Question

Pls solve the problem urgently but correctly and step by step will leave you 10 likes Description: This is a case we worked on during

Pls solve the problem urgently but correctly and step by step will leave you 10 likes

Description:

This is a case we worked on during the Annual AICPA Accounting and Tax Conference in Washington DC a few years ago. It is a fairly complicated case that took my team a while to figure out. I believe it is a great way to practice your debits and credits. It was a 100-minute session with top KPMG European partners acting as workshop leaders.

Required - Make all journal entries indicated for FY 2012 using pages 3 and 4. Observe that positive R/E and Reserve numbers are credits and negative numbers are debits to R/E and Reserves. Your analyses must show the accounts that are Credited and Debited against the DRs and CRs made in the R/E account and in the OCI Reserve accounts.

This is a critical analysis and thinking case that requires you to analyze incomplete information and synthesize a solution drawing upon mostly Intermediate Accounting knowledge and information gained from the IFRS text. The MSWord file email attachment should be one page (the last page completed).

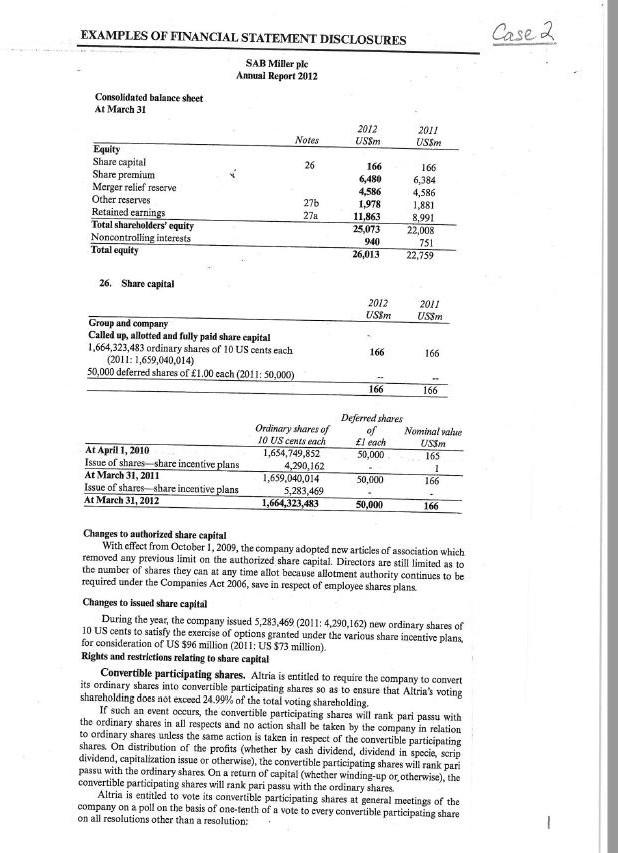

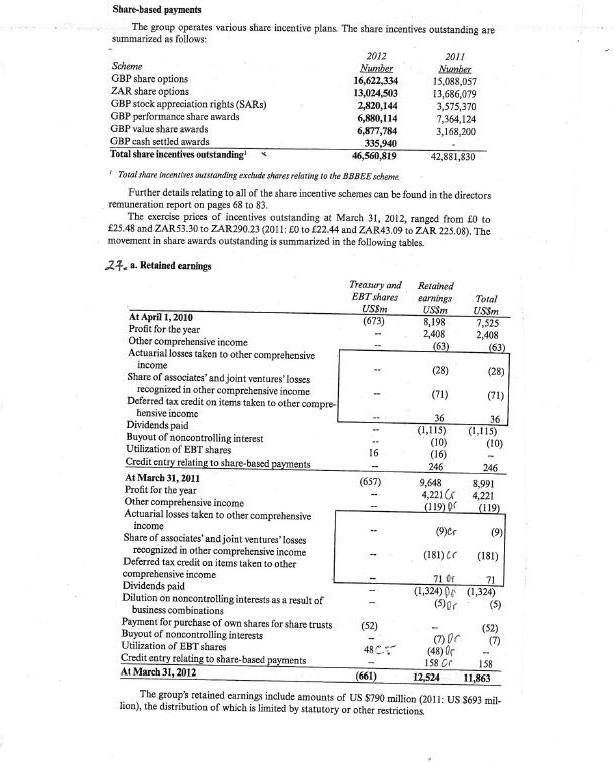

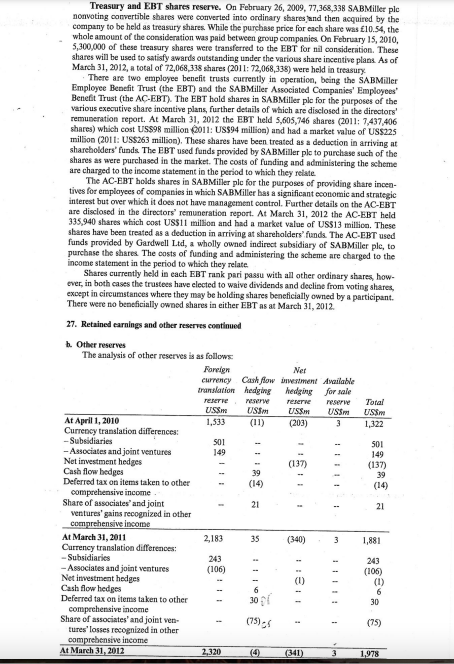

EXAMPLES OF FINANCIAL STATEMENT DISCLOSURES SAB Miller plc Annusal Report 2012 Consolidated balance sheet At March 31 26. Share capital Changes to authorized share capital With effect from October 1,2009, the company adopted new articles of association which removed any previous limit on the authorized share capital. Directors are still limited as to the number of sbares they can at any time allot because allotment authority continucs to be required under the Companies Act 2006, save in respect of employee shares plans. Changes to issued share capital During the yeas, the company issued \\( 5,283,469(2011: 4,290,162) \\) new ordinary shares of 10 US cents to satisfy the exercise of options granted under the various share incentive plans, for consideration of US \\( \\$ 96 \\) million (2011: US \\( \\$ 73 \\) million). Rights and restrictions relating to share capital Convertible participating shares. Altria is entitled to require the company to convert its ordinary shares into convertible participating shares so as to ensure that Altria's voting shareholding does ast excoed \24.99 of the total voting shareholding. If such an event occurs, the convertible participating shares will rank pari passu with the ordinary shares in all respects and no action shall be taken by the company in relation to ordinary shares urless the same action is taken in respect of the convertible participating shares On distribution of the profits (whether by cash dividend, dividend in specie, scrip dividend, capitalization issue or otherwise), the convertible participating shares will rank pari passu with the ordinary shares On a return of capital (whether winding-up or, otherwise), the convertible participating shares will rank pari passu with the ordinary shares. Altria is entitled to vote its convertible participating shares at general meetings of the company on a poll on the basis of one-tenth of a vote to every convertible participating share on all resolutions other than a resolution: Share-based payments The group operates various share incentive plans. The share incentives outstanding are summarized as follows: 1. Total share incentwes outsanding exclude shares relating to the BBBEE scheme Further details relating to all of the share inceative schemes can be found in the directors remuneration report on pages 68 to 83 . The exercise prices of incentives outstanding at March 31, 2012, ranged from fo to f25.48 and ZAR 53.30 to ZAR290.23 (2011; E0 to 22.44 and ZAR43.09 to ZAR 225.08). The movement in share awards outstanding is summarized in the following tables. 