please help determine the chart with D/E and D/A etc

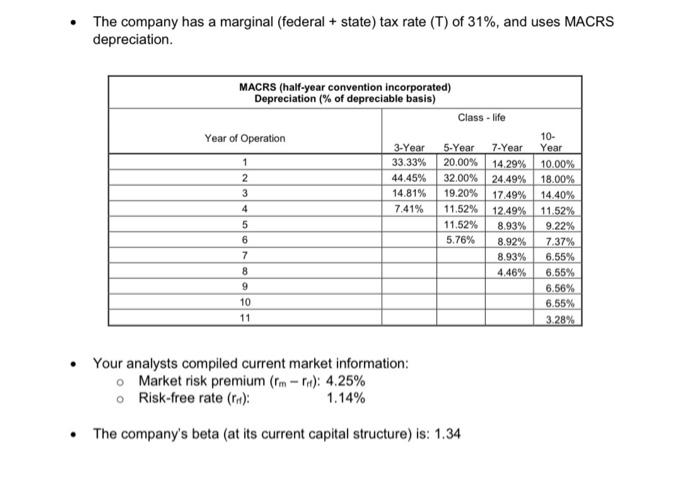

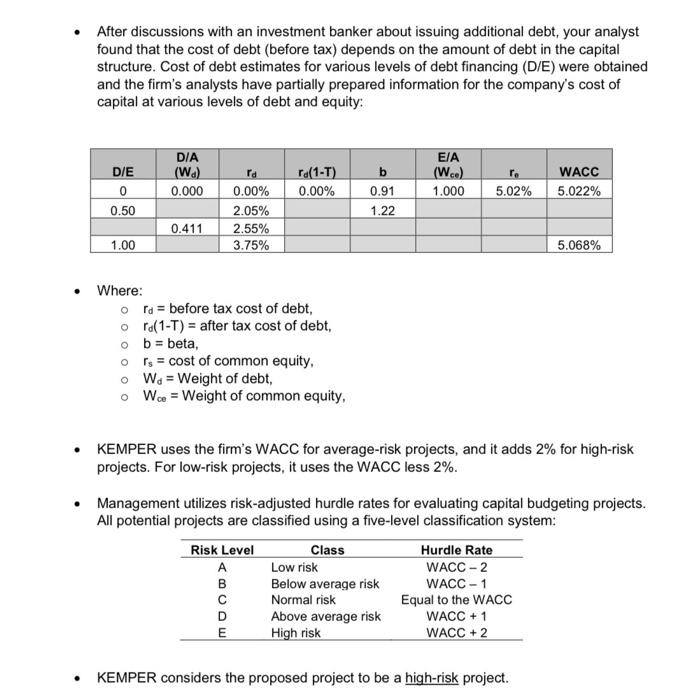

B.E. Kemper, LLC (KEMPER) is a custom parts fabricator supporting the classic auto and recreational marine industries. The company is evaluating a proposal by its Marketing department to develop one-of-a-kind, customize parts for resto-mod professionals and the hobbyist in their desire for that special, unique "new" old car/truck. This approach will require the expertise of design artists and engineers working with the restorer and the need for custom programs, computer-aided design. CNC milling equipment, and both polymer & metal 3D printing equipment Market studies indicate that the restoration market is continuing to grow and is broadening to include the newer 'classic' vehicles of the '80s and '90s. The industry consists of both professional restoration shops and many talented hobbyists. The anticipated demand is incorporated in the forecasts below. Sales Forecast: The estimate of sales revenues for this project is $1,250,000 in year 1. Sales growth of 50% is forecast for year 2, 30% for year 3, then the growth rate settles to 10% each year for years 4, 5 and 6. Sales are then stable with a growth rate of 0% (equal to year 6) in years 7 and 8. Finally, sales are expected to decline by 10% in year 9. Production cost forecasts are: o Fixed costs: $455,000 per year (a large portion of this cost is labor for the designer and engineer). Annual variable costs: 46% of sales revenue. The company will have to purchase new equipment, mentioned above, to produce the new product. The equipment, including shipping and installation, is expected to cost (t=0) $ 5,325,000 The equipment falls into the IRS 10-year class life using the MACRS depreciation method with the / year convention. (See MACRS table). If the company goes ahead with the proposed product, it will affect the company's net operating working capital. At the outset, t = 0, inventory will increase by $265,000. Accounts receivable will increase by $125,000, and accounts payable will increase by $245,000. The net operating working capital will be liquidated after the project is completed. The program (project) is planned to continue for 9 years. At the end of the project, the equipment will be salvaged (sold). The forecasts predict that the equipment can be sold then for $225,500. KEMPER - Financial Structure Current Capital Structure KEMPER has the following levels of debt and common equity (market values): o Debt: $ 4,894,300 o Equity: $7.021.700 Total Capital: $11.916,000 0 The company has a marginal (federal + state) tax rate (T) of 31%, and uses MACRS depreciation. MACRS (half-year convention incorporated) Depreciation (% of depreciable basis) Class - life Year of Operation 10- 3-Year 5-Year 7-Year Year 1 33.33% 20.00% 14.29% 10.00% 2 44.45% 32.00% 24.49% 18.00% 3 14.81% 19.20% 17.49% 14.40% 4 7.41% 11.52% 12.49% 11.52% 5 11.52% 8.93% 9.22% 6 5.76% 8.92% 7.37% 7 8.93% 6.55% 8 4.46% 6.55% 9 6.56% 10 6.55% 11 3.28% Your analysts compiled current market information: o Market risk premium (rm - P.) 4.25% o Risk-free rate (r): 1.14% The company's beta (at its current capital structure) is: 1.34 After discussions with an investment banker about issuing additional debt, your analyst found that the cost of debt (before tax) depends on the amount of debt in the capital structure. Cost of debt estimates for various levels of debt financing (D/E) were obtained and the firm's analysts have partially prepared information for the company's cost of capital at various levels of debt and equity: D/E 0 0.50 DIA (W) 0.000 re(1-T) 0.00% EIA (W) 1.000 0.91 1.22 re 5.02% ra 0.00% 2.05% 2.55% 3.75% WACC 5.022% 0.411 1.00 5.068% Where: Ora = before tax cost of debt, ord(1-T) = after tax cost of debt, ob = beta, o rs = cost of common equity, o Wa = Weight of debt, o Wc = Weight of common equity, KEMPER uses the firm's WACC for average-risk projects, and it adds 2% for high-risk projects. For low-risk projects, it uses the WACC less 2%. Management utilizes risk-adjusted hurdle rates for evaluating capital budgeting projects. All potential projects are classified using a five-level classification system: Risk Level Class Hurdle Rate Low risk WACC - 2 B Below average risk WACC - 1 Normal risk Equal to the WACC D Above average risk WACC + 1 E High risk WACC + 2 . KEMPER considers the proposed project to be a high-risk project. B.E. Kemper, LLC (KEMPER) is a custom parts fabricator supporting the classic auto and recreational marine industries. The company is evaluating a proposal by its Marketing department to develop one-of-a-kind, customize parts for resto-mod professionals and the hobbyist in their desire for that special, unique "new" old car/truck. This approach will require the expertise of design artists and engineers working with the restorer and the need for custom programs, computer-aided design. CNC milling equipment, and both polymer & metal 3D printing equipment Market studies indicate that the restoration market is continuing to grow and is broadening to include the newer 'classic' vehicles of the '80s and '90s. The industry consists of both professional restoration shops and many talented hobbyists. The anticipated demand is incorporated in the forecasts below. Sales Forecast: The estimate of sales revenues for this project is $1,250,000 in year 1. Sales growth of 50% is forecast for year 2, 30% for year 3, then the growth rate settles to 10% each year for years 4, 5 and 6. Sales are then stable with a growth rate of 0% (equal to year 6) in years 7 and 8. Finally, sales are expected to decline by 10% in year 9. Production cost forecasts are: o Fixed costs: $455,000 per year (a large portion of this cost is labor for the designer and engineer). Annual variable costs: 46% of sales revenue. The company will have to purchase new equipment, mentioned above, to produce the new product. The equipment, including shipping and installation, is expected to cost (t=0) $ 5,325,000 The equipment falls into the IRS 10-year class life using the MACRS depreciation method with the / year convention. (See MACRS table). If the company goes ahead with the proposed product, it will affect the company's net operating working capital. At the outset, t = 0, inventory will increase by $265,000. Accounts receivable will increase by $125,000, and accounts payable will increase by $245,000. The net operating working capital will be liquidated after the project is completed. The program (project) is planned to continue for 9 years. At the end of the project, the equipment will be salvaged (sold). The forecasts predict that the equipment can be sold then for $225,500. KEMPER - Financial Structure Current Capital Structure KEMPER has the following levels of debt and common equity (market values): o Debt: $ 4,894,300 o Equity: $7.021.700 Total Capital: $11.916,000 0 The company has a marginal (federal + state) tax rate (T) of 31%, and uses MACRS depreciation. MACRS (half-year convention incorporated) Depreciation (% of depreciable basis) Class - life Year of Operation 10- 3-Year 5-Year 7-Year Year 1 33.33% 20.00% 14.29% 10.00% 2 44.45% 32.00% 24.49% 18.00% 3 14.81% 19.20% 17.49% 14.40% 4 7.41% 11.52% 12.49% 11.52% 5 11.52% 8.93% 9.22% 6 5.76% 8.92% 7.37% 7 8.93% 6.55% 8 4.46% 6.55% 9 6.56% 10 6.55% 11 3.28% Your analysts compiled current market information: o Market risk premium (rm - P.) 4.25% o Risk-free rate (r): 1.14% The company's beta (at its current capital structure) is: 1.34 After discussions with an investment banker about issuing additional debt, your analyst found that the cost of debt (before tax) depends on the amount of debt in the capital structure. Cost of debt estimates for various levels of debt financing (D/E) were obtained and the firm's analysts have partially prepared information for the company's cost of capital at various levels of debt and equity: D/E 0 0.50 DIA (W) 0.000 re(1-T) 0.00% EIA (W) 1.000 0.91 1.22 re 5.02% ra 0.00% 2.05% 2.55% 3.75% WACC 5.022% 0.411 1.00 5.068% Where: Ora = before tax cost of debt, ord(1-T) = after tax cost of debt, ob = beta, o rs = cost of common equity, o Wa = Weight of debt, o Wc = Weight of common equity, KEMPER uses the firm's WACC for average-risk projects, and it adds 2% for high-risk projects. For low-risk projects, it uses the WACC less 2%. Management utilizes risk-adjusted hurdle rates for evaluating capital budgeting projects. All potential projects are classified using a five-level classification system: Risk Level Class Hurdle Rate Low risk WACC - 2 B Below average risk WACC - 1 Normal risk Equal to the WACC D Above average risk WACC + 1 E High risk WACC + 2 . KEMPER considers the proposed project to be a high-risk project