Answered step by step

Verified Expert Solution

Question

1 Approved Answer

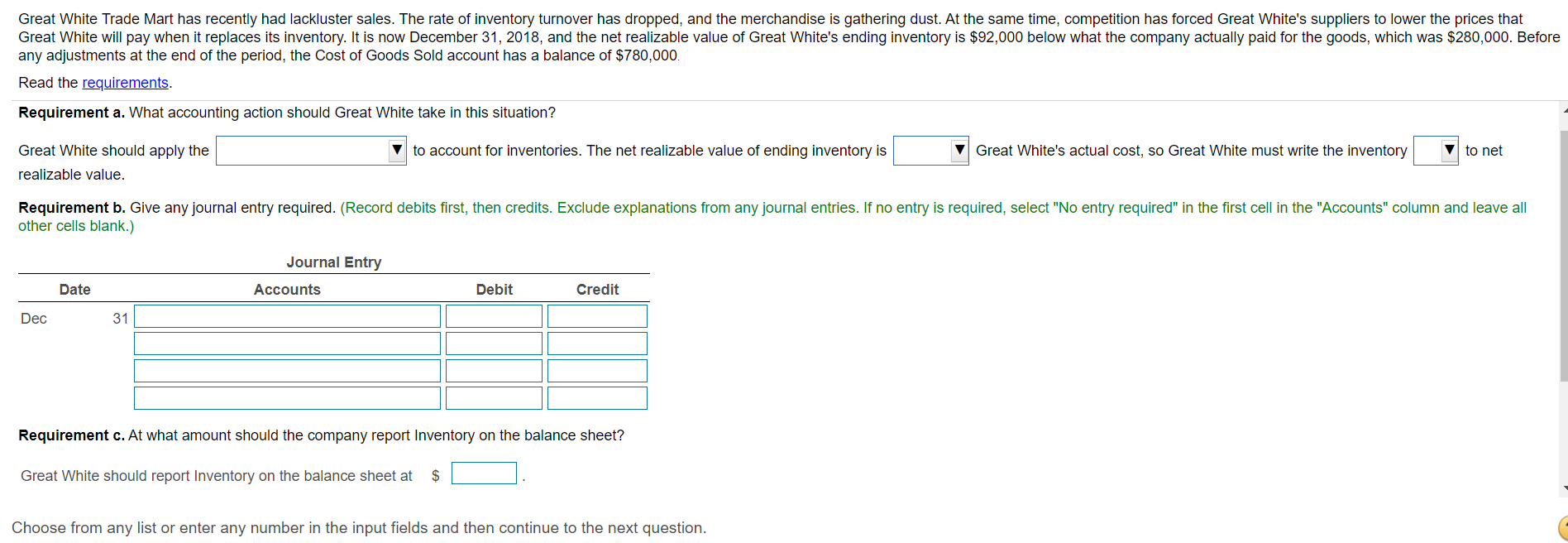

PLEASE HELP ANSWER ALL QUESTIONS Great White Trade Mart has recently had lackluster sales. The rate of inventory turnover has dropped, and the merchandise is

PLEASE HELP ANSWER ALL QUESTIONS

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Construction Safety Auditing Made Easy A Checklist Approach To OSHA Compliance

Authors: Kathleen Hess-Kosa

2nd Edition

0865879796, 978-0865879799