Answered step by step

Verified Expert Solution

Question

1 Approved Answer

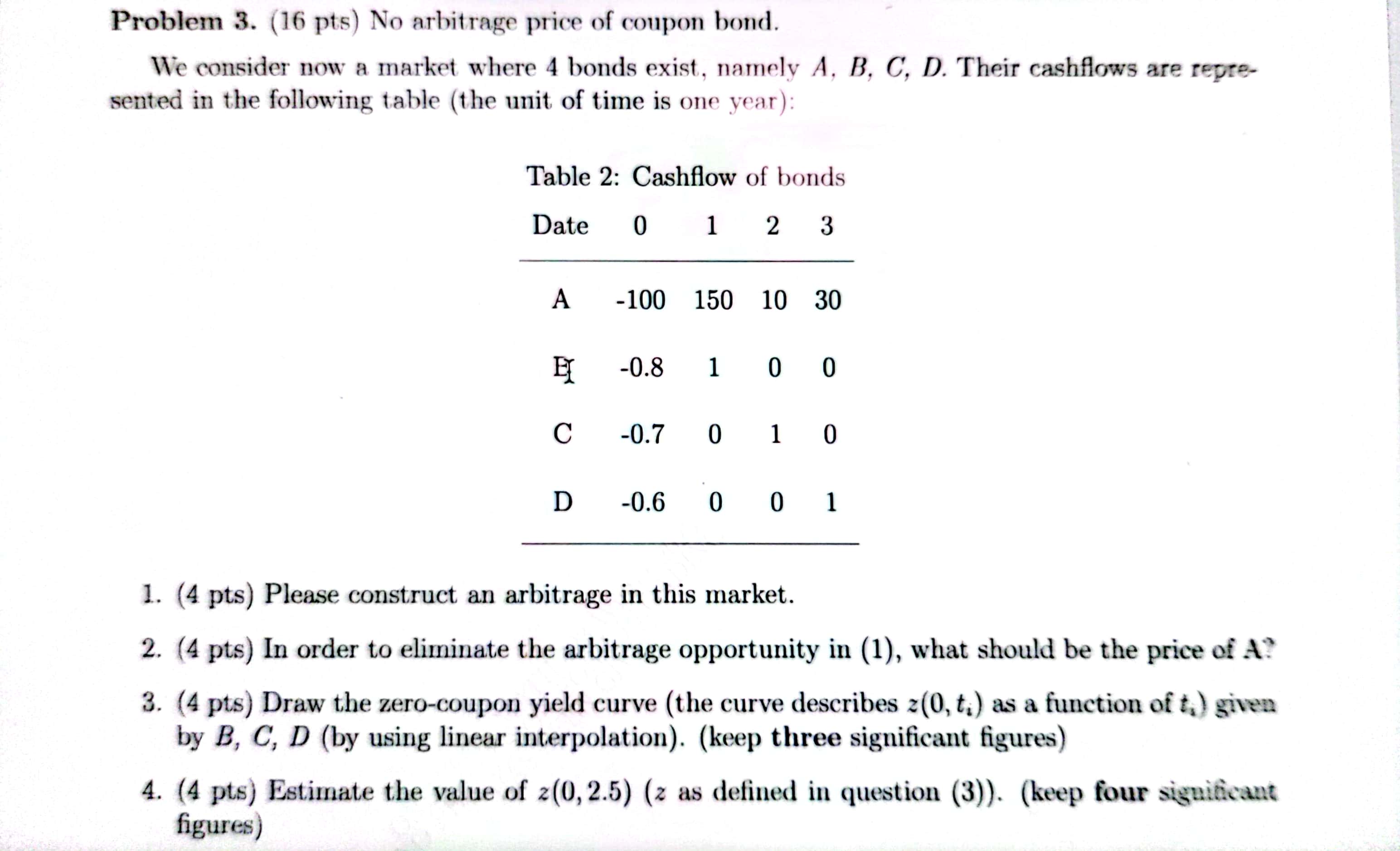

Problem 3. (16 pts) No arbitrage price of coupon bond. We consider now a market where 4 bonds exist, namely A, B, C, D.

Problem 3. (16 pts) No arbitrage price of coupon bond. We consider now a market where 4 bonds exist, namely A, B, C, D. Their cashflows are repre- sented in the following table (the unit of time is one year): Table 2: Cashflow of bonds Date 0 1 2 3 A -100 150 10 30 EX -0.8 100 C -0.7 0 10 D -0.6001 1. (4 pts) Please construct an arbitrage in this market. 2. (4 pts) In order to eliminate the arbitrage opportunity in (1), what should be the price of A? 3. (4 pts) Draw the zero-coupon yield curve (the curve describes z(0, t.) as a function of t) given by B, C, D (by using linear interpolation). (keep three significant figures) 4. (4 pts) Estimate the value of 2(0,2.5) (z as defined in question (3)). (keep four significant figures)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Lets address each part of the problem step by step Part 1 Construct Arbitrage To construct an arbitrage we need to find a combination of these bonds t...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Financial Planning For Executives And Entrepreneurs

Authors: Michael J. Nathanson, Jeffrey T. Craig, Jennifer A. Geoghegan, Nadine Gordon Lee, Michael A. Haber, Seth P. Hieken, Matthew C. Ilteris, D. Scott McDonald, Joseph A. Salvati, Stephen R. Stelljes

1st Edition

3030405273, 978-3030405274