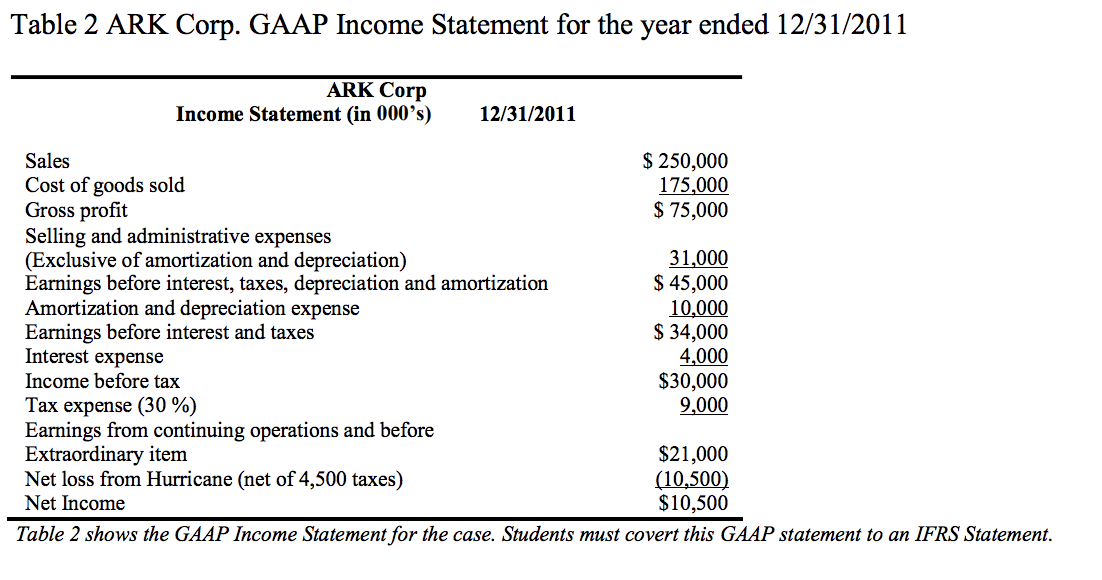

Prepare an income statement under IFRS for year 1. Assume that the net income remains the same under IFRS as it does for GAAP and any difference is reconciled in the tax expense and tax payable accounts.

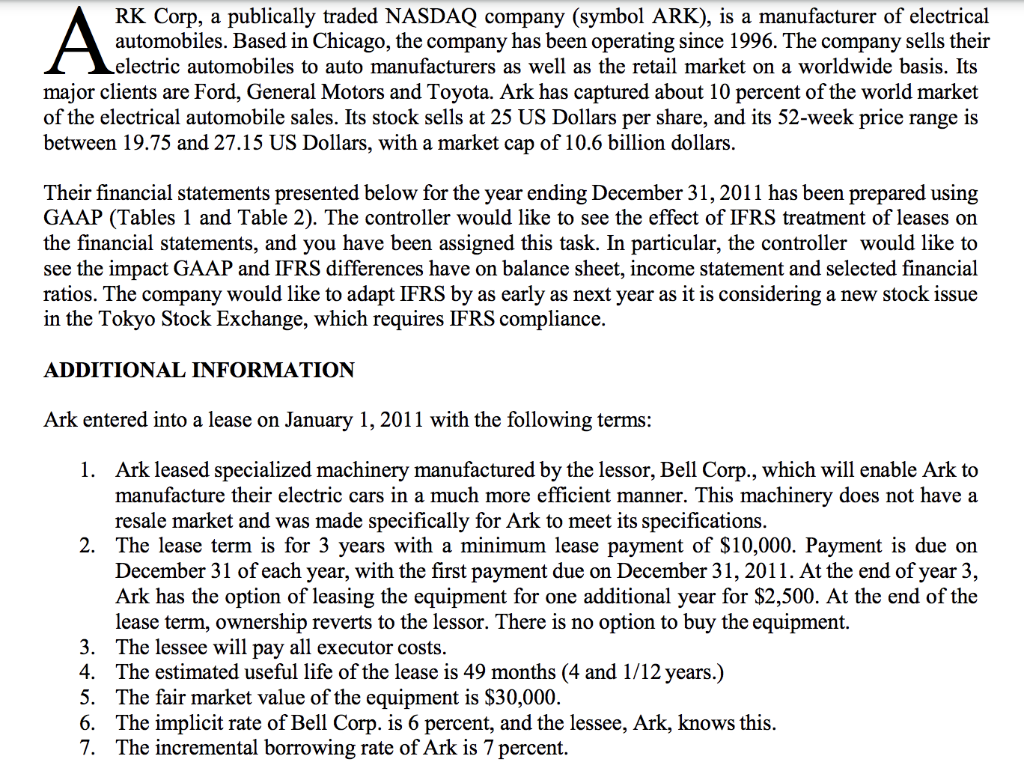

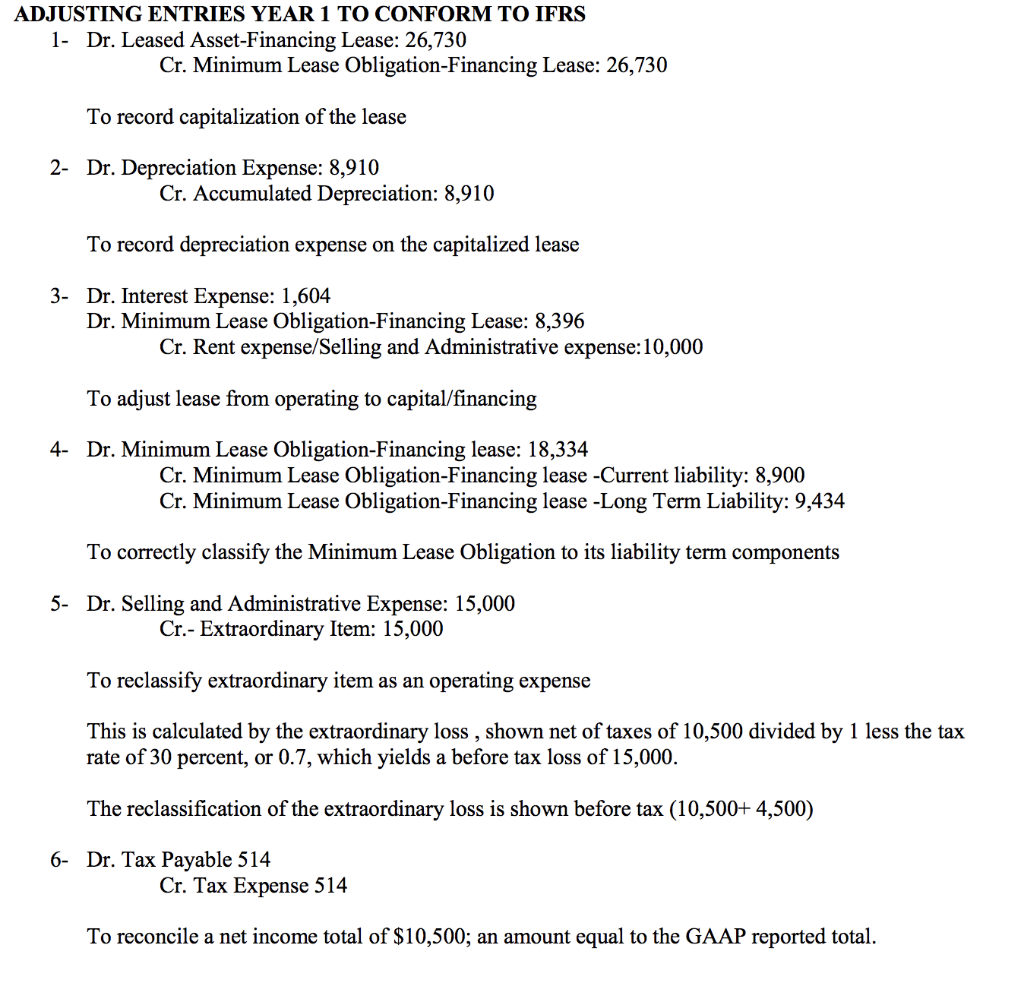

RK Corp, a publically traded NASDAQ company (symbol ARK), is a manufacturer of electrical automobiles. Based in Chicago, the company has been operating since 1996. The company sells their major clients are Ford, General Motors and Toyota. Ark has captured about 10 percent of the world market of the electrical automobile sales. Its stock sells at 25 US Dollars per share, and its 52-week price range is between 19.75 and 27.15 US Dollars, with a market cap of 10.6 billion dollars. Their financial statements presented below for the year ending December 31, 2011 has been prepared using GAAP (Tables 1 and Table 2). The controller would like to see the effect of IFRS treatment of leases on the financial statements, and you have been assigned this task. In particular, the controller would like to see the impact GAAP and IFRS differences have on balance sheet, income statement and selected financial ratios. The company would like to adapt IFRS by as early as next year as it is considering a new stock issue in the Tokyo Stock Exchange, which requires IFRS compliance. ADDITIONAL INFORMATION Ark entered into a lease on January 1, 2011 with the following terms: 1. Ark leased specialized machinery manufactured by the lessor, Bell Corp., which will enable Ark to manufacture their electric cars in a much more efficient manner. This machinery does not have a resale market and was made specifically for Ark to meet its specifications. 2. The lease term is for 3 years with a minimum lease payment of $10,000. Payment is due on December 31 of each year, with the first payment due on December 31, 2011. At the end of year 3, Ark has the option of leasing the equipment for one additional year for $2,500. At the end of the lease term, ownership reverts to the lessor. There is no option to buy the equipment. 3. The lessee will pay all executor costs. 