Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please use the following information to prepare the business combination valuation entries and the pre-acquisition entries as at: 1 July 2017 30 June 2018 30

Please use the following information to prepare the business combination valuation entries and the pre-acquisition entries as at:

1 July 2017

30 June 2018

30 June 2019

30 June 2020

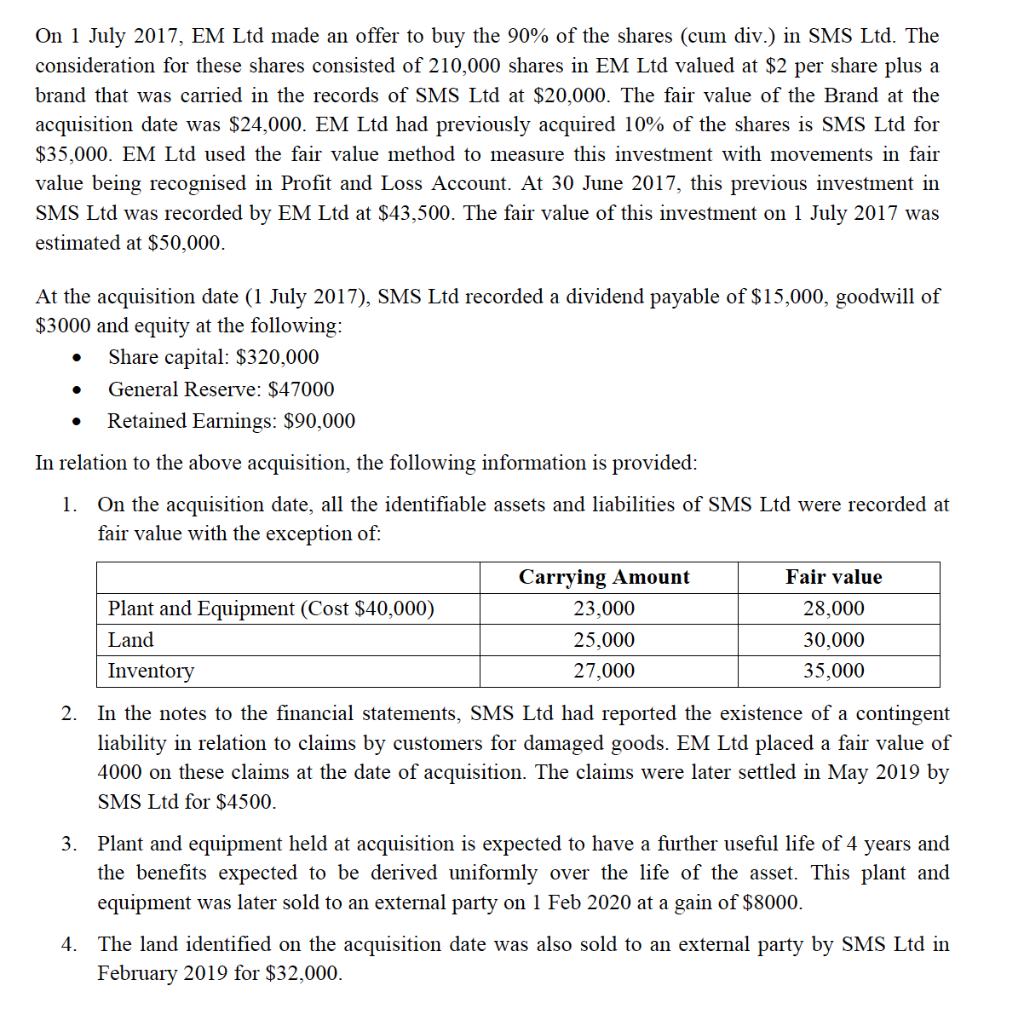

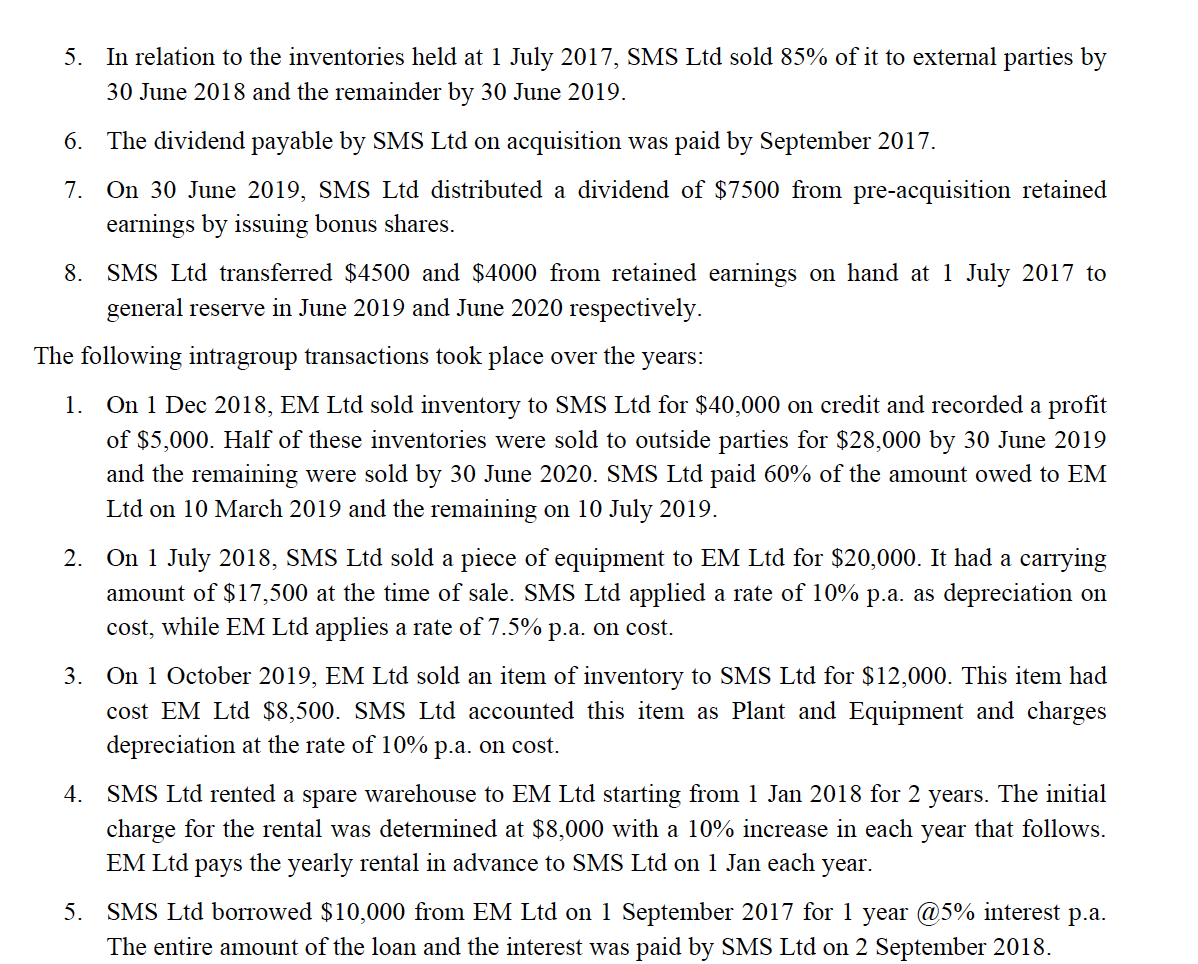

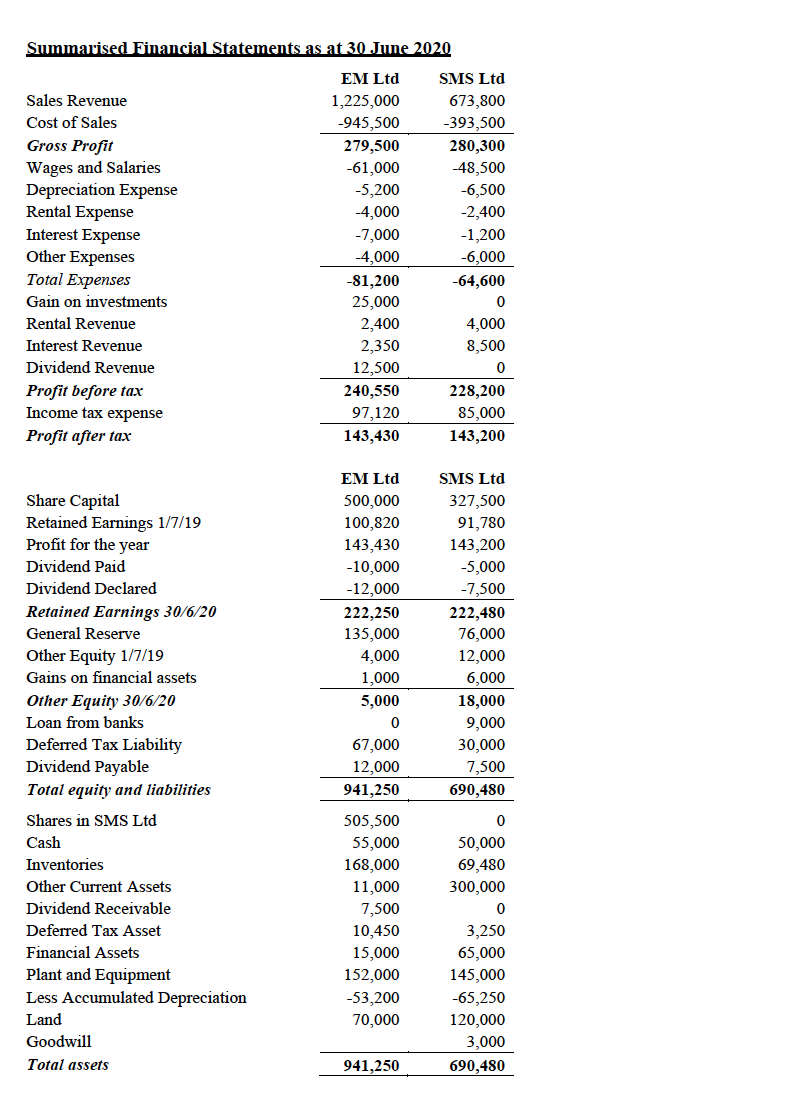

On 1 July 2017, EM Ltd made an offer to buy the 90% of the shares (cum div.) in SMS Ltd. The consideration for these shares consisted of 210,000 shares in EM Ltd valued at $2 per share plus a brand that was carried in the records of SMS Ltd at $20,000. The fair value of the Brand at the acquisition date was $24,000. EM Ltd had previously acquired 10% of the shares is SMS Ltd for $35,000. EM Ltd used the fair value method to measure this investment with movements in fair value being recognised in Profit and Loss Account. At 30 June 2017, this previous investment in SMS Ltd was recorded by EM Ltd at $43,500. The fair value of this investment on 1 July 2017 was estimated at $50,000. At the acquisition date (1 July 2017), SMS Ltd recorded a dividend payable of $15,000, goodwill of $3000 and equity at the following: Share capital: $320,000 General Reserve: $47000 Retained Earnings: $90,000 In relation to the above acquisition, the