Answered step by step

Verified Expert Solution

Question

1 Approved Answer

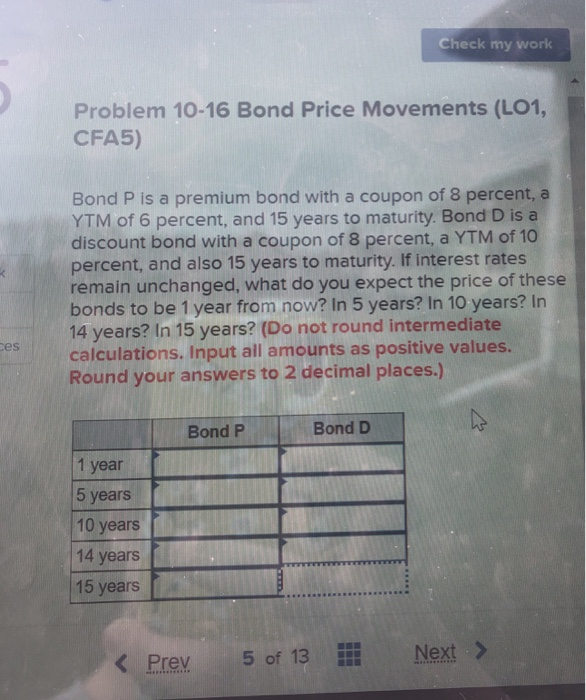

Problem 10-16 Bond Price Movements (LO1, CFA5) Check my work Problem 10-16 Bond Price Movements (LO1, CFA5) Bond P is a premium bond with a

Problem 10-16 Bond Price Movements (LO1, CFA5)

Check my work Problem 10-16 Bond Price Movements (LO1, CFA5) Bond P is a premium bond with a coupon of 8 percent, a YTM of 6 percent, and 15 years to maturity. Bond D is a discount bond with a coupon of 8 percent, a YTM of 10 percent, and also 15 years to maturity. If interest rates remain unchanged, what do you expect the price of these bonds to be 1 year from now? In 5 years? In 10 years? In 14 years? In 15 years? (Do not round intermediate calculations. Input all amounts as positive values. Round your answers to 2 decimal places.) ces Bond P Bond D 1 year 5 years 10 years 14 years 15 years Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Liberalization And The Reconstruction Of State Market Relations

Authors: Robert B. Packer

1st Edition

1138488518, 978-1138488519