Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please explain what is wrong. On January 1, 2021, Displays Incorporated had the following account balances: Debit Credit $ 36,000 Accounts Cash Accounts receivable Supplies

please explain what is wrong.

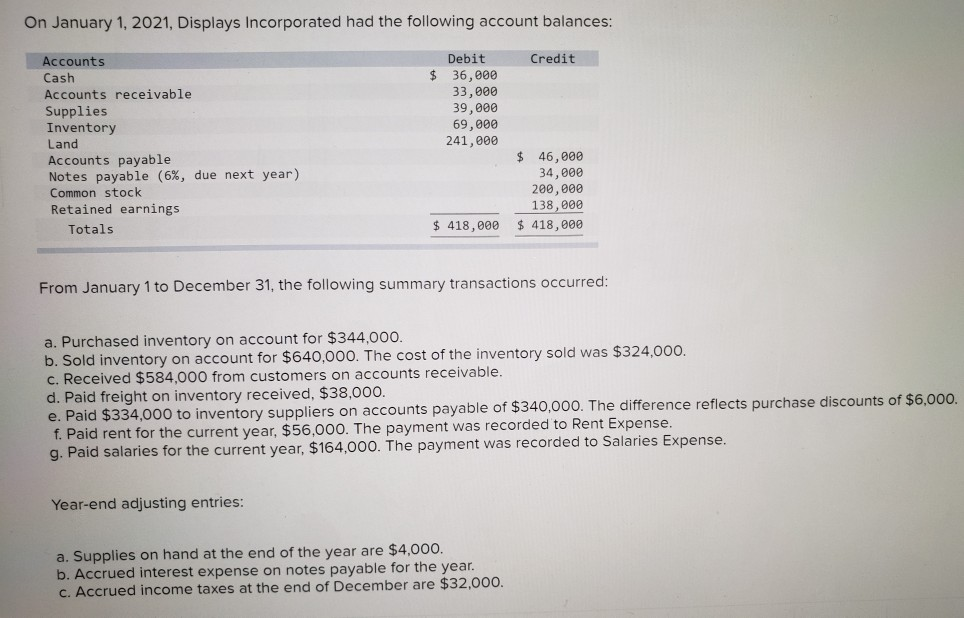

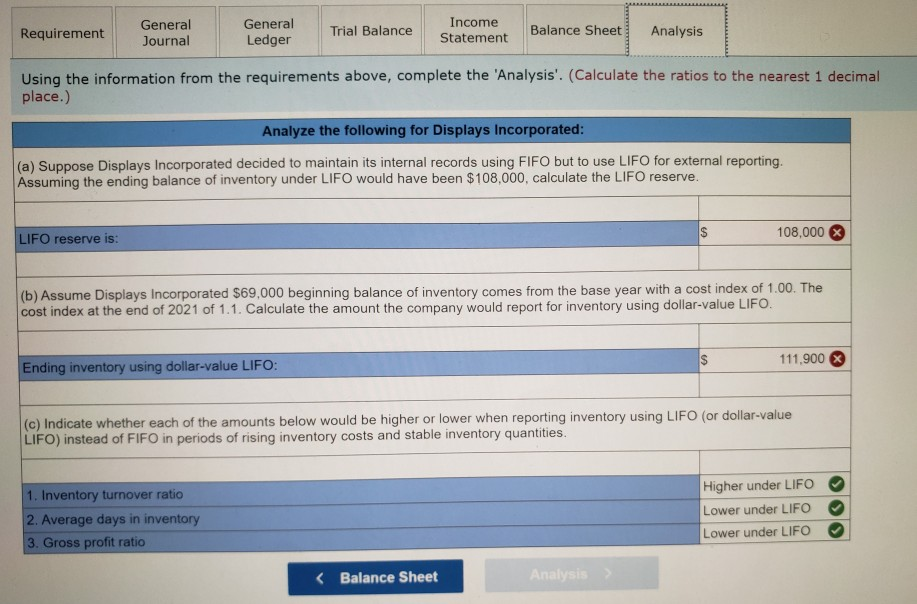

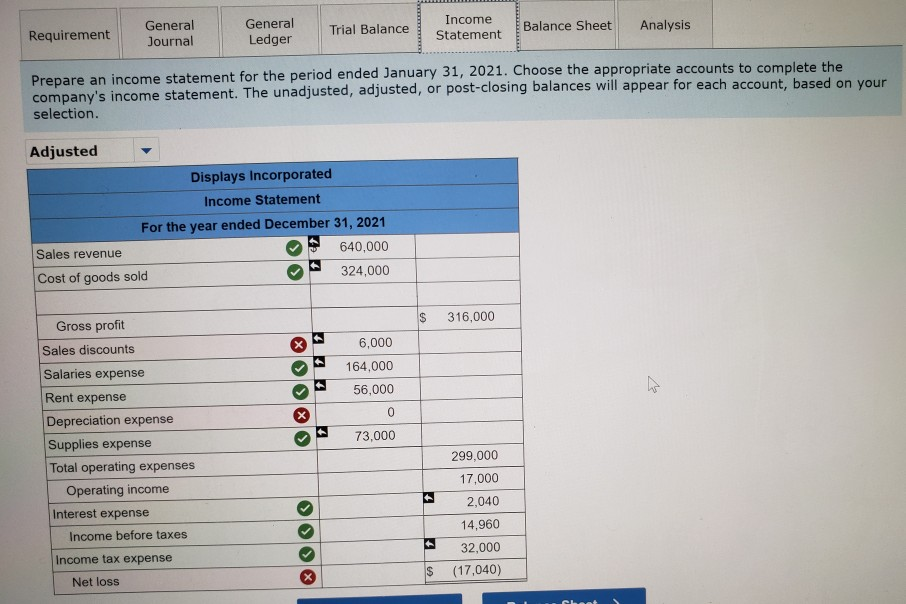

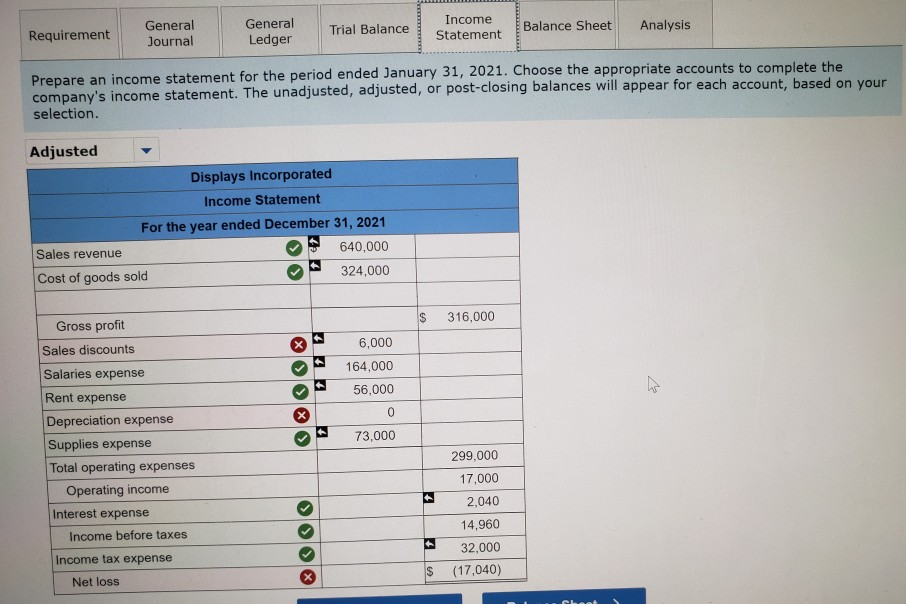

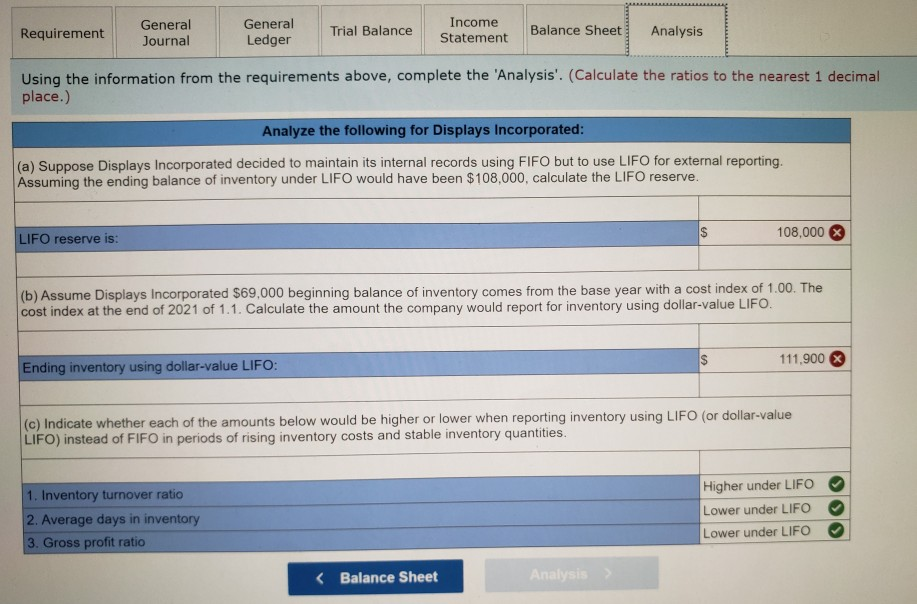

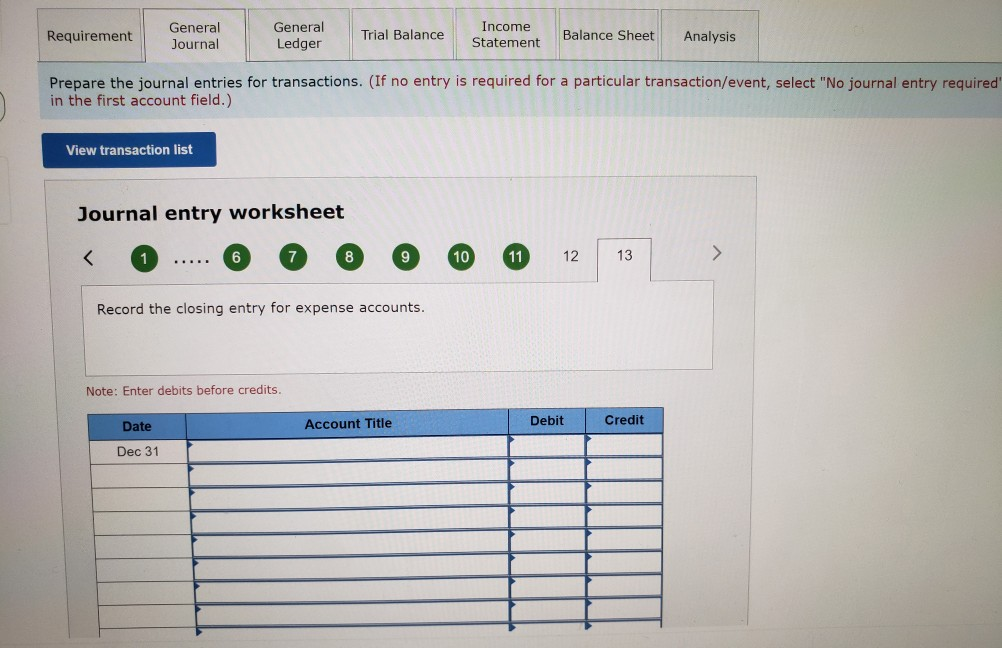

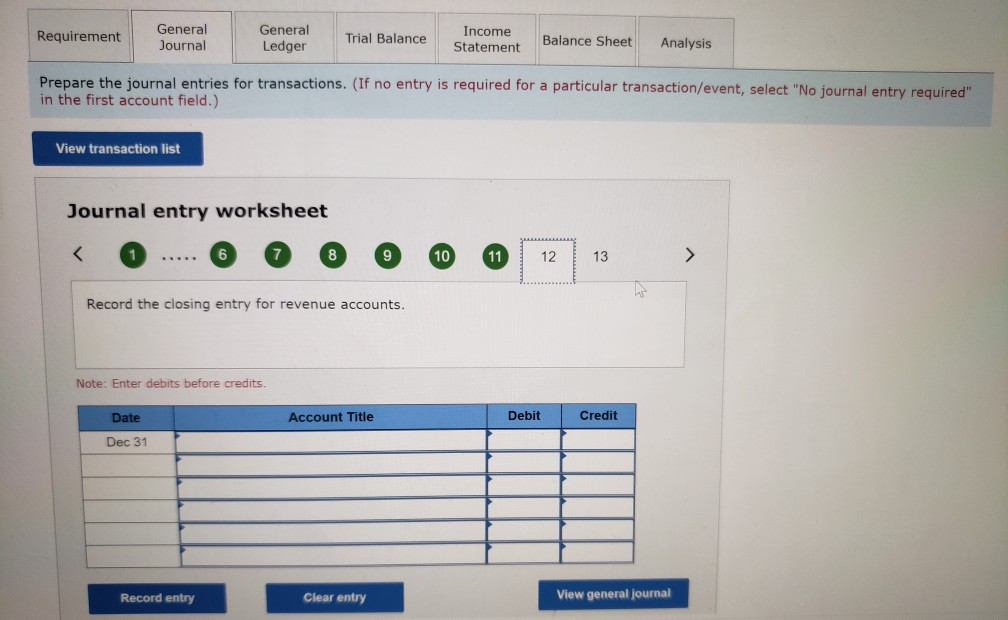

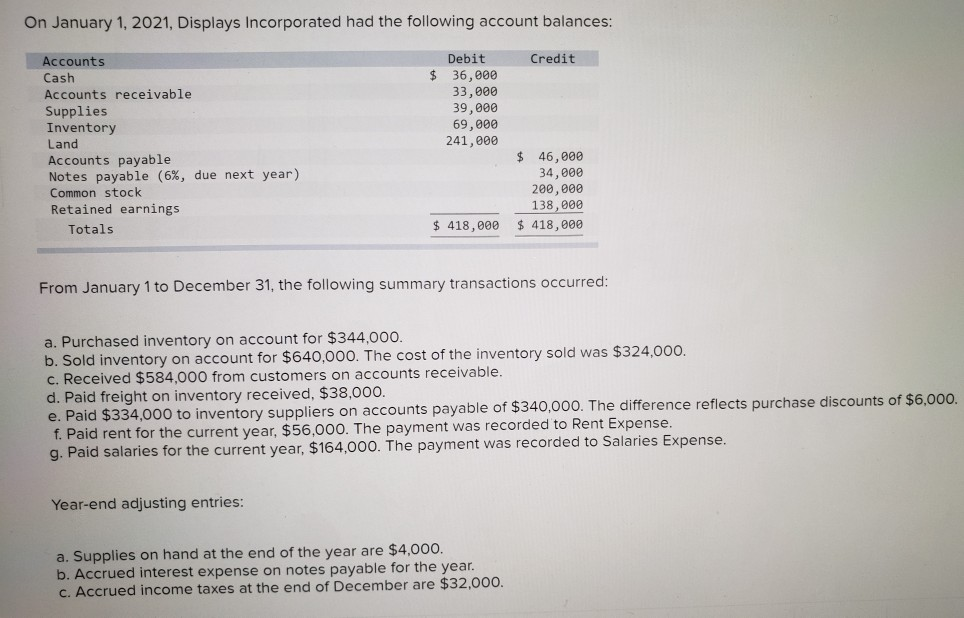

