Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please help me with this and there is detailed guideline which can help to solve it quickly!!! Thank you please provide detailed explaination Berry Case-

Please help me with this and there is detailed guideline which can help to solve it quickly!!!

Please help me with this and there is detailed guideline which can help to solve it quickly!!!

Thank you please provide detailed explaination

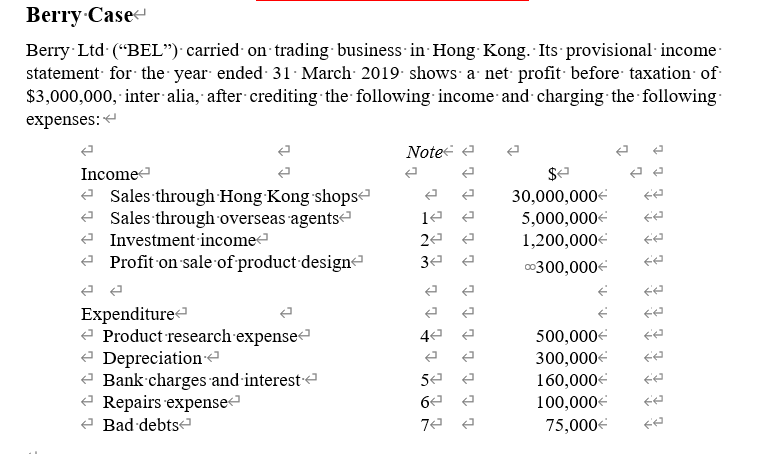

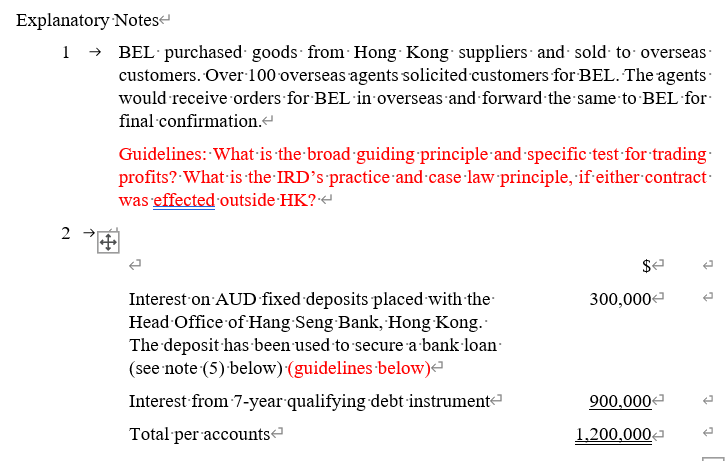

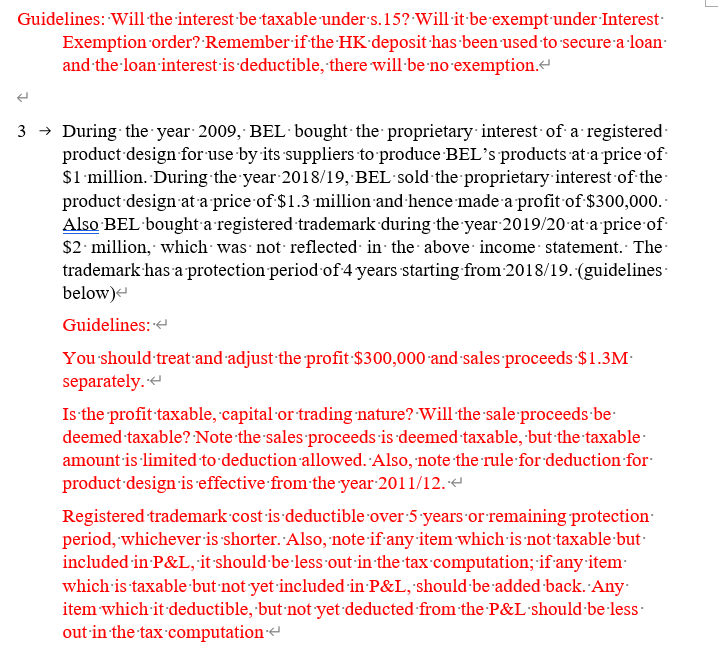

Berry Case- Berry Ltd (BEL). carried on-trading business in Hong Kong. Its provisional income statement for the year ended 31 March 2019 shows a net profit before taxation of $3,000,000, inter alia, after crediting the following income and charging the following expenses: Note e Income Sales through Hong Kong shops 30,000,000 Sales through overseas agents 5,000,000 Investment income 2 e 1,200,000 Profit on sale of product design 32 e 00300,000 t tt 14 Expenditure Product research expense- Depreciation Bank charges and interest Repairs expense Bad debts ttttt 5 500,000 300,000 160,000 100,000+ 75,000 64 76 Guidelines: Will the interest be taxable unders.152-Will-it-be-exempt under Interest: Exemption order? Remember if the HK deposit has been used to secure-a-loan and the loan interest is deductible, there will be no exemption. e 3 During the year 2009, BEL bought the proprietary interest of a registered product design for use by its suppliers to produce BEL's products at a price of $1 million. During the year 2018/19, BEL sold the proprietary interest of the product design at a price of $1.3 million and hence made a profit of $300,000. Also BEL bought-a-registered trademark during the year 2019/20-at a price of $2 million, which was not reflected in the above income statement. The trademark has a protection period of 4 years starting from 2018/19. (guidelines below) Guidelines: You should treat and adjust the profit-$300,000 and sales proceeds $1.3M separately. Is the profit taxable, capital or trading nature? Will the sale proceeds.be deemed taxable? Note the sales proceeds is deemed taxable, but the taxable amount is limited to deduction allowed. Also, note the rule for deduction for product design is effective from the year 2011/12.4 Registered trademark cost is deductible over 5 years or remaining protection period, whichever is shorter. Also, note-if any item which is not taxable but included-in-P&L, it should-be-less out in the tax computation; if any item which is taxable but not yet included-in-P&L, should be added back. Any item which-it deductible, but not yet deducted from the P&L should be less out in the tax computation 4 Please also note: the deduction for registered-mark-should start from the year of acquisition, 'over-5 years of remaining protection year:(starting from the year of acquisition. Be careful for the year of acquisition in the case, and the remaining protection period starting from the year of acquisition. 4 C 4 The product research expense included $150,000 for new research equipment. Guidelines: 'Note the enhanced deduction for R&D, may-it apply or NOT. 5 20,000 C 140,000 t Bank charges on ordinary trading transactions Interest on bank loan* -secured by a deposit with Hang Seng Bank (see-note-2 above) (guidelines below) Total per accounts 160,000 *The bank loan was used to buy trading stock. Guidelines: Was it for the purpose of trade? Any condition in s. 16(2) being satisfied?- Any restrictions? 6 The repairs expense of $100,000 was for initial repairs to a second-hand- packing machine which was acquired during the year. The expense was for the purpose to put the machine back to operable condition for obtaining the relevant license from the government. (Guidelines: was the repairs expense capital nature?) 