Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please show your workings clearly Answer the following questions on option pricing. Suppose that a call option and a put option have the same characteristics

Please show your workings clearly

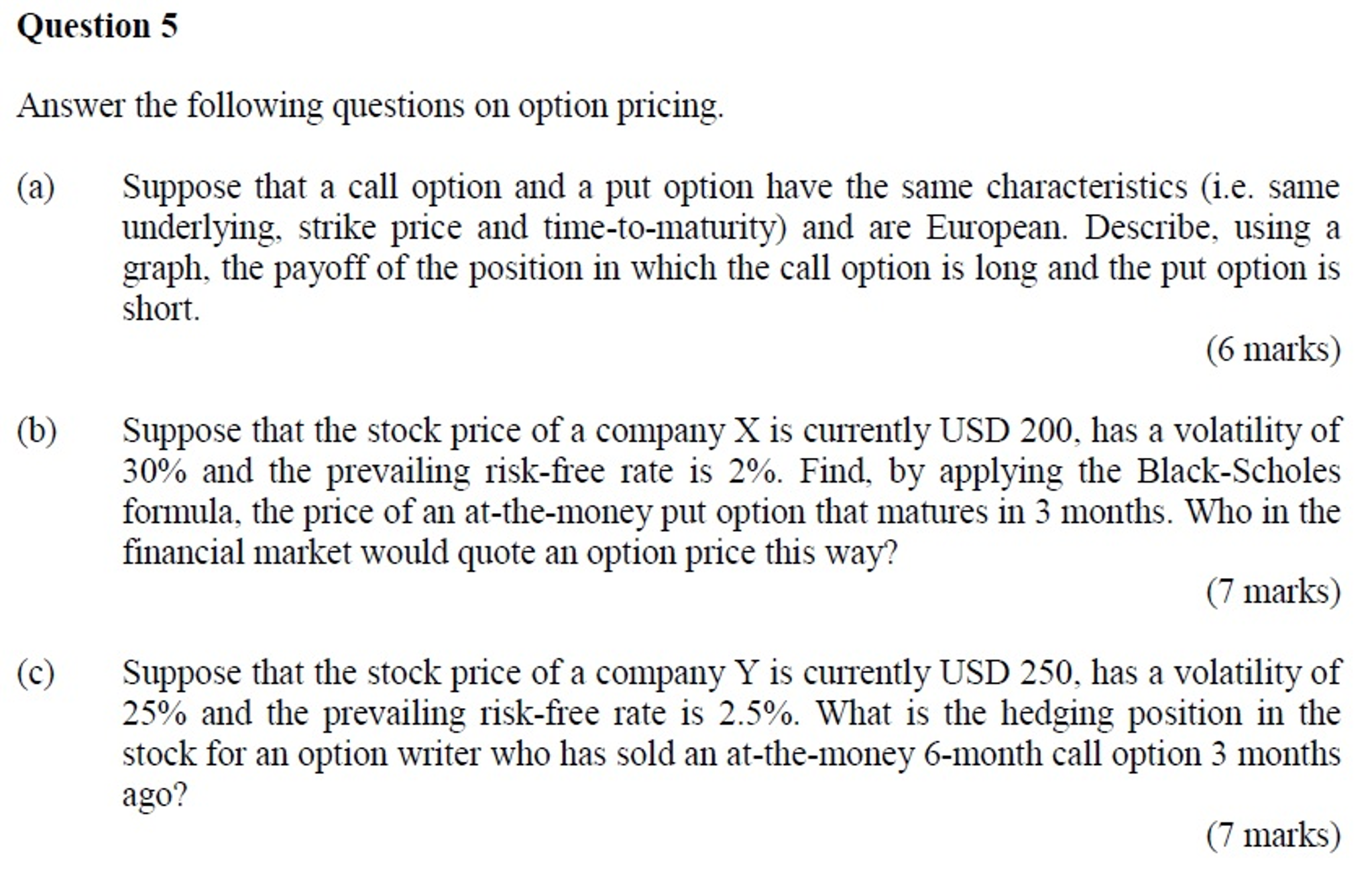

Answer the following questions on option pricing. Suppose that a call option and a put option have the same characteristics (i.e. same underlying, strike price and time-to-maturity) and are European. Describe, using a graph, the payoff of the position in which the call option is long and the put option is short. Suppose that the stock price of a company X is currently USD 200, has a volatility of 30% and the prevailing risk-free rate is 2%. Find, by applying the Black-Scholes formula, the price of an at-the-money put option that matures in 3 months. Who in the financial market would quote an option price this way? Suppose that the stock price of a company Y is currently USD 250, has a volatility of 25% and the prevailing risk-free rate is 2.5%. What is the hedging position in the stock for an option writer who has sold an at-the-money 6-month call option 3 months agoStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Interest Rate Swaps And Their Derivatives A Practitioners Guide

Authors: Amir Sadr

1st Edition

0470443944, 978-0470443941