Answered step by step

Verified Expert Solution

Question

1 Approved Answer

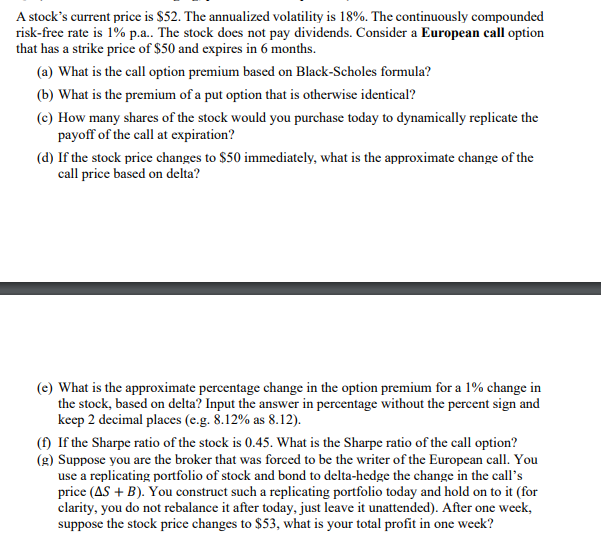

Please help me solve ( c ) to ( e ) A stock's current price is $ 5 2 . The annualized volatility is 1

Please help me solve c to eA stock's current price is $ The annualized volatility is The continuously compounded

riskfree rate is pa The stock does not pay dividends. Consider a European call option

that has a strike price of $ and expires in months.

a What is the call option premium based on BlackScholes formula?

b What is the premium of a put option that is otherwise identical?

c How many shares of the stock would you purchase today to dynamically replicate the

payoff of the call at expiration?

d If the stock price changes to $ immediately, what is the approximate change of the

call price based on delta?

e What is the approximate percentage change in the option premium for a change in

the stock, based on delta? Input the answer in percentage without the percent sign and

keep decimal places eg as

f If the Sharpe ratio of the stock is What is the Sharpe ratio of the call option?

g Suppose you are the broker that was forced to be the writer of the European call. You

use a replicating portfolio of stock and bond to deltahedge the change in the call's

price You construct such a replicating portfolio today and hold on to it for

clarity, you do not rebalance it after today, just leave it unattended After one week,

suppose the stock price changes to $ what is your total profit in one week?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

8th Edition

0077606779, 978-0697789945