Answered step by step

Verified Expert Solution

Question

1 Approved Answer

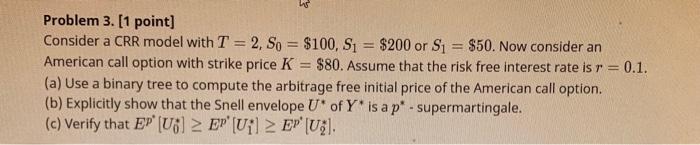

Problem 3. [1 point] Consider a CRR model with T=2,S0=$100,S1=$200 or S1=$50. Now consider an American call option with strike price K=$80. Assume that the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Credit A CFOs Guide To Bank Debt And Loan Agreements

Authors: Susan C. Alker

1st Edition

B089M2DG8V, 979-8649897921