On January 1, 2021, Displays Incorporated had the following account balances: Debit Credit $ 36,000 Accounts Cash Accounts receivable Supplies Inventory Land Accounts payable Notes payable (6%, due next year) Common stock Retained earnings Totals 33,000 39,000 69,000 241,000 $ 46,000 34,000 200,000 138,000 $ 418,000 $ 418,000 From January 1 to December 31, the following summary transactions occurred: a. Purchased inventory on account for $344,000. b. Sold inventory on account for $640,000. The cost of the inventory sold was $324,000. c. Received $584,000 from customers on accounts receivable. d. Paid freight on inventory received, $38,000. e. Paid $334,000 to inventory suppliers on accounts payable of $340,000. The difference reflects purchase discounts of $6,000. f. Paid rent for the current year, $56,000. The payment was recorded to Rent Expense. g. Paid salaries for the current year, $164,000. The payment was recorded to Salaries Expense. Year-end adjusting entries: a. Supplies on hand at the end of the year are $4,000. b. Accrued interest expense on notes payable for the year. C. Accrued income taxes at the end of December are $32,000. Requirement General Journal General Ledger Trial Balance Income Statement Balance Sheet Analysis Prepare the journal entries for transactions. (If no entry is required for a particular transaction/event, select "No journal entry required" in the first account field.) View transaction list Journal entry worksheet (b) Assume Displays Incorporated $69,000 beginning balance of inventory comes from the base year with a cost index of 1.00. The cost index at the end of 2021 of 1.1. Calculate the amount the company would report for inventory using dollar-value LIFO. $ 111.900 Ending inventory using dollar-value LIFO: (c) Indicate whether each of the amounts below would be higher or lower when reporting inventory using LIFO (or dollar-value LIFO) instead of FIFO in periods of rising inventory costs and stable inventory quantities. 1. Inventory turnover ratio 2. Average days in inventory 3. Gross profit ratio Higher under LIFO Lower under LIFO Lower under LIFO

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started