Answered step by step

Verified Expert Solution

Question

1 Approved Answer

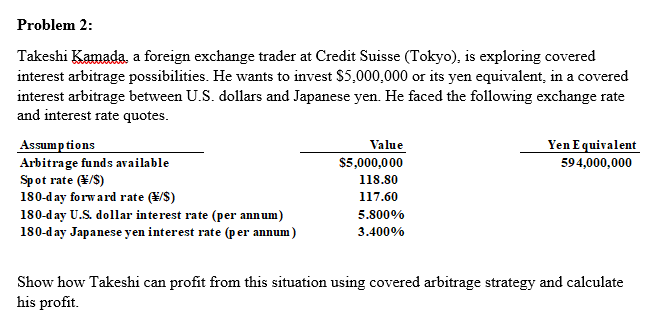

Problem 2: Takeshi Kamada, a foreign exchange trader at Credit Suisse (Tokyo), is exploring covered interest arbitrage possibilities. He wants to invest $5,000,000 or its

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Business Mathematics with Canadian Applications

Authors: S. A. Hummelbrunner, Kelly Halliday, K. Suzanne Coombs

10th edition

133052311, 978-0133052312