Answered step by step

Verified Expert Solution

Question

1 Approved Answer

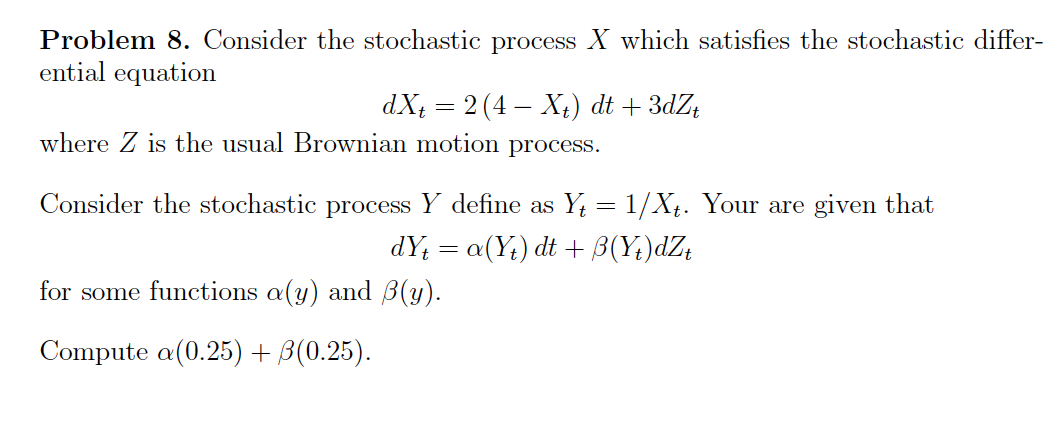

Problem 8. Consider the stochastic process X which satisfies the stochastic differ- ential equation dxt = 2(4-Xt) dt + 3dZt == where Z is

Problem 8. Consider the stochastic process X which satisfies the stochastic differ- ential equation dxt = 2(4-Xt) dt + 3dZt == where Z is the usual Brownian motion process. Consider the stochastic process Y define as Y = 1/Xt. Your are given that dYa(Y) dt + (Yt)dZt for some functions a(y) and (y). Compute a(0.25) + (0.25).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Stochastic Finance With Market Examples

Authors: Nicolas Privault

2nd Edition

1032288272, 9781032288277