Answered step by step

Verified Expert Solution

Question

1 Approved Answer

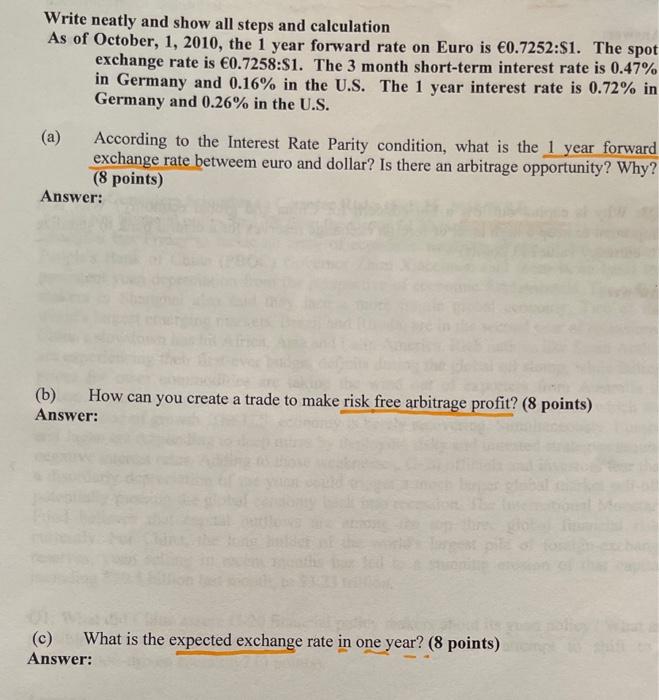

please show everyone calculated number. thanks Write neatly and show all steps and calculation As of October, 1, 2010, the 1 year forward rate on

please show everyone calculated number.

Write neatly and show all steps and calculation As of October, 1, 2010, the 1 year forward rate on Euro is 0.7252:$1. The spot exchange rate is 0.7258:31. The 3 month short-term interest rate is 0.47% in Germany and 0.16% in the U.S. The 1 year interest rate is 0.72% in Germany and 0.26% in the U.S. (a) According to the Interest Rate Parity condition, what is the 1 year forward exchange rate betweem euro and dollar? Is there an arbitrage opportunity? Why? (8 points) Answer: (b) How can you create a trade to make risk free arbitrage profit? (8 points) Answer: (c) What is the expected exchange rate in one year? (8 points) thanks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

NFT For Beginners How To Create Buy Sell And Make A Living Off Of Digital Art And Cryptocurrencies

Authors: Greg Middleton

1st Edition

B0CCCVRTTN, 979-8853522039