Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please please do this question urgently and perfectly. I will give positive rating if you solve this urgently and perfectly. highlight the main answer n

please please do this question urgently and perfectly. I will give positive rating if you solve this urgently and perfectly. highlight the main answer

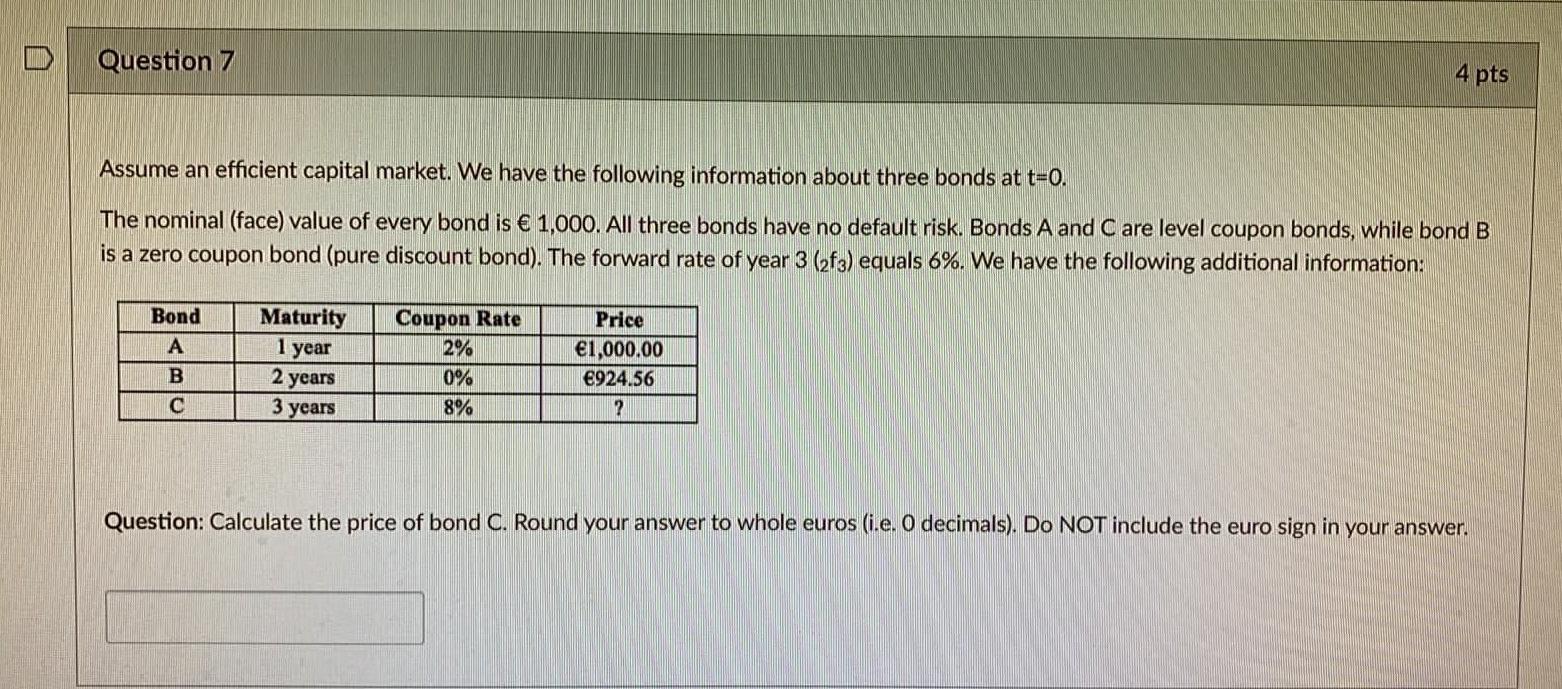

n Question 7 4 pts Assume an efficient capital market. We have the following information about three bonds at t=0. The nominal (face) value of every bond is 1,000. All three bonds have no default risk. Bonds A and Care level coupon bonds, while bond B is a zero coupon bond (pure discount bond). The forward rate of year 3 (zf3) equals 6%. We have the following additional information: Maturity 1 year Coupon Rate 2% Bond B C Price 1,000.00 924.56 ? 0% 2 years 3 years 8% Question: Calculate the price of bond C. Round your answer to whole euros (i.e. O decimals). Do NOT include the euro sign in yourStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Basel II Implementation Chapter 4 Pillar II Challenges And Dealing With Procyclicality

Authors: Bogie Ozdemir, Peter Miu

1st Edition

0071731784