Answered step by step

Verified Expert Solution

Question

1 Approved Answer

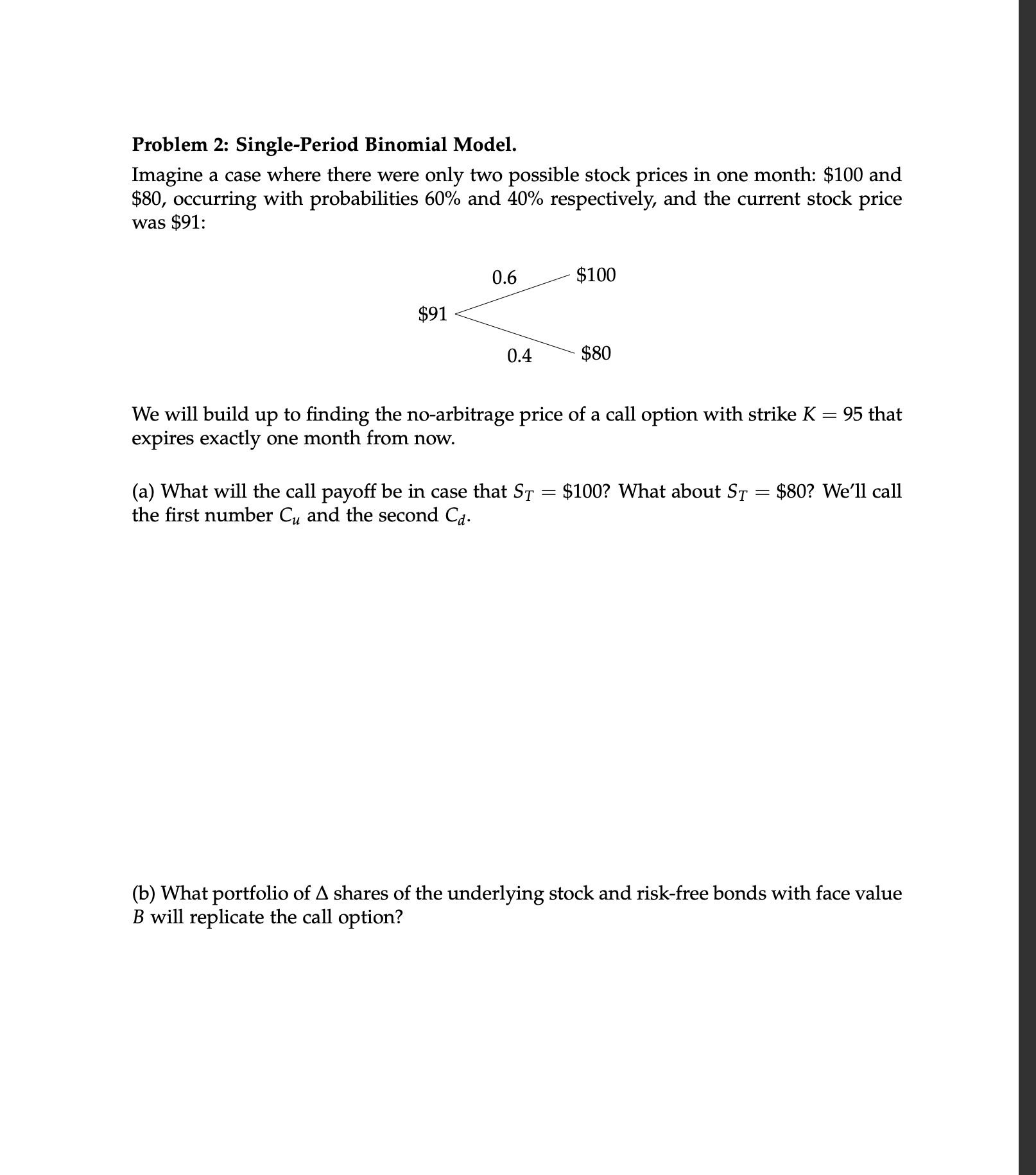

Problem 2: Single-Period Binomial Model. Imagine a case where there were only two possible stock prices in one month: $100 and $80, occurring with probabilities

Problem 2: Single-Period Binomial Model. Imagine a case where there were only two possible stock prices in one month: $100 and $80, occurring with probabilities 60% and 40% respectively, and the current stock price was $91 : We will build up to finding the no-arbitrage price of a call option with strike K=95 that expires exactly one month from now. (a) What will the call payoff be in case that ST=$100 ? What about ST=$80 ? We'll call the first number Cu and the second Cd. (b) What portfolio of shares of the underlying stock and risk-free bonds with face value B will replicate the call option? (c) What is the no-arbitrage price of the call option, assuming the continuously compounded risk-free rate is 2% annually? (d) What are the risk-neutral probabilities of the two states? Price the call with riskneutral pricing

Problem 2: Single-Period Binomial Model. Imagine a case where there were only two possible stock prices in one month: $100 and $80, occurring with probabilities 60% and 40% respectively, and the current stock price was $91 : We will build up to finding the no-arbitrage price of a call option with strike K=95 that expires exactly one month from now. (a) What will the call payoff be in case that ST=$100 ? What about ST=$80 ? We'll call the first number Cu and the second Cd. (b) What portfolio of shares of the underlying stock and risk-free bonds with face value B will replicate the call option? (c) What is the no-arbitrage price of the call option, assuming the continuously compounded risk-free rate is 2% annually? (d) What are the risk-neutral probabilities of the two states? Price the call with riskneutral pricing Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Blockchain Developer A Practical Guide For Designing Implementing Publishing Testing And Securing Distributed Blockchain Based Projects

Authors: Elad Elrom

1st Edition

1484248465, 978-1484248461