4. The estimated useful life of the lease is 49 months (4 and 1/12 years.) 5. The fair market value of the equipment is $30,000. 6. The implicit rate of Bell Corp. is 6 percent, and the lessee, Ark, knows this. 7. The incremental borrowing rate of Ark is 7 percent. ADJUSTING ENTRIES YEAR 1 TO CONFORM TO IFRS 1- Dr. Leased Asset-Financing Lease: 26,730 Cr. Minimum Lease Obligation-Financing Lease: 26,730 To record capitalization of the lease 2- Dr. Depreciation Expense: 8,910 Cr. Accumulated Depreciation: 8,910 To record depreciation expense on the capitalized lease 3- Dr. Interest Expense: 1,604 Dr. Minimum Lease Obligation-Financing Lease: 8,396 Cr. Rent expense/Selling and Administrative expense:10,000 To adjust lease from operating to capital/financing 4- Dr. Minimum Lease Obligation-Financing lease: 18,334 Cr. Minimum Lease Obligation-Financing lease -Current liability: 8,900 Cr. Minimum Lease Obligation-Financing lease - Long Term Liability: 9,434 To correctly classify the Minimum Lease Obligation to its liability term components 5. Dr. Selling and Administrative Expense: 15,000 Cr.- Extraordinary Item: 15,000 To reclassify extraordinary item as an operating expense This is calculated by the extraordinary loss , shown net of taxes of 10,500 divided by 1 less the tax rate of 30 percent, or 0.7, which yields a before tax loss of 15,000. The reclassification of the extraordinary loss is shown before tax (10,500+ 4,500) 6- Dr. Tax Payable 514 Cr. Tax Expense 514 To reconcile a net income total of $10,500; an amount equal to the GAAP reported total. Table 2 ARK Corp. GAAP Income Statement for the year ended 12/31/2011 ARK Corp Income Statement (in 000's) 12/31/2011 Sales $ 250,000 Cost of goods sold 175,000 Gross profit $ 75,000 Selling and administrative expenses (Exclusive of amortization and depreciation) 31,000 Earnings before interest, taxes, depreciation and amortization $ 45,000 Amortization and depreciation expense 10,000 Earnings before interest and taxes $ 34,000 Interest expense 4,000 Income before tax $30,000 Tax expense (30 %) 9,000 Earnings from continuing operations and before Extraordinary item $21,000 Net loss from Hurricane (net of 4,500 taxes) (10,500) Net Income $10,500 Table 2 shows the GAAP Income Statement for the case. Students must covert this GAAP statement to an IFRS Statement. RK Corp, a publically traded NASDAQ company (symbol ARK), is a manufacturer of electrical automobiles. Based in Chicago, the company has been operating since 1996. The company sells their major clients are Ford, General Motors and Toyota. Ark has captured about 10 percent of the world market of the electrical automobile sales. Its stock sells at 25 US Dollars per share, and its 52-week price range is between 19.75 and 27.15 US Dollars, with a market cap of 10.6 billion dollars. Their financial statements presented below for the year ending December 31, 2011 has been prepared using GAAP (Tables 1 and Table 2). The controller would like to see the effect of IFRS treatment of leases on the financial statements, and you have been assigned this task. In particular, the controller would like to see the impact GAAP and IFRS differences have on balance sheet, income statement and selected financial ratios. The company would like to adapt IFRS by as early as next year as it is considering a new stock issue in the Tokyo Stock Exchange, which requires IFRS compliance. ADDITIONAL INFORMATION Ark entered into a lease on January 1, 2011 with the following terms: 1. Ark leased specialized machinery manufactured by the lessor, Bell Corp., which will enable Ark to manufacture their electric cars in a much more efficient manner. This machinery does not have a resale market and was made specifically for Ark to meet its specifications. 2. The lease term is for 3 years with a minimum lease payment of $10,000. Payment is due on December 31 of each year, with the first payment due on December 31, 2011. At the end of year 3, Ark has the option of leasing the equipment for one additional year for $2,500. At the end of the lease term, ownership reverts to the lessor. There is no option to buy the equipment. 3. The lessee will pay all executor costs. 4. The estimated useful life of the lease is 49 months (4 and 1/12 years.) 5. The fair market value of the equipment is $30,000. 