following information is provided: 1. On the acquisition date, all the identifiable assets and liabilities of SMS Ltd were recorded at fair value with the exception of: . Plant and Equipment (Cost $40,000) Land Carrying Amount 23,000 25,000 27,000 Fair value 28,000 30,000 35,000 Inventory 2. In the notes to the financial statements, SMS Ltd had reported the existence of a contingent liability in relation to claims by customers for damaged goods. EM Ltd placed a fair value of 4000 on these claims at the date of acquisition. The claims were later settled in May 2019 by SMS Ltd for $4500. 3. Plant and equipment held at acquisition is expected to have a further useful life of 4 years and the benefits expected to be derived uniformly over the life of the asset. This plant and equipment was later sold to an external party on 1 Feb 2020 at a gain of $8000. 4. The land identified on the acquisition date was also sold to an external party by SMS Ltd in February 2019 for $32,000. 5. In relation to the inventories held at 1 July 2017, SMS Ltd sold 85% of it to external parties by 30 June 2018 and the remainder by 30 June 2019. 6. The dividend payable by SMS Ltd on acquisition was paid by September 2017. 7. On 30 June 2019, SMS Ltd distributed a dividend of $7500 from pre-acquisition retained earnings by issuing bonus shares. 8. SMS Ltd transferred $4500 and $4000 from retained earnings on hand at 1 July 2017 to general reserve in June 2019 and June 2020 respectively. The following intragroup transactions took place over the years: 1. On 1 Dec 2018, EM Ltd sold inventory to SMS Ltd for $40,000 on credit and recorded a profit of $5,000. Half of these inventories were sold to outside parties for $28,000 by 30 June 2019 and the remaining were sold by 30 June 2020. SMS Ltd paid 60% of the amount owed to EM Ltd on 10 March 2019 and the remaining on 10 July 2019. 2. On 1 July 2018, SMS Ltd sold a piece of equipment to EM Ltd for $20,000. It had a carrying amount of $17,500 at the time of sale. SMS Ltd applied a rate of 10% p.a. as depreciation on cost, while EM Ltd applies a rate of 7.5% p.a. on cost. 3. On 1 October 2019, EM Ltd sold an item of inventory to SMS Ltd for $12,000. This item had cost EM Ltd $8,500. SMS Ltd accounted this item as Plant and Equipment and charges depreciation at the rate of 10% p.a. on cost. 4. SMS Ltd rented a spare warehouse to EM Ltd starting from 1 Jan 2018 for 2 years. The initial charge for the rental was determined at $8,000 with a 10% increase in each year that follows. EM Ltd pays the yearly rental in advance to SMS Ltd on 1 Jan each year. 5. SMS Ltd borrowed $10,000 from EM Ltd on 1 September 2017 for 1 year @5% interest p.a. The entire amount of the loan and the interest was paid by SMS Ltd on 2 September 2018. Summarised Financial Statements as at 30 June 2020 Sales Revenue Cost of Sales Gross Profit Wages and Salaries Depreciation Expense Rental Expense