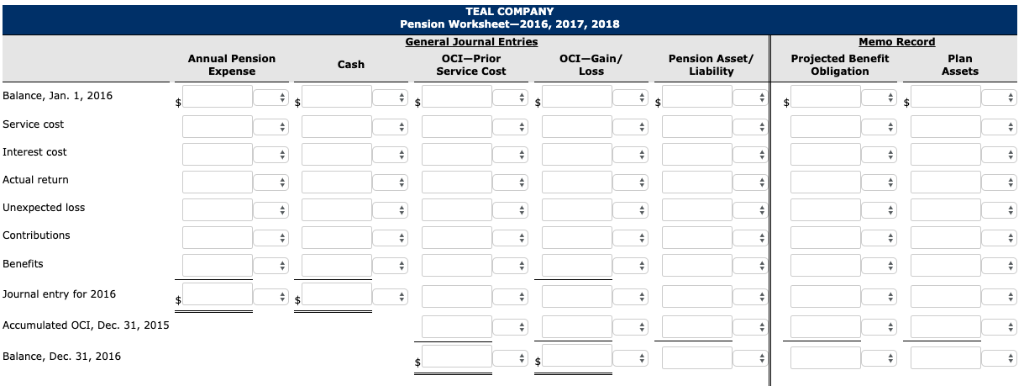

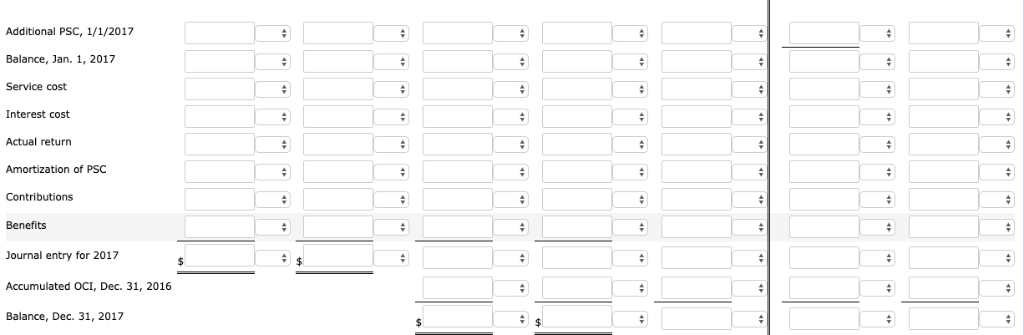

Prepare a pension worksheet presenting all 3 years pension balances and activities