7 Write-off of a staff loan* (5%-interest and 95% principal) 20,000 Bad debts recovered (trade debts written off in the year 2018/19) (8,000) Provision --5-% on total trade debtors' balance 10,000 -on-specified trade debtors 53,000 Total per accounts 75,000 The loan was provided to the staff's bank account in Hong Kong. Guidelines: Was the staff loan, interest and principal, a trade debt taxed before? Was it lent in ordinary course of money lending business?-- 8 Depreciation allowance agreed by the Inland Revenue Department for the year was $200,000 Guidelines: Adjust the accounting depreciation and depreciation allowance separately 1 Required *(a) Calculate the profits tax payable by BEL for the year of assessment-2018/19, ignore provisional tax. Guidelines:-MUST follow the format in the lecture notes. State-the-title, tax rates, tax reduction clearly. (11 marks) (b) Explain your profits tax treatments for the following items: (1)>Sales through overseas agents $5,000,000 (3 marks) (2)>Interest from fixed term bank deposit interest $300,000 (3 marks) (3)>Sales proceeds of the registered product design $1,300,000 (2 marks) (4)>Registered trademark acquisition cost $2,000,000 (2 marks) (5)>Interest on bank loan $140,000 (3 marks) (6)>Write-off of staff-loan $20,000 (3 marks) (7)>Initial repairs expense of the second-hand packing machine $100,000 (3 marks) Guidelines: Your explanation should include: A.~Rules: Relevant provision in the IRO, DIPN, case-law (summarising in brief, don't copy from notes, you don't need to copy the whole story of a case, just state the principle and case-name-in-sufficient- B.-Analysing the tax position-with-reference the case-facts and the relevant rules you stated in (A) above. C. Don'ts: Remember, don't just state-it is taxable or deductible. It is also wrong to just mention, say under s.14 it is not taxable. YOU must explain by using A+B:I: mentioned above. (sub-total 19 marks) Total (30 marks) Berry Case- Berry Ltd (BEL). carried on-trading business in Hong Kong. Its provisional income statement for the year ended 31 March 2019 shows a net profit before taxation of $3,000,000, inter alia, after crediting the following income and charging the following expenses: Note e Income Sales through Hong Kong shops 30,000,000 Sales through overseas agents 5,000,000 Investment income 2 e 1,200,000 Profit on sale of product design 32 e 00300,000 t tt 14 Expenditure Product research expense- Depreciation Bank charges and interest Repairs expense Bad debts ttttt 5 500,000 300,000 160,000 100,000+ 75,000 64 76 Guidelines: Will the interest be taxable unders.152-Will-it-be-exempt under Interest: Exemption order? Remember if the HK deposit has been used to secure-a-loan and the loan interest is deductible, there will be no exemption. e 3 During the year 2009, BEL bought the proprietary interest of a registered product design for use by its suppliers to produce BEL's products at a price of $1 million. During the year 2018/19, BEL sold the proprietary interest of the product design at a price of $1.3 million and hence made a profit of $300,000. Also BEL bought-a-registered trademark during the year 2019/20-at a price of $2 million, which was not reflected in the above income statement. The trademark has a protection period of 4 years starting from 2018/19. (guidelines below) Guidelines: You should treat and adjust the profit-$300,000 and sales proceeds $1.3M separately. Is the profit taxable, capital or trading nature? Will the sale proceeds.be deemed taxable? Note the sales proceeds is deemed taxable, but the taxable amount is limited to deduction allowed. Also, note the rule for