Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please help! Q 2, Q 3 and Q 4 combined: You are given the following information. The spot exchange rate today for the number of

Please help!

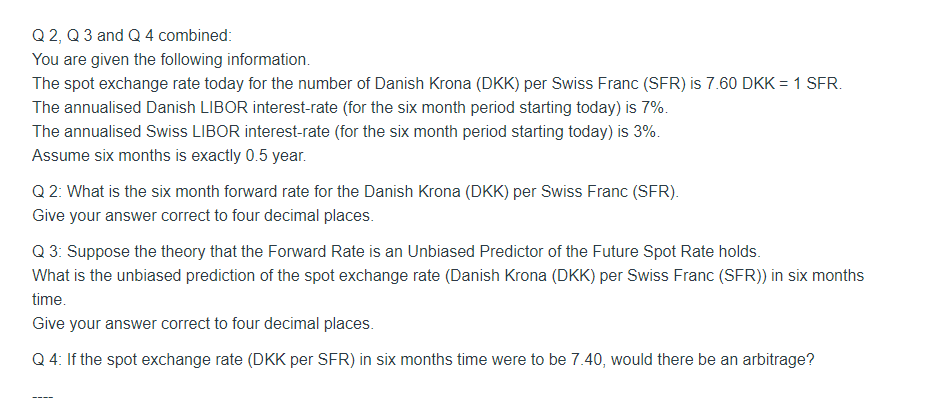

Q 2, Q 3 and Q 4 combined: You are given the following information. The spot exchange rate today for the number of Danish Krona (DKK) per Swiss Franc (SFR) is 7.60 DKK =1SFR. The annualised Danish LIBOR interest-rate (for the six month period starting today) is 7%. The annualised Swiss LIBOR interest-rate (for the six month period starting today) is 3%. Assume six months is exactly 0.5 year. Q 2: What is the six month forward rate for the Danish Krona (DKK) per Swiss Franc (SFR). Give your answer correct to four decimal places. Q 3: Suppose the theory that the Forward Rate is an Unbiased Predictor of the Future Spot Rate holds. What is the unbiased prediction of the spot exchange rate (Danish Krona (DKK) per Swiss Franc (SFR)) in six months time. Give your answer correct to four decimal places. Q 4: If the spot exchange rate (DKK per SFR) in six months time were to be 7.40, would there be an arbitrage

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started