Answered step by step

Verified Expert Solution

Question

1 Approved Answer

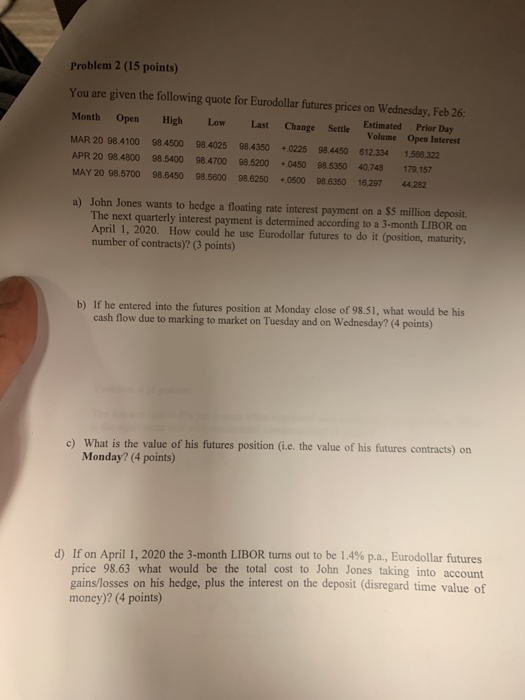

Problem 2 (15 points) You are given the following quote for Eurodollar futures prices on Wednesday, Feb 26: Month Open H igh Low Last Change

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The World Is Your Oyster The Guide To Finding Great Investments Around The Globe

Authors: Jeff D. Opdyke

1st Edition

0307381048, 978-0307381040