Answered step by step

Verified Expert Solution

Question

1 Approved Answer

prepare, in proper form, an adjusted income statement for 2021 [The following information applies to the questions displayed below.] Dyer, Incorporated, completed its first year

prepare, in proper form, an adjusted income statement for 2021

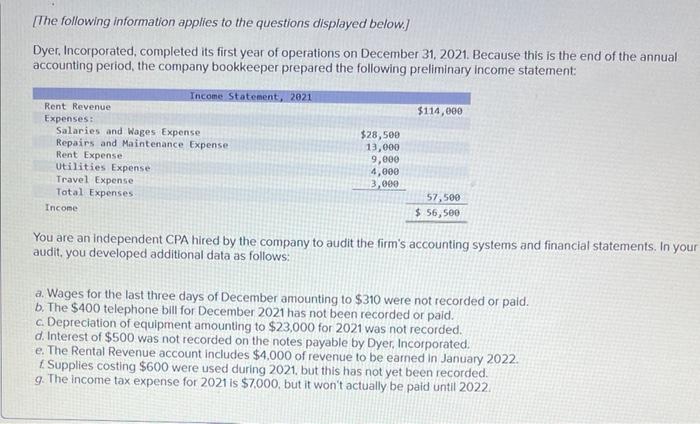

[The following information applies to the questions displayed below.] Dyer, Incorporated, completed its first year of operations on December 31, 2021. Because this is the end of the annual accounting period, the company bookkeeper prepared the following preliminary income statement: You are an independent CPA hired by the company to audit the firm's accounting systems and financial statements. In your audit, you developed additional data as follows: a. Wages for the last three days of December amounting to $310 were not recorded or paid. b. The $400 telephone bill for December 2021 has not been recorded or paid. c. Depreciation of equipment amounting to $23,000 for 2021 was not recorded. d. Interest of $500 was not recorded on the notes payable by Dyer. Incorporated. e. The Rental Revenue account includes $4,000 of revenue to be earned in January 2022 . f Supplies costing $600 were used during 2021, but this has not yet been recorded. g. The income tax expense for 2021 is $7.000. but it won't actually be paid until 2022 2. Prepare, in proper form, an adjusted income statement for 2021 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Accounting Principles

Authors: John J. Wild, Ken W. Shaw, Barbara Chiappetta

20th Edition

1259157148, 78110874, 9780077616212, 978-1259157141, 77616219, 978-0078110870