27. a. Retained earnings lion), the distribution of which is limited by statutory or other restrictions Treasury and EBT shares reserve. On February 26, 2009, 77,368,338 SABMillet ple nonvoting convertible shares were corverted into ordinary shares, and then acquired by the company to be held as treasury shares. While the purchase price for each share was 210.54 , the whole amouat of the consideration was paid between group companies. On February 15, 2010, \\( 5,300,000 \\) of these treasury shares were transferred to the EBT for nil consideration. These shares will be used to satisfy awards outstanding under the various share incentive plans. As of March 31, 2012, a total of 72,068,338 shares (2011: 72,068,338) were held in treasury. There are two employee benefit trusts curreotly in operntion, being the SABMiller Employee Benefit Trust (the EBT) asd the SABMiller Associated Companies' Employees' Beneft Trust (the AC-EBT). The EBT hold shares in SABMiller ple for the purposes of the various executive share incentive plans, further details of which are disclosed in the directors' remuneration report. At March 31, 2012 the EBT held 5,605,746 shares (2011: 7,437,406 shares) which cost US\\$98 million (0011: US\\$94 million) and had a market value of US\\$225 milson (201 1: US\\$263 million). These shares have been treated as a deduction in arriving at shareholders' funds. The EBT used funds provided by SABMiller ple to purchase such of the shares as were purchased in the market. The costs of funding and administering the scheme are charged to the income statement in the period to which they relate. The AC-EBT bolds shares in SABMiller ple for the purposes of providing share incentives for emplayees of companies in which SABMiller bas a significant economic and strategic interest but over which it does not have management control. Further details on the AC-EBT are disclosed in the directors' remuneration report. At March 31, 2012 the AC-EBT held 335,940 shares which cost USS11 million and had a market value of USS13 million. These shares have been treated as a deduction in arriving at shareholders' funds. The AC-EBT used funds provided by Gardwell Ltd, a wholly owned indirect subsidiary of SABMillef ple, to purchase the shares. The costs of funding and administering the scheme are charged to the income statement in the period to which they relate. Shares currently beld in each EBT rank pari passu with all other ordinary shares, howover, in both cases the trustees have elected to waive dividends and decline from woting shares, exoept in circumstances where they may be holding shares beneficially owned by a participant. There were no beneficially owned shares in either EBT as at March 31, 2012. 27. Retained earnings and other reserves coetinued b. Other reserves The analysis of other reserves is as follows: (i) Proposed by any person other than Altria, to wind-up the company; (ii) Proposed by any person other than Altria, to appoint an administrator or to approve any arrangement with the company's creditors; (iii) Proposed by the board, to sell all or substantially all of the undertaking of the company; or (iv) Proposed by any person other than Altria, to alter any of the class rights attaching to the convertible participating shares or to approve the creation of any new class of shares, in which case Altria shall be entitled on a poll to vote on the resolution on the basis of one vote for each convertible participating share, but for the purposes of any resolution other than a resolution meationed in (iv) above, the convertible participating shares shall be treated as being of the same class as the ordinary shares and no separate meeting or resolution of the bolders of the convertible participating share shall be required to be convened or passed. Upon a transfer of convertible participating shares by Altria other than to an affiliate, such convertible participating shares shall convert into ordinary shares. Altria is entitled to require the company to convert its convertible participating shares into ordinary shares if: (i) A third party