Please Help!

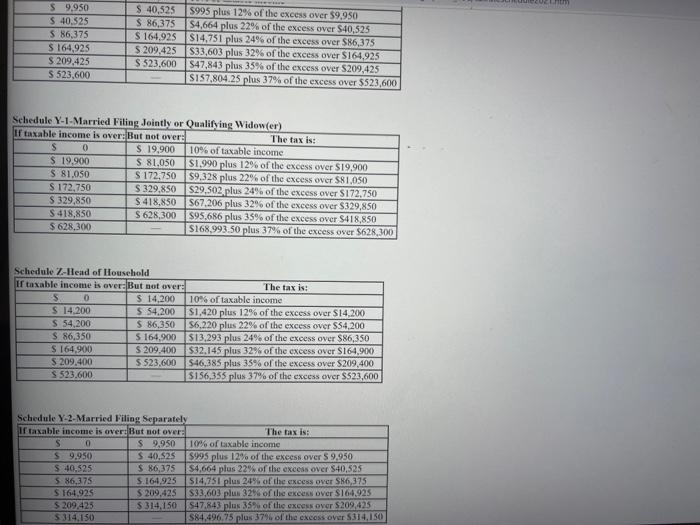

Required information {The following information applies to the questions displayed below.) Demarco and Janine Jackson have been married for 20 years and have four children (no children under age 6 at year- end) who qualify as their dependents (Damarcus, Jasmine, Michael, and Candice). The couple received salary income of $102,100 and qualified business income of $10,000 from an investment in a partnership, and they sold their home this year. They initially purchased the home three years ago for $242,000 and they sold it for $355,000. The gain on the sale qualified for the exclusion from the sale of a principal residence. The Jacksons incurred $18,600 of itemized deductions (no charitable contributions), and they had $1,000 withheld from their paychecks for federal taxes. They are also allowed to claim a child tax credit for each of their children. However, because Candice was 18 years of age at year end, the Jacksons may claim a child tax credit for other qualifying dependents for Candice (Use the tax rate schedules) c. What would their taxable income be if their itemized deductions totale $32,200 instead of $18,600? Description Amount (1) Gross income (2) For AGI deductions (3) Adjusted gross income (4) Standard deduction (5) Itemized deductions (7) Deduction for qualified business income (8) Total deductions from AGI Taxable income e. Assume the original facts but now suppose the Jacksons also incurred a loss of $7,100 on the sale of some of their investment assets. What effect does the $7,100 loss have on their taxable income? t. Assume the original facts but now suppose the Jacksons own investments that appreciated by $10,000 during the year. The Jacksons believe the investments will continue to appreciate, so they did not sell the investments during this year. What is the Jacksons'taxable income? The come . What would their taxable income be if they had $o itemized deductions and $8,100 of for AGI deductions? Amount Description (1) Gross income (2) For AGI deductions (3) Adjusted gross income (4) Standard deduction (5) Itemized deductions (7) Deduction for qualified business income (8) Total deductions from AGI Taxable income e. Assume the original facts but now suppose the Jacksons also incurred a loss of $7100 on the sale of some of their investment assets. What effect does the $7,100 loss have on their taxable income? Com S 9.950 S 40.525 $ 86,375 S 164,925 S 209,425 S 523,600 $ 40,525 5995 plus 12% of the excess over $9.950 $ 86,375 S4,664 plus 22% of the excess over $40.525 $164.925 S14,751 plus 24% of the excess over $86,375 $ 209,425 $33,603 plus 32% of the excess over $164.925 $ 523,600 S47,843 plus 35% of the excess over $209,425 $157,804.25 plus 37% of the excess over $523,600 Schedule Y-1. Married Filing Jointly or Qualifying Widow(er) If taxable income is over: But not over: The tax is: $ 0 $ 19,900 10% of taxable income $ 19.900 S 81,050 S1.990 plus 12% of the excess over $19,900 S 81.050 S 172.750 $9,328 plus 22% of the excess over $81,050 S 172,750 S 329,850 $29.502 plus 24% of the excess over $172.750 S 329,850 $ 418,850 $67,206 plus 32% of the excess over $329,850 $ 418,850 S628,300 $95.686 plus 35% of the excess over $418,850 $ 628,300 $168.993.50 plus 37% of the excess over $628,300 Schedule Z-Head of Household Ir taxable income is over:But not over: The tax is: 5 0 $ 14,200 10% of taxable income S 14.200 S 54.200 $1,420 plus 12% of the excess over $14,200 $ 54,200 $ 86,350 S6.220 plus 22% of the excess over $54,200 $ 86,350 5 164.900 $13,293 plus 24% of the excess over $86,350 $164.900 S 209.400 $32.145 plus 32% of the excess over $164.900) $ 209,400 $ 523,600 $46,385 plus 35% of the excess over $209,400 S 523.600 $156,355 plus 37% of the excess over $523,600 Schedule Y-2-Married Filing Separately If taxable income is over But not over: The tax is: S 0 $ 9,950 10% of taxable income $9.950 $ 40.525 S995 plus 12% of the excess over $9.950 $ 40.525 $ 86,375 $4,664 plus 22% of the excess over $40,525 5 86,375 5.164.925 514,751 plus 24% of the excess over $86,375 S 164.925 $ 209,425 $33,603 plus 32% of the excess over $164.925 $ 209,425 $314,150 $47.843 plus 35% of the excess over $209,425 $314.150 $84.496.75 plus 37% of the excess over 5314,150