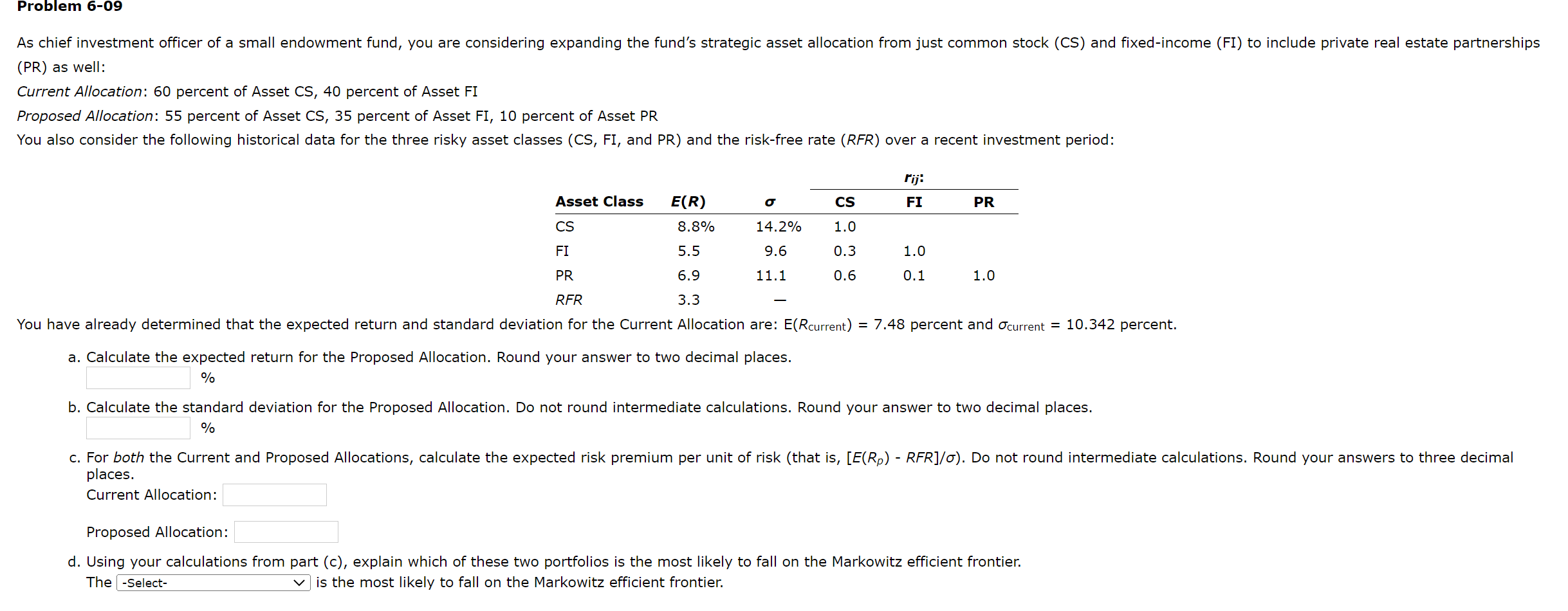

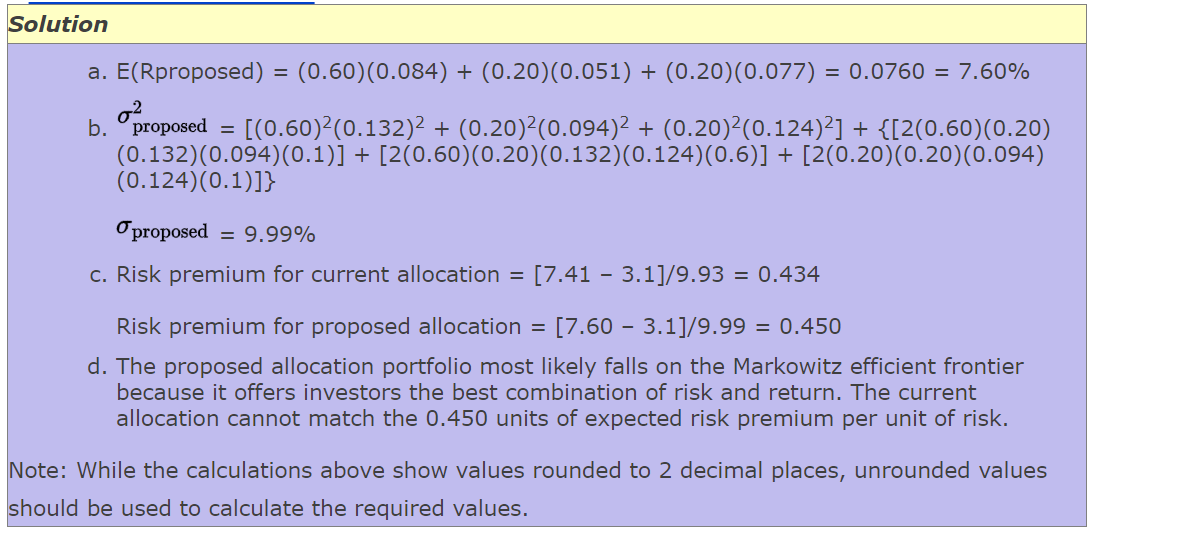

(PR) as well: Current Allocation: 60 percent of Asset CS, 40 percent of Asset FI Proposed Allocation: 55 percent of Asset CS, 35 percent of Asset FI, 10 percent of Asset PR You also consider the following historical data for the three risky asset classes (CS, FI, and PR) and the risk-free rate (RFR) over a recent investment period: You have already determined that the expected return and standard deviation for the Current Allocation are: E(Rcurrent)=7.48 percent and current=10.342 percent. a. Calculate the expected return for the Proposed Allocation. Round your answer to two decimal places. % b. Calculate the standard deviation for the Proposed Allocation. Do not round intermediate calculations. Round your answer to two decimal places. % places. Current Allocation: Proposed Allocation: d. Using your calculations from part (c), explain which of these two portfolios is the most likely to fall on the Markowitz efficient frontier. The -Select- is the most likely to fall on the Markowitz efficient frontier. a. E( Rproposed )=(0.60)(0.084)+(0.20)(0.051)+(0.20)(0.077)=0.0760=7.60% b. proposed2=[(0.60)2(0.132)2+(0.20)2(0.094)2+(0.20)2(0.124)2]+{[2(0.60)(0.20) (0.132)(0.094)(0.1)]+[2(0.60)(0.20)(0.132)(0.124)(0.6)]+[2(0.20)(0.20)(0.094) (0.124)(0.1)]} proposed=9.99% c. Risk premium for current allocation =[7.413.1]/9.93=0.434 Risk premium for proposed allocation =[7.603.1]/9.99=0.450 d. The proposed allocation portfolio most likely falls on the Markowitz efficient frontier because it offers investors the best combination of risk and return. The current allocation cannot match the 0.450 units of expected risk premium per unit of risk. While the calculations above show values rounded to 2 decimal places, unrounded values ould