Answered step by step

Verified Expert Solution

Question

1 Approved Answer

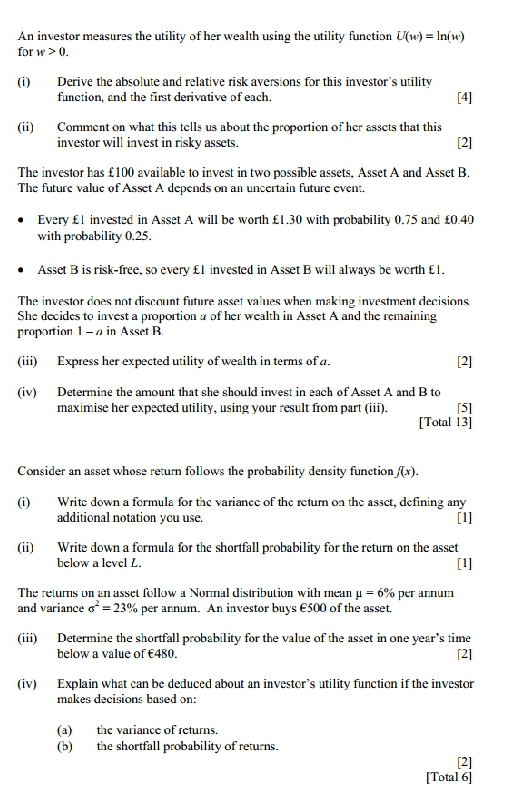

Please solve precisely. Thank you An investor measures the utility of her wealth using the utility function Uw) = In(w) for w > 0. (i)

Please solve precisely. Thank you

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Economic Change In Asia Implications For Corporate Strategy And Social Responsibility

Authors: M Bruna Zolin, Bernadette Andreosso O'Callaghan, Jacques Jaussaud

1st Edition

1317286650, 9781317286653