncertainty of future cash flows because of Contraction risk when interest rates decline, the security will have a shorter maturity than was anticipated at the time of interest rates Extension risk the risk that when are reluctant to give up the benefits of a contractual interest rate that now looks low interest rates rise, fewer prepayments will occur because homeowners Credit enhancements structures, reserve funds, and overcollateralization, where a monoline insurance guarantee is a common external Collateralized mortgage obligations Collateralized mortgage obligations (CMOs) are bond classes created by redirecting the interest and principal from a pool of pass-throughs or whole loans. cannot eliminate prepayment risk; can only transfer the various forms of this risk among different classes of bonds called "tranches" securities can be created to closely satisfy the asset/liability needs of institutional COMMERCIAL MORTGAGE-BACKED SECURITIES rn. APTER 7 INTRODUCTION TO ASSET-BACKED SECURITIES enefits of securitization for economies and financial markets Securitization process An example Exhibit 1 Page 328 . The majority of the sales are from loans granted by the company to its customers The loans are fully amortizing with monthly payments. Mediquip's credit department makes the decision and services the loans . The medical equipment serves as collateral In this example is that Mediquip will be the servicer. Mediquip will set up a legal entity, Medical Equipment Trust (MET special purpose vehicle (SPV) but sometimes also called a special purpose entity (SPE) se con MET obtains the US$200 million from investors by selling securities that are MET (the SPV) would be called either the "issuer" or the "trust. .Th the US$200 million of loans. These are the asset-backed securities. " Mediquip, the seller of the collateral to MET, would be called the "seller" or "depositor. he payments that are received from the collateral are distributed() to pay fees, other administrative fees and (2) to make cash pa the security and principal) to that is, the investors who bought the ABS ABS usually include different bond classes or t securitization transaction is commonly re allocated to the investors in the various tranches of the ABS ferred to as the waterfall (cash flow is then rules set out in the prospectus). Parties and Their Role to a Securitization Transaction Originator (seller of the collateral): Originally owns the assets and sells them to the issuer Special purpose vehicle (SPV): Creates a security backed by the assets and sells them to The main two parties in securitization The third parties in securitization . Servicer (different from the seller): Independent accountants, lawyers/attorneys, truste underwriters, rating agencies, and guarantors Tranches board le 78576e57d790/766947response-content-disposition in In a subordination (senior/subordinated) structure, the bond classes differ as to how they will share any losses resulting from defaults of the borrowers whose loans are in the pool of The motivation for the creation of different structures is the redistribution of a type of risk, called "prepayment risk." among Prepayment risk cash flows as set forth in the loan agreement because of bond classes. is the uncertainty that the cash flows will be different from the scheduled the borrowers' ability to alter atruerture is to redisibute tditkociated wih the collateral. This is referred to as credit tranching: that is, created to allow investors a choice in the amount a set of bond classes is of credit risk that they prefer to bear. RESIDENTIAL MORTGAGE LOANS mortgage loan, or simply mortgage, is a loan secured by the collateral of some specified real estate property that payments to the lender obliges the borrower to make a predetermined series of er defaults mortgage gives the lender the right to foreclose on the loan if the (i.e., allows the lender to take the The to take possession of the mortgaged property and then sell it). , the amount of the loan advanced to purchase the property is less than the -The loan-to-value ratio is less than 100%. Five specifications of MORTGAGE design 1) The maturity of the loan .2) How the interest rate is determined . 3) How the principal is to be repaid (i.e, the amortization schedule 4) Whether the borrower has the option to prepay and, in this case, whether any .5) The rights of the lender in a foreclosure RESIDENTIAL MORTGAGE-BACKED SECURITIES (three sectors) guaranteed by a federal agency non-agency RMBS (not guaranteed by a federal agency or a GSE) . . MORTGAGE pass-through SECURITIES through security is a security created when one or more holders of mortgages certificates in the pool. form a pool of mortgages and sell shares or participation The cash flow of a mortgage secunty interest + Scheduled repayment of principal+ Any prepayments Components of prepayment risk he prepayment risk is the components uncertainty of future cash flows because of Contraction risk when interest rates decline, the security will have a shorter maturity than was anticipated at the time of interest rates Extension risk the risk that when are reluctant to give up the benefits of a contractual interest rate that now looks low interest rates rise, fewer prepayments will occur because homeowners Credit enhancements structures, reserve funds, and overcollateralization, where a monoline insurance guarantee is a common external Collateralized mortgage obligations Collateralized mortgage obligations (CMOs) are bond classes created by redirecting the interest and principal from a pool of pass-throughs or whole loans. cannot eliminate prepayment risk; can only transfer the various forms of this risk among different classes of bonds called "tranches" securities can be created to closely satisfy the asset/liability needs of institutional COMMERCIAL MORTGAGE-BACKED SECURITIES Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Core Concepts

Authors: Raymond M Brooks

2nd edition

132671034, 978-0132671033