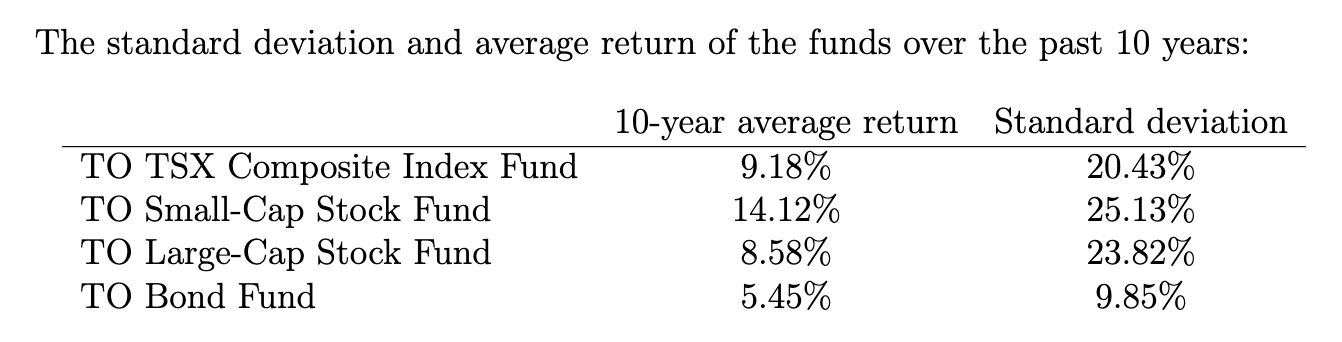

Problem 2 You are discussing your retirement plan with Emma Li when she mentions that Maureen O'Brien, a representative from Toronto Financial Services, is visiting your office today. You decide that you should meet with Maureen, so Emma sets up an appointment for you later in the day. When you sit down with Maureen, she discusses the various investment options available in the company's retirement plan. You mention to Maureen that you researched your new employer before you accepted your new job. Analysis of the company has led to your belief that the company is growing and will achieve a grater market share in the future. You also feel you should support your employer. Given these considerations, along with the fact that you are a conservative investor, you are leaning toward investing 100% of your retirement amount in the company you now work for. Assume the risk-free rate is the historical average T-Bill rate of 3.4%. The correlation between the TO Large-Cap Stock Fund and the TO Bond Fund is 0.1. Note that the spreadsheet graphing and Solver in Excel may assist you in answering the questions. The standard deviation and average return of the funds over the past 10 years: TO TSX Composite Index Fund TO Small-Cap Stock Fund TO Large-Cap Stock Fund TO Bond Fund 10-year average return Standard deviation 9.18% 20.43% 14.12% 25.13% 8.58% 23.82% 5.45% 9.85% 5. Compute an efficient portfolio of both risky funds and a risk-free asset that would be preferred by an investor that has a low volatility (risk) target of o(Rp) = 5%. What is the optimal portfolio for this investor? What about a more risk tolerant investor who has a high expected return target of E(Rp) = 12%. What is the optimal portfolio for this other investor? Report the composition, the expected return, and the volatility of these two portfolios. Comment on the ratio of investment in the TO Large-Cap Stock Fund and the TO Bond Fund for both investors. (2 points) = 6. Would some other investors who are considering investing in the TO Large-Cap Stock Fund, the TO Bond Fund, and the risk-free asset find it efficient to short sell only one of the two risky funds? Explain. (1 point) Problem 2 You are discussing your retirement plan with Emma Li when she mentions that Maureen O'Brien, a representative from Toronto Financial Services, is visiting your office today. You decide that you should meet with Maureen, so Emma sets up an appointment for you later in the day. When you sit down with Maureen, she discusses the various investment options available in the company's retirement plan. You mention to Maureen that you researched your new employer before you accepted your new job. Analysis of the company has led to your belief that the company is growing and will achieve a grater market share in the future. You also feel you should support your employer. Given these considerations, along with the fact that you are a conservative investor, you are leaning toward investing 100% of your retirement amount in the company you now work for. Assume the risk-free rate is the historical average T-Bill rate of 3.4%. The correlation between the TO Large-Cap Stock Fund and the TO Bond Fund is 0.1. Note that the spreadsheet graphing and Solver in Excel may assist you in answering the questions. The standard deviation and average return of the funds over the past 10 years: TO TSX Composite Index Fund TO Small-Cap Stock Fund TO Large-Cap Stock Fund TO Bond Fund 10-year average return Standard deviation 9.18% 20.43% 14.12% 25.13% 8.58% 23.82% 5.45% 9.85% 5. Compute an efficient portfolio of both risky funds and a risk-free asset that would be preferred by an investor that has a low volatility (risk) target of o(Rp) = 5%. What is the optimal portfolio for this investor? What about a more risk tolerant investor who has a high expected return target of E(Rp) = 12%. What is the optimal portfolio for this other investor? Report the composition, the expected return, and the volatility of these two portfolios. Comment on the ratio of investment in the TO Large-Cap Stock Fund and the TO Bond Fund for both investors. (2 points) = 6. Would some other investors who are considering investing in the TO Large-Cap Stock Fund, the TO Bond Fund, and the risk-free asset find it efficient to short sell only one of the two risky funds? Explain. (1 point)