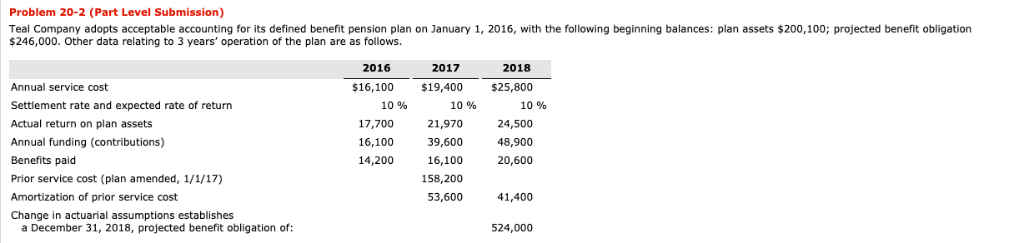

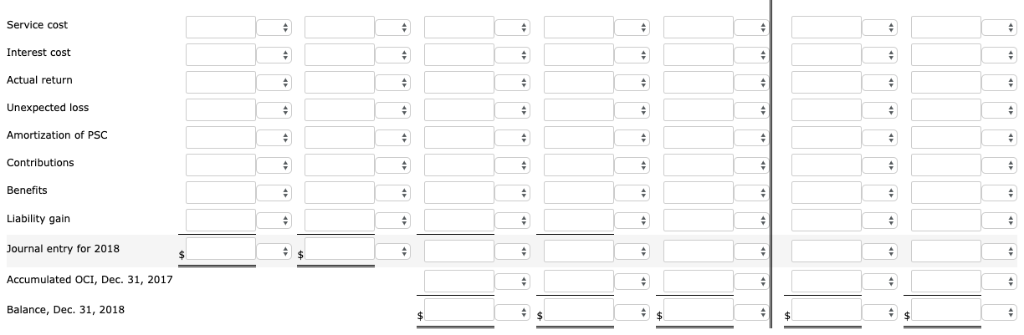

Problem 20-2 (Part Level Submission) Teal Company adopts acceptable accounting for its defined benefit pension plan on January 1, 2016, with the following beginning balances: plan assets $200,100; projected benefit obligation $246,000. Other data relating to 3 years' operation of the plan are as follows. 2016 2017 2018 Annual service cost Settlement rate and expected rate of return Actual return on plan assets Annual funding (contributions) Benefits paid Prior service cost (plan amended, 1/1/17) Amortization of prior service cost Change in actuarial assumptions establishes $16,100 $19,400 $25,800 10 % 10% 10% 17,700 16,100 14,200 21,970 39,600 16,100 158,200 53,600 24,500 48,900 20,600 41,400 a December 31, 2018, projected benefit obligation of: 524,000 TEAL COMPANY Pension Worksheet-2016, 2017, 2018 Annual Pension Expense ocI-Prior Service Cost OCI-Gain/ Loss Pension Asset/ Liability Projected Benefit Obligation Plan Assets Cash Balance, Jan. 1, 2016 Service cost Interest cost Actual return Contributions Benefits Journal entry for 2016 Accumulated OCI, Dec. 31, 2015 Balance, Dec. 31, 2016 Additional PSC, 1/1/2017 Balance, Jan. 1, 2017 Service cost Interest cost Actual return Amortization of PSC Contributions Benefits Journal entry for 2017 Accumulated OCI, Dec. 31, 2016 Balance, Dec. 31, 2017 Service cost Interest cost Actual return Unexpected loss Amortization of PSC Contributions Benefits Liability gain Journal entry for 2018 Accumulated OCI, Dec. 31, 2017 Balance, Dec. 31, 2018 Problem 20-2 (Part Level Submission) Teal Company adopts acceptable accounting for its defined benefit pension plan on January 1, 2016, with the following beginning balances: plan assets $200,100; projected benefit obligation $246,000. Other data relating to 3 years' operation of the plan are as follows. 2016 2017 2018 Annual service cost Settlement rate and expected rate of return Actual return on plan assets Annual funding (contributions) Benefits paid Prior service cost (plan amended, 1/1/17) Amortization of prior service cost Change in actuarial assumptions establishes $16,100 $19,400 $25,800 10 % 10% 10% 17,700 16,100 14,200 21,970 39,600 16,100 158,200 53,600 24,500 48,900 20,600 41,400 a December 31, 2018, projected benefit obligation of: 524,000 TEAL COMPANY Pension Worksheet-2016, 2017, 2018 Annual Pension Expense ocI-Prior Service Cost OCI-Gain/ Loss Pension Asset/ Liability Projected Benefit Obligation Plan Assets Cash Balance, Jan. 1, 2016 Service cost Interest cost Actual return Contributions Benefits Journal entry for 2016 Accumulated OCI, Dec. 31, 2015 Balance, Dec. 31, 2016 Additional PSC, 1/1/2017 Balance, Jan. 1, 2017 Service cost Interest cost Actual return Amortization of PSC Contributions Benefits Journal entry for 2017 Accumulated OCI, Dec. 31, 2016 Balance, Dec. 31, 2017 Service cost Interest cost Actual return Unexpected loss Amortization of PSC Contributions Benefits Liability gain Journal entry for 2018 Accumulated OCI, Dec. 31, 2017 Balance, Dec. 31, 2018