has made a takeover offer for the company and (if such offer becomes or is declared unconditional in all respects) it would result in the yoting shareholding of the third party being more than \30 of the total votingshareholding; and (ii) Altria has communicated to the company in writing its intention not itself to make an offer competing with such third party offer, provided that the conversion date shall be no earlier than the date on which the third party's offer becomes or is declared unconditional in all respects. Altria is entitled to require the company to convert its convertible participating shares into ordinary shares if the voting shareholding of a third party should be more than \24.99, provided that: (i) The number of ordinary shares held by Altria following such conversion shain be limited to one ordinary share more than the number of ordinary shares held by the third party; and (ii) Such conversion shall at no time result in Altria's voting shareholding being equal to or greater than the woting shareholding which would require Altria to make a mandatory offer in terms of Rule 9 of the City Code. If Altria wishes to acquire additional ordinary shares (other than pursuant to a preamptive issue of new ordinary shares or with the prior approval of the board), Altria shall first convert into ordinary shares the lesser of: (i) Such number of convertible participating shares as would result in Altria's voting shareholding being such percentage as would, in the event of Altria sabsequently acquiring one additional ordinary share, require Altria to make a mandatory offer in terms of Rule 9 of the City Code; and (ii) All of its remaining convertible participating shares. The company must use its best endeavors to procure that the ordinary shares arising on conversion of the convertible participating shares are admitted to the Official List and to trading on the London Stock Exchange's market for listed securities, admitted to listing and trading on the JSE Ltd, and admitted to listing and trading on any other stock exchange upon which the ordinary shares are from time to time listed and traded, but no admission to listing or trading shall be sought for the convertible participating shares while they remain convertible participating shares. Deferred shares The deferred shares do not carry any voting rights and do not entitle holders thereof to receive any dividends or other distributions. In the event of a winding-up, deferred shareholders would receive no more than the nominal valve. Deferred shares represent the only nonequity share capital of the group. EXAMPLES OF FINANCIAL STATEMENT DISCLOSURES SAB Miller plc Annusal Report 2012 Consolidated balance sheet At March 31 26. Share capital Changes to authorized share capital With effect from October 1,2009, the company adopted new articles of association which removed any previous limit on the authorized share capital. Directors are still limited as to the number of sbares they can at any time allot because allotment authority continucs to be required under the Companies Act 2006, save in respect of employee shares plans. Changes to issued share capital During the yeas, the company issued \\( 5,283,469(2011: 4,290,162) \\) new ordinary shares of 10 US cents to satisfy the exercise of options granted under the various share incentive plans, for consideration of US \\( \\$ 96 \\) million (2011: US \\( \\$ 73 \\) million). Rights and restrictions relating to share capital Convertible participating shares. Altria is entitled to require the company to convert its ordinary shares into convertible participating shares so as to ensure that Altria's voting shareholding does ast excoed \24.99 of the total voting shareholding. If such an event occurs, the convertible participating shares will rank pari passu with the ordinary shares in all respects and no action shall be taken by the company in relation to ordinary shares urless the same action is taken in respect of the convertible participating shares On