Please help me only with question #2

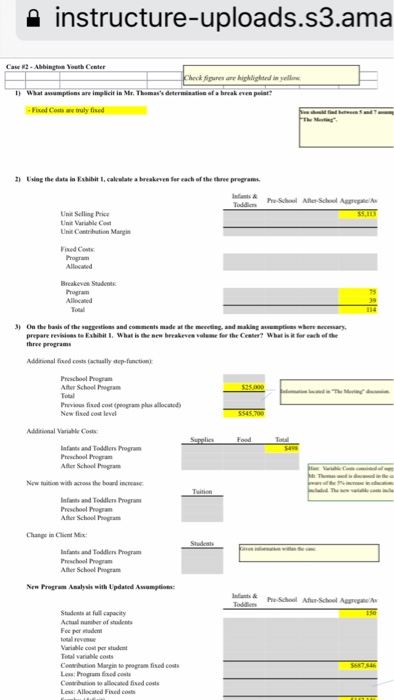

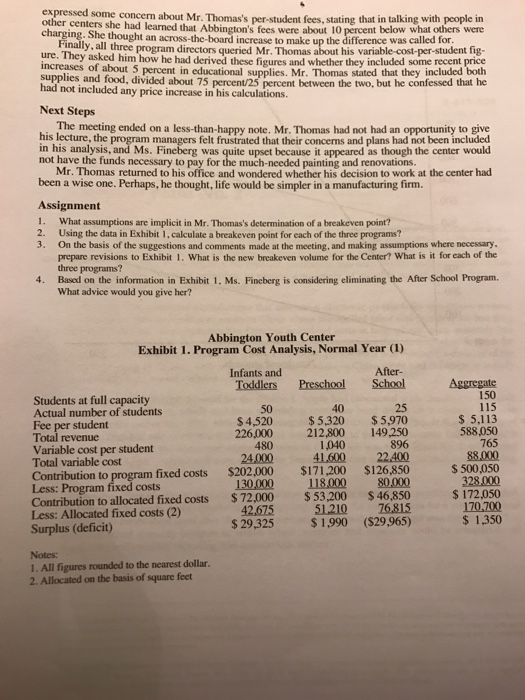

expressed some concern about Mr. Thomas's per-student fees, stating that in talking with people in other she had learned that Abbington's fees were about 10 percent below what others Centers She thought an across-the-board increase to make up the difference was called for. Finally all three program directors queried about his variable-cost-per-student fig- ure. They him how he had derived these figures and whether they included some recent price of about 5 percent in educational supplies. Mr. Thomas stated that they included both supplies and food, divided about 75 percent/25 percent between the two.but he confessed that he had not any price increase in his calculations. Next Steps The meeting ended on a less-than-happy note. Mr.Thomas had not had an opportunity to give his lecture, the program managers felt frustrated that their concerms and plans had not been included was quite because it appeared as though the center would not have the funds necessary to pay for the much-needed and renovations Mr. Thomas returned to his and whether his at the center had been a wise one. Perhaps, he thought life would be simpler in a manufacturing firm. Assignment 1. What assumptions are implicit in Mr. Thomas's determination of a breakeven point? 2. Using the data in Exhibit 1, a breakeven point for each of the three programs? calculate 3. On the basis of the suggestions and comments made at the meeting, and making assumptions where necessary. prepare revisions to Exhibit 1. What is the new breakeven volume for the Center? What is it for each of the 4. Based on the information in Exhibit 1. Ms. Fineberg is considering eliminating the After School Program. What advice would you give her? Abbington Youth Center Exhibit 1. Program Cost Analysis, Normal Year (i) After Infants and 150 Students at full capacity 115 Actual number of students 5,113 5320 5970 $4,520 Fee per student 588,050 226.000 212800 149.250 Total revenue 765 1,040 896 Variable cost per student 41600 22400 Total variable cost 500,050 Contribution to program fixed costs $202,000 $171.200 $126,850 1300000 llE 0000 800000 172,050 Contribution to allocated fixed costs 72,000 53,200 46,850 51.210 16.815 Less: Allocated fixed costs (2) 1.350 1990 ($29,965) 29,325 Surplus (deficit) l. All figures rounded to the nearest dollar. 2. Allocated on the basis of square feet expressed some concern about Mr. Thomas's per-student fees, stating that in talking with people in other she had learned that Abbington's fees were about 10 percent below what others Centers She thought an across-the-board increase to make up the difference was called for. Finally all three program directors queried about his variable-cost-per-student fig- ure. They him how he had derived these figures and whether they included some recent price of about 5 percent in educational supplies. Mr. Thomas stated that they included both supplies and food, divided about 75 percent/25 percent between the two.but he confessed that he had not any price increase in his calculations. Next Steps The meeting ended on a less-than-happy note. Mr.Thomas had not had an opportunity to give his lecture, the program managers felt frustrated that their concerms and plans had not been included was quite because it appeared as though the center would not have the funds necessary to pay for the much-needed and renovations Mr. Thomas returned to his and whether his at the center had been a wise one. Perhaps, he thought life would be simpler in a manufacturing firm. Assignment 1. What assumptions are implicit in Mr. Thomas's determination of a breakeven point? 2. Using the data in Exhibit 1, a breakeven point for each of the three programs? calculate 3. On the basis of the suggestions and comments made at the meeting, and making assumptions where necessary. prepare revisions to Exhibit 1. What is the new breakeven volume for the Center? What is it for each of the 4. Based on the information in Exhibit 1. Ms. Fineberg is considering eliminating the After School Program. What advice would you give her? Abbington Youth Center Exhibit 1. Program Cost Analysis, Normal Year (i) After Infants and 150 Students at full capacity 115 Actual number of students 5,113 5320 5970 $4,520 Fee per student 588,050 226.000 212800 149.250 Total revenue 765 1,040 896 Variable cost per student 41600 22400 Total variable cost 500,050 Contribution to program fixed costs $202,000 $171.200 $126,850 1300000 llE 0000 800000 172,050 Contribution to allocated fixed costs 72,000 53,200 46,850 51.210 16.815 Less: Allocated fixed costs (2) 1.350 1990 ($29,965) 29,325 Surplus (deficit) l. All figures rounded to the nearest dollar. 2. Allocated on the basis of square feet