be used to calculate the required values. (PR) as well: Current Allocation: 60 percent of Asset CS, 40 percent of Asset FI Proposed Allocation: 55 percent of Asset CS, 35 percent of Asset FI, 10 percent of Asset PR You also consider the following historical data for the three risky asset classes (CS, FI, and PR) and the risk-free rate (RFR) over a recent investment period: You have already determined that the expected return and standard deviation for the Current Allocation are: E(Rcurrent)=7.48 percent and current=10.342 percent. a. Calculate the expected return for the Proposed Allocation. Round your answer to two decimal places. % b. Calculate the standard deviation for the Proposed Allocation. Do not round intermediate calculations. Round your answer to two decimal places. % places. Current Allocation: Proposed Allocation: d. Using your calculations from part (c), explain which of these two portfolios is the most likely to fall on the Markowitz efficient frontier. The -Select- is the most likely to fall on the Markowitz efficient frontier. a. E( Rproposed )=(0.60)(0.084)+(0.20)(0.051)+(0.20)(0.077)=0.0760=7.60% b. proposed2=[(0.60)2(0.132)2+(0.20)2(0.094)2+(0.20)2(0.124)2]+{[2(0.60)(0.20) (0.132)(0.094)(0.1)]+[2(0.60)(0.20)(0.132)(0.124)(0.6)]+[2(0.20)(0.20)(0.094) (0.124)(0.1)]} proposed=9.99% c. Risk premium for current allocation =[7.413.1]/9.93=0.434 Risk premium for proposed allocation =[7.603.1]/9.99=0.450 d. The proposed allocation portfolio most likely falls on the Markowitz efficient frontier because it offers investors the best combination of risk and return. The current allocation cannot match the 0.450 units of expected risk premium per unit of risk. While the calculations above show values rounded to 2 decimal places, unrounded values ould be used to calculate the required values