Question

PLEASE READ INFO BELOW AND SEE PHOTO ATTACHED. Consider a mutual fund that is currently investing only in Toyota Motor Corporations stock (Ticker: TM). The

PLEASE READ INFO BELOW AND SEE PHOTO ATTACHED.

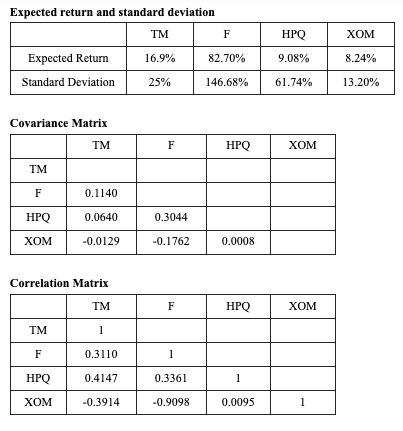

Consider a mutual fund that is currently investing only in Toyota Motor Corporations stock (Ticker: TM). The fund manager has collected information of another three stocks. The fund manager wants to combine TM with another stock and reduce the portfolios risk using diversification.

Assume that the fund manager invests 60% of the assets in TM and 40% in XOM to form the optimal risky portfolio. Then the fund manager wants to further combine the risky portfolio of two stocks (i.e., 60% in TM and 40% in XOM) with risk-free assets. However, the risk-free rates of lending and borrowing are different. The fund manager can invest in risk-free assets with 2% return. When she borrows, the risk-free rate is 5%. Suppose her risk aversion index is A=5. Then the optimal weight for the risk-free asset is _____%. (For example, if the optimal weight is 60%, then put "60" below. Keep two digits after decimal.)

What is the optimal weight for the risk-free asset?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit And Assurance Principles And Practices In Singapore

Authors: Dr Ernest Kan

5th Edition

9814838136, 978-9814838139