distribution of the profits (whether by cash dividend, dividend in specie, scrip dividend, capitalization issue or otherwise), the convertible participating shares will rank pari passu with the ordinary shares On a return of capital (whether winding-up or, otherwise), the convertible participating shares will rank pari passu with the ordinary shares. Altria is entitled to vote its convertible participating shares at general meetings of the company on a poll on the basis of one-tenth of a vote to every convertible participating share on all resolutions other than a resolution: Share-based payments The group operates various share incentive plans. The share incentives outstanding are summarized as follows: 1. Total share incentwes outsanding exclude shares relating to the BBBEE scheme Further details relating to all of the share inceative schemes can be found in the directors remuneration report on pages 68 to 83 . The exercise prices of incentives outstanding at March 31, 2012, ranged from fo to f25.48 and ZAR 53.30 to ZAR290.23 (2011; E0 to 22.44 and ZAR43.09 to ZAR 225.08). The movement in share awards outstanding is summarized in the following tables. 27. a. Retained earnings lion), the distribution of which is limited by statutory or other restrictions Treasury and EBT shares reserve. On February 26, 2009, 77,368,338 SABMillet ple nonvoting convertible shares were corverted into ordinary shares, and then acquired by the company to be held as treasury shares. While the purchase price for each share was 210.54 , the whole amouat of the consideration was paid between group companies. On February 15, 2010, \\( 5,300,000 \\) of these treasury shares were transferred to the EBT for nil consideration. These shares will be used to satisfy awards outstanding under the various share incentive plans. As of March 31, 2012, a total of 72,068,338 shares (2011: 72,068,338) were held in treasury. There are two employee benefit trusts curreotly in operntion, being the SABMiller Employee Benefit Trust (the EBT) asd the SABMiller Associated Companies' Employees' Beneft Trust (the AC-EBT). The EBT hold shares in SABMiller ple for the purposes of the various executive share incentive plans, further details of which are disclosed in the directors' remuneration report. At March 31, 2012 the EBT held 5,605,746 shares (2011: 7,437,406 shares) which cost US\\$98 million (0011: US\\$94 million) and had a market value of US\\$225 milson (201 1: US\\$263 million). These shares have been treated as a deduction in arriving at shareholders' funds. The EBT used funds provided by SABMiller ple to purchase such of the shares as were purchased in the market. The costs of funding and administering the scheme are charged to the income statement in the period to which they relate. The AC-EBT bolds shares in SABMiller ple for the purposes of providing share incentives for emplayees of companies in which SABMiller bas a significant economic and strategic interest but over which it does not have management control. Further details on the AC-EBT are disclosed in the directors' remuneration report. At March 31, 2012 the AC-EBT held 335,940 shares which cost USS11 million and had a market value of USS13 million. These shares have been treated as a deduction in arriving at shareholders' funds. The AC-EBT used funds provided by Gardwell Ltd, a wholly owned indirect subsidiary of SABMillef ple, to purchase the shares. The costs of funding and administering the scheme are charged to the income statement in the period to which they relate. Shares currently beld in each EBT rank pari passu with all other ordinary shares, howover, in both cases the trustees have elected to waive dividends and decline from woting shares, exoept in circumstances where they may be holding shares beneficially owned by a participant. There were no beneficially owned shares in either EBT as at March 31, 2012. 