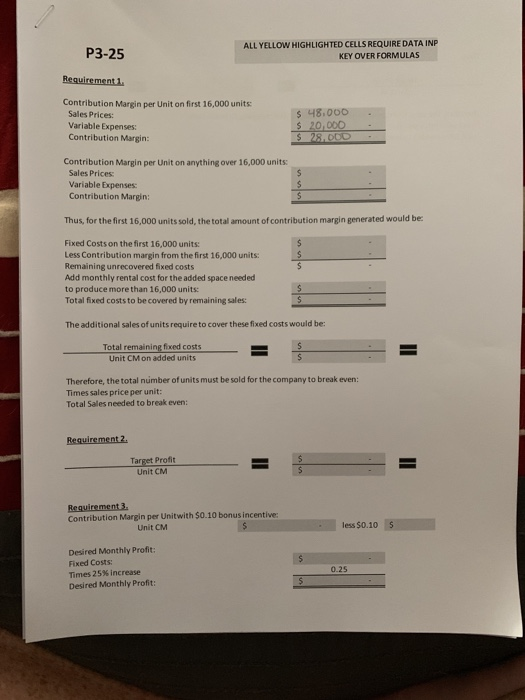

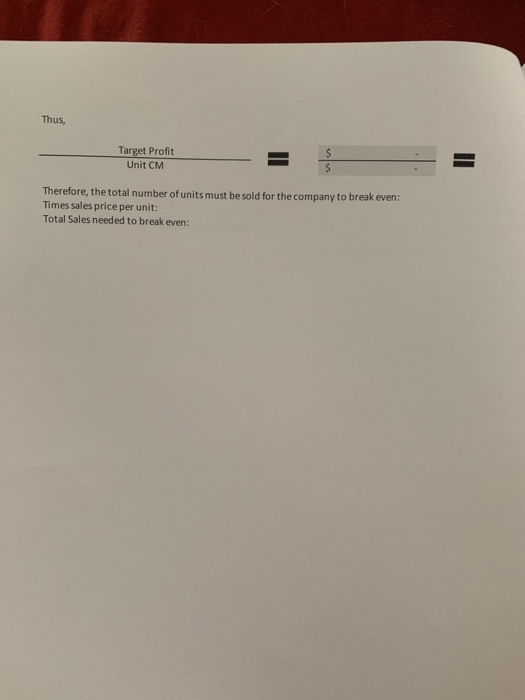

PROBLEM 3-25 Changes in Fixed and Variable Expenses; Break-Even and Target Profit Analysis [LO3-4, LO3-5, LO3-6] Neptune Company produces toys and other items for use in beach and resort areas. A small, inflat- able toy has come onto the market that the company is anxious to produce and sell. The new toy will sell for $3 per unit. Enough capacity exists in the company's plant to produce 16,000 units of the toy each month. Variable expenses to manufacture and sell one unit would be $1.25, and fixed expenses associated with the toy would total $35,000 per month. The company's Marketing Department predicts that demand for the new toy will exceed the 16,000 units that the company is able to produce. Additional manufacturing space can be rented from another company at a fixed expense of $1,000 per month. Variable expenses in the rented facility would total $1.40 per unit, due to somewhat less efficient operations than in the main plant. Chapter 3 Required: 1. Compute the monthly break-even point for the new toy in unit sales and in dollar sales. 2. How many units must be sold each month to make a monthly profit of $12,000? 3. If the sales manager receives a bonus of 10 cents for each unit sold in excess of the break-even point, how many units must be sold each month to earn a return of 25% on the monthly invest- ment in fixed expenses? P3-25 ALL YELLOW HIGHLIGHTED CELLS REQUIRE DATA INP KEY OVER FORMULAS Requirement1 Contribution Margin per Unit on first 16,000 units Sales Prices: Variable Expenses: Contribution Margin: $48.000 $ 20,000 $ 28, DOD - Contribution Margin per Unit on anything over 16,000 units: Sales Prices Variable Expenses Contribution Margin: Thus, for the first 16,000 units sold, the total amount of contribution margin generated would be Fixed Costs on the first 16,000 units: Less Contribution margin from the first 16,000 units: Remaining unrecovered fixed costs Add monthly rental cost for the added space needed to produce more than 16,000 units: Total fixed costs to be covered by remaining sales: The additional sales of units require to cover these fixed costs would be: Total remaining fixed costs Unit CM on added units Therefore, the total number of units must be sold for the company to break even: Times sales price per unit: Total Sales needed to break even: Requirement 2. Target Profit Unit CM Requirement 3. Contribution Margin per Unitwith $0.10 bonus incentive: Unit CM less $0.10 5 Desired Monthly Profit: Fixed Costs: Times 25% increase Desired Monthly Profit: Thus, Target Profit Unit CM Therefore, the total number of units must be sold for the company to break even: Times sales price per unit: Total Sales needed to break even