Answered step by step

Verified Expert Solution

Question

1 Approved Answer

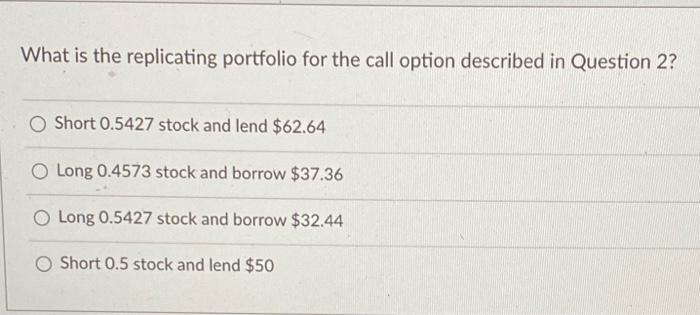

Please just answer Q3 What is the replicating portfolio for the call option described in Question 2? Short 0.5427 stock and lend $62.64 Long 0.4573

Please just answer Q3

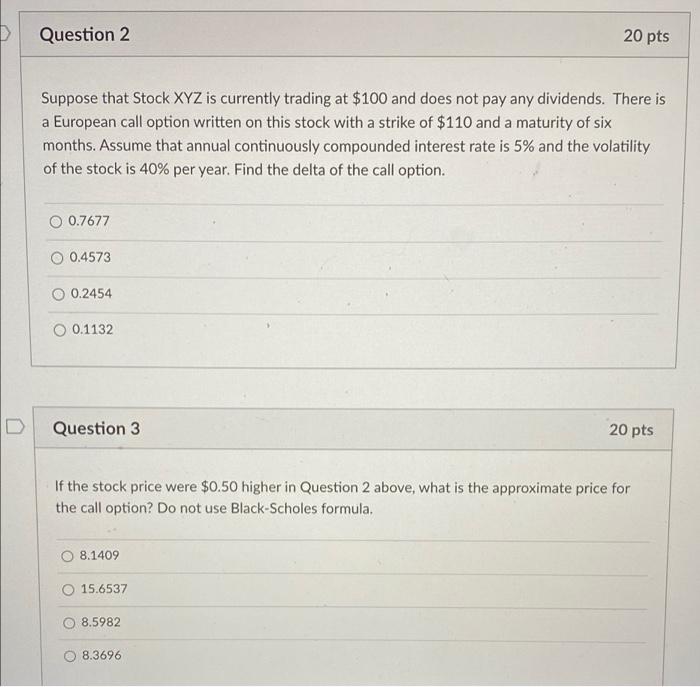

What is the replicating portfolio for the call option described in Question 2? Short 0.5427 stock and lend $62.64 Long 0.4573 stock and borrow $37.36 Long 0.5427 stock and borrow $32.44 Short 0.5 stock and lend $50 Question 2 20 pts Suppose that Stock XYZ is currently trading at $100 and does not pay any dividends. There is a European call option written on this stock with a strike of $110 and a maturity of six months. Assume that annual continuously compounded interest rate is 5% and the volatility of the stock is 40% per year. Find the delta of the call option. O 0.7677 0.4573 O 0.2454 O 0.1132 Question 3 20 pts If the stock price were $0.50 higher in Question 2 above, what is the approximate price for the call option? Do not use Black-Scholes formula, 8.1409 15.6537 8.5982 O 8.3696 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Operations

Authors: Charles Finley

1st Edition

1491292423, 978-1491292426