6. The implicit rate of Bell Corp. is 6 percent, and the lessee, Ark, knows this. 7. The incremental borrowing rate of Ark is 7 percent. ADJUSTING ENTRIES YEAR 1 TO CONFORM TO IFRS 1- Dr. Leased Asset-Financing Lease: 26,730 Cr. Minimum Lease Obligation-Financing Lease: 26,730 To record capitalization of the lease 2- Dr. Depreciation Expense: 8,910 Cr. Accumulated Depreciation: 8,910 To record depreciation expense on the capitalized lease 3- Dr. Interest Expense: 1,604 Dr. Minimum Lease Obligation-Financing Lease: 8,396 Cr. Rent expense/Selling and Administrative expense:10,000 To adjust lease from operating to capital/financing 4- Dr. Minimum Lease Obligation-Financing lease: 18,334 Cr. Minimum Lease Obligation-Financing lease -Current liability: 8,900 Cr. Minimum Lease Obligation-Financing lease - Long Term Liability: 9,434 To correctly classify the Minimum Lease Obligation to its liability term components 5. Dr. Selling and Administrative Expense: 15,000 Cr.- Extraordinary Item: 15,000 To reclassify extraordinary item as an operating expense This is calculated by the extraordinary loss , shown net of taxes of 10,500 divided by 1 less the tax rate of 30 percent, or 0.7, which yields a before tax loss of 15,000. The reclassification of the extraordinary loss is shown before tax (10,500+ 4,500) 6- Dr. Tax Payable 514 Cr. Tax Expense 514 To reconcile a net income total of $10,500; an amount equal to the GAAP reported total. Table 2 ARK Corp. GAAP Income Statement for the year ended 12/31/2011 ARK Corp Income Statement (in 000's) 12/31/2011 Sales $ 250,000 Cost of goods sold 175,000 Gross profit $ 75,000 Selling and administrative expenses (Exclusive of amortization and depreciation) 31,000 Earnings before interest, taxes, depreciation and amortization $ 45,000 Amortization and depreciation expense 10,000 Earnings before interest and taxes $ 34,000 Interest expense 4,000 Income before tax $30,000 Tax expense (30 %) 9,000 Earnings from continuing operations and before Extraordinary item $21,000 Net loss from Hurricane (net of 4,500 taxes) (10,500) Net Income $10,500 Table 2 shows the GAAP Income Statement for the case. Students must covert this GAAP statement to an IFRS Statement