Answered step by step

Verified Expert Solution

Question

1 Approved Answer

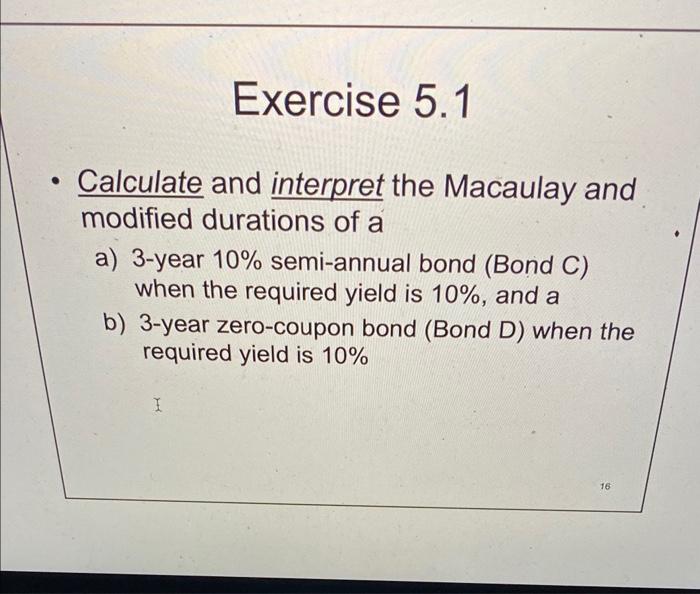

Please help me ASAP Calculate and interpret the Macaulay and modified durations of a a) 3-year 10% semi-annual bond (Bond C) when the required yield

Please help me ASAP

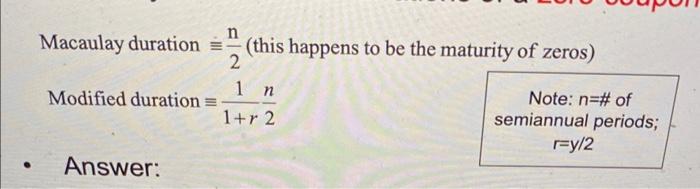

Calculate and interpret the Macaulay and modified durations of a a) 3-year 10\% semi-annual bond (Bond C) when the required yield is 10%, and a b) 3-year zero-coupon bond (Bond D) when the required yield is 10% Macaulay duration 2n (this happens to be the maturity of zeros) Modified duration 1+r12n Note: n=# of semiannual periods; - Answer: r=y/2

Calculate and interpret the Macaulay and modified durations of a a) 3-year 10\% semi-annual bond (Bond C) when the required yield is 10%, and a b) 3-year zero-coupon bond (Bond D) when the required yield is 10% Macaulay duration 2n (this happens to be the maturity of zeros) Modified duration 1+r12n Note: n=# of semiannual periods; - Answer: r=y/2

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Issues In Behavioral Finance

Authors: Simon Grima

1st Edition

1787698823, 978-1787698826