deduction for product design is effective from the year 2011/12.4 Registered trademark cost is deductible over 5 years or remaining protection period, whichever is shorter. Also, note-if any item which is not taxable but included-in-P&L, it should-be-less out in the tax computation; if any item which is taxable but not yet included-in-P&L, should be added back. Any item which-it deductible, but not yet deducted from the P&L should be less out in the tax computation 4 Please also note: the deduction for registered-mark-should start from the year of acquisition, 'over-5 years of remaining protection year:(starting from the year of acquisition. Be careful for the year of acquisition in the case, and the remaining protection period starting from the year of acquisition. 4 C 4 The product research expense included $150,000 for new research equipment. Guidelines: 'Note the enhanced deduction for R&D, may-it apply or NOT. 5 20,000 C 140,000 t Bank charges on ordinary trading transactions Interest on bank loan* -secured by a deposit with Hang Seng Bank (see-note-2 above) (guidelines below) Total per accounts 160,000 *The bank loan was used to buy trading stock. Guidelines: Was it for the purpose of trade? Any condition in s. 16(2) being satisfied?- Any restrictions? 6 The repairs expense of $100,000 was for initial repairs to a second-hand- packing machine which was acquired during the year. The expense was for the purpose to put the machine back to operable condition for obtaining the relevant license from the government. (Guidelines: was the repairs expense capital nature?) 7 Write-off of a staff loan* (5%-interest and 95% principal) 20,000 Bad debts recovered (trade debts written off in the year 2018/19) (8,000) Provision --5-% on total trade debtors' balance 10,000 -on-specified trade debtors 53,000 Total per accounts 75,000 The loan was provided to the staff's bank account in Hong Kong. Guidelines: Was the staff loan, interest and principal, a trade debt taxed before? Was it lent in ordinary course of money lending business?-- 8 Depreciation allowance agreed by the Inland Revenue Department for the year was $200,000 Guidelines: Adjust the accounting depreciation and depreciation allowance separately 1 Required *(a) Calculate the profits tax payable by BEL for the year of assessment-2018/19, ignore provisional tax. Guidelines:-MUST follow the format in the lecture notes. State-the-title, tax rates, tax reduction clearly. (11 marks) (b) Explain your profits tax treatments for the following items: (1)>Sales through overseas agents $5,000,000 (3 marks) (2)>Interest from fixed term bank deposit interest $300,000 (3 marks) (3)>Sales proceeds of the registered product design $1,300,000 (2 marks) (4)>Registered trademark acquisition cost $2,000,000 (2 marks) (5)>Interest on bank loan $140,000 (3 marks) (6)>Write-off of staff-loan $20,000 (3 marks) (7)>Initial repairs expense of the second-hand packing machine $100,000 (3 marks) Guidelines: Your explanation should include: A.~Rules: Relevant provision in the IRO, DIPN, case-law (summarising in brief, don't copy from notes, you don't need to copy the whole story of a case, just state the principle and case-name-in-sufficient- B.-Analysing the tax position-with-reference the case-facts and the relevant rules you stated in (A) above. C. Don'ts: Remember, don't just state-it is taxable or deductible. It is also wrong to just mention, say under s.14 it is not taxable. YOU must explain by using A+B:I: mentioned above. (sub-total 19 marks) Total (30 marks)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cornerstones of Financial and Managerial Accounting

Authors: Rich Jones, Mowen, Hansen, Heitger

1st Edition

9780538751292, 324787359, 538751290, 978-0324787351