27. Retained earnings and other reserves coetinued b. Other reserves The analysis of other reserves is as follows: (i) Proposed by any person other than Altria, to wind-up the company; (ii) Proposed by any person other than Altria, to appoint an administrator or to approve any arrangement with the company's creditors; (iii) Proposed by the board, to sell all or substantially all of the undertaking of the company; or (iv) Proposed by any person other than Altria, to alter any of the class rights attaching to the convertible participating shares or to approve the creation of any new class of shares, in which case Altria shall be entitled on a poll to vote on the resolution on the basis of one vote for each convertible participating share, but for the purposes of any resolution other than a resolution meationed in (iv) above, the convertible participating shares shall be treated as being of the same class as the ordinary shares and no separate meeting or resolution of the bolders of the convertible participating share shall be required to be convened or passed. Upon a transfer of convertible participating shares by Altria other than to an affiliate, such convertible participating shares shall convert into ordinary shares. Altria is entitled to require the company to convert its convertible participating shares into ordinary shares if: (i) A third party has made a takeover offer for the company and (if such offer becomes or is declared unconditional in all respects) it would result in the yoting shareholding of the third party being more than \30 of the total votingshareholding; and (ii) Altria has communicated to the company in writing its intention not itself to make an offer competing with such third party offer, provided that the conversion date shall be no earlier than the date on which the third party's offer becomes or is declared unconditional in all respects. Altria is entitled to require the company to convert its convertible participating shares into ordinary shares if the voting shareholding of a third party should be more than \24.99, provided that: (i) The number of ordinary shares held by Altria following such conversion shain be limited to one ordinary share more than the number of ordinary shares held by the third party; and (ii) Such conversion shall at no time result in Altria's voting shareholding being equal to or greater than the woting shareholding which would require Altria to make a mandatory offer in terms of Rule 9 of the City Code. If Altria wishes to acquire additional ordinary shares (other than pursuant to a preamptive issue of new ordinary shares or with the prior approval of the board), Altria shall first convert into ordinary shares the lesser of: (i) Such number of convertible participating shares as would result in Altria's voting shareholding being such percentage as would, in the event of Altria sabsequently acquiring one additional ordinary share, require Altria to make a mandatory offer in terms of Rule 9 of the City Code; and (ii) All of its remaining convertible participating shares. The company must use its best endeavors to procure that the ordinary shares arising on conversion of the convertible participating shares are admitted to the Official List and to trading on the London Stock Exchange's market for listed securities, admitted to listing and trading on the JSE Ltd, and admitted to listing and trading on any other stock exchange upon which the ordinary shares are from time to time listed and traded, but no admission to listing or trading shall be sought for the convertible participating shares while they remain convertible participating shares. Deferred shares The deferred shares do not carry any voting rights and do not entitle holders thereof to receive any dividends or other distributions. In the event of a winding-up, deferred shareholders would receive no more than the nominal valve. Deferred shares represent the only nonequity share capital of the group

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Survey of Accounting

Authors: Carl S Warren

5th Edition

9780538489737, 538749091, 538489731, 978-0538749091