Interest Expense Other Expenses Total Expenses Gain on investments Rental Revenue Interest Revenue Dividend Revenue Profit before tax Income tax expense Profit after tax EM Ltd 1,225,000 -945,500 279,500 -61,000 -5,200 -4,000 -7,000 -4,000 -81,200 25,000 2,400 2,350 12,500 240,550 97,120 143,430 SMS Ltd 673,800 -393,500 280,300 -48,500 -6,500 -2,400 -1,200 -6,000 -64,600 0 4,000 8,500 0 228,200 85,000 143,200 EM Ltd 500,000 100,820 143,430 -10,000 -12,000 222,250 135,000 4,000 1,000 5,000 0 67,000 12,000 941,250 SMS Ltd 327,500 91,780 143,200 -5,000 -7,500 222,480 76,000 12,000 Share Capital Retained Earnings 1/7/19 Profit for the year Dividend Paid Dividend Declared Retained Earnings 30/6/20 General Reserve Other Equity 1/7/19 Gains on financial assets Other Equity 30/6/20 Loan from banks Deferred Tax Liability Dividend Payable Total equity and liabilities Shares in SMS Ltd Cash Inventories Other Current Assets Dividend Receivable Deferred Tax Asset Financial Assets Plant and Equipment Less Accumulated Depreciation Land Goodwill Total assets 6,000 18,000 9,000 30,000 7,500 690,480 505,500 55,000 168,000 11,000 7,500 10,450 15,000 152,000 -53,200 70,000 0 50,000 69,480 300,000 0 3,250 65,000 145,000 -65,250 120,000 3,000 690,480 941,250

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Why CISOs Fail Internal Audit And IT Audit The Missing Link In Security Management How To Fix It

Authors: Barak Engel

1st Edition

1138197890, 978-1138197893