Answered step by step

Verified Expert Solution

Question

1 Approved Answer

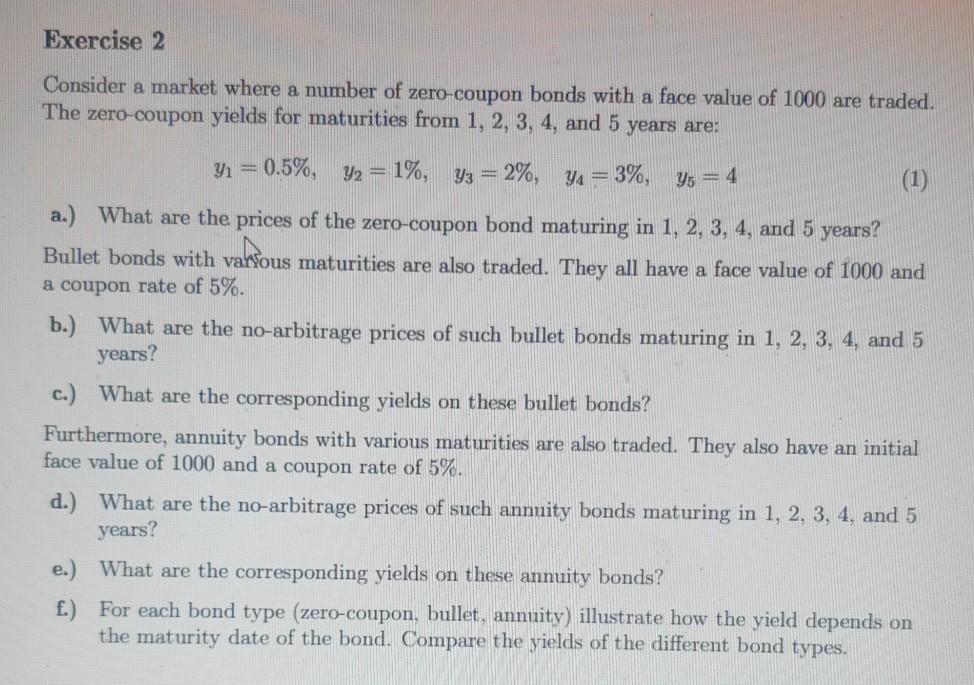

Please show all steps Exercise 2 Consider a market where a number of zero-coupon bonds with a face value of 1000 are traded. The zero-coupon

Please show all steps

Exercise 2 Consider a market where a number of zero-coupon bonds with a face value of 1000 are traded. The zero-coupon yields for maturities from 1, 2, 3, 4, and 5 years are: Ys = 4 y = 0.5%, y2 = 1%, y3 = 2%, YA = 3%, a.) What are the prices of the zero-coupon bond maturing in 1, 2, 3, 4, and 5 years? Bullet bonds with varfous maturities are also traded. They all have a face value of 1000 and valou a coupon rate of 5%. b.) What are the no-arbitrage prices of such bullet bonds maturing in 1, 2, 3, 4, and 5 years? c.) What are the corresponding yields on these bullet bonds? Furthermore, annuity bonds with various maturities are also traded. They also have an initial face value of 1000 and a coupon rate of 5%. d.) What are the no-arbitrage prices of such annuity bonds maturing in 1, 2, 3, 4, and 5 years? e.) What are the corresponding yields on these anmity bonds? f.) For each bond type (zero-coupon, bullet, annuity) illustrate how the yield depends on the maturity date of the bond. Compare the yields of the different bond typesStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Market Analysis And Behaviour The Adaptive Preference Hypothesis

Authors: Emil Dinga, Camelia Oprean Stan, Cristina Roxana Tinisescu, Vasile Brctian, Gabriela Mariana Ionescu

1st Edition

1032255161, 1000609731, 9781032255163, 9781000609738