Answered step by step

Verified Expert Solution

Question

1 Approved Answer

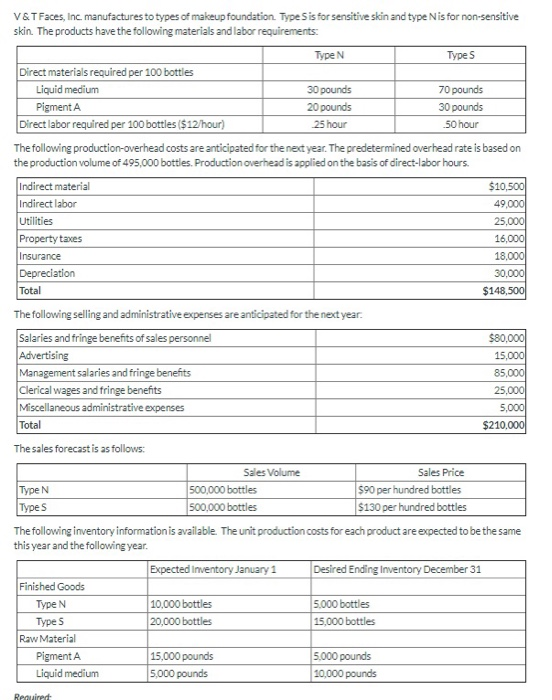

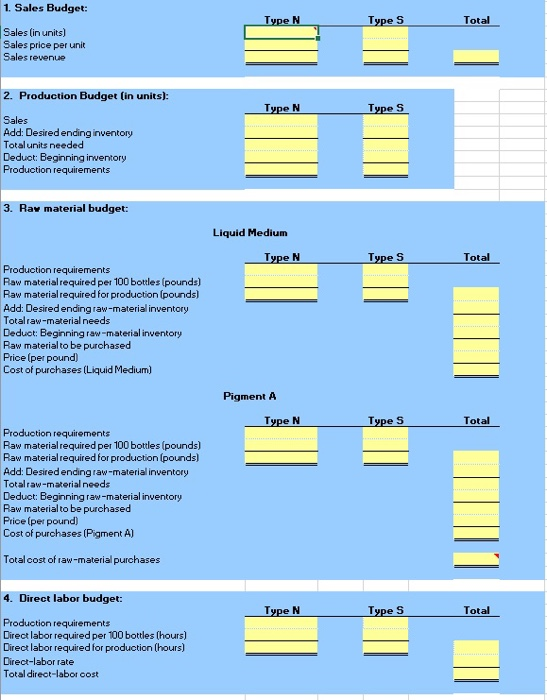

Prepare a master budget for V & T Faces, Inc., for the next year. Assume an income tax rate of 40 percent. Include the following:

Prepare a master budget for V & T Faces, Inc., for the next year. Assume an income tax rate of 40 percent. Include the following:

Sales budget

Production budget

Direct-material budget

Direct-labor budget

please use attached budget template

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Committees Audit Committees Issues Constraints And Development Trends Of Their Roles And Responsibilities

Authors: Mounir Hedhili

1st Edition

620362120X, 978-6203621204