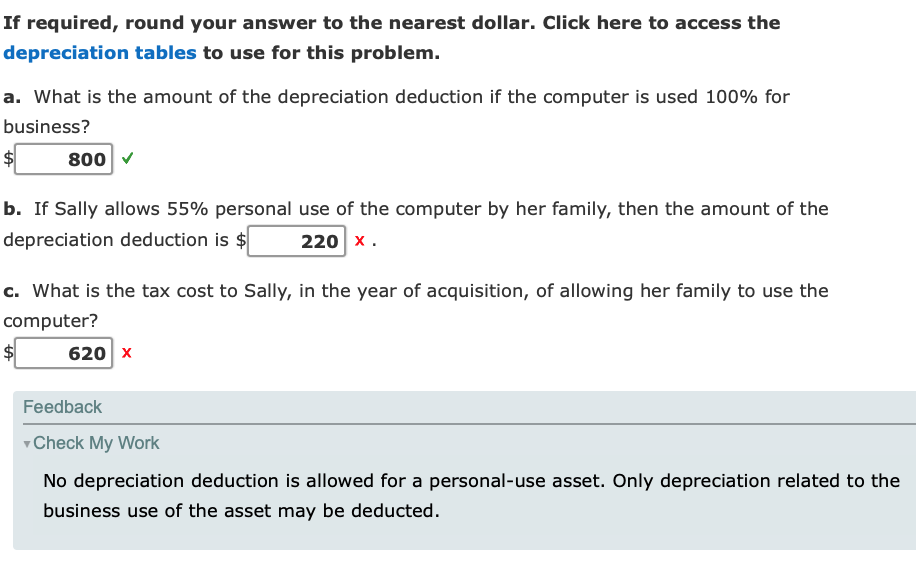

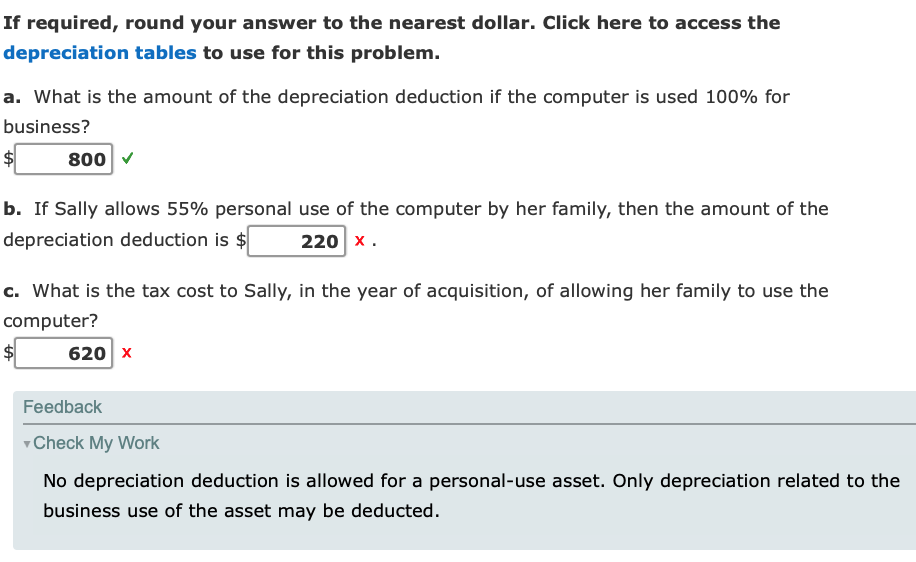

Problem 8-45 (LO. 2, 4, 9)

Sally purchased a new computer (5-year property) on June 1, 2020, for $4,000. Sally could use the computer 100% of the time in her business, or she could allow her family to use the computer as well. Sally estimates that if her family uses the computer, the business use will be 45% and the personal use will be 55%.

Determine the tax cost to Sally, in the year of acquisition, of allowing her family to use the computer. Assume that Sally would not elect 179 immediate expensing and that her marginal income tax rate is 32%. She does not claim any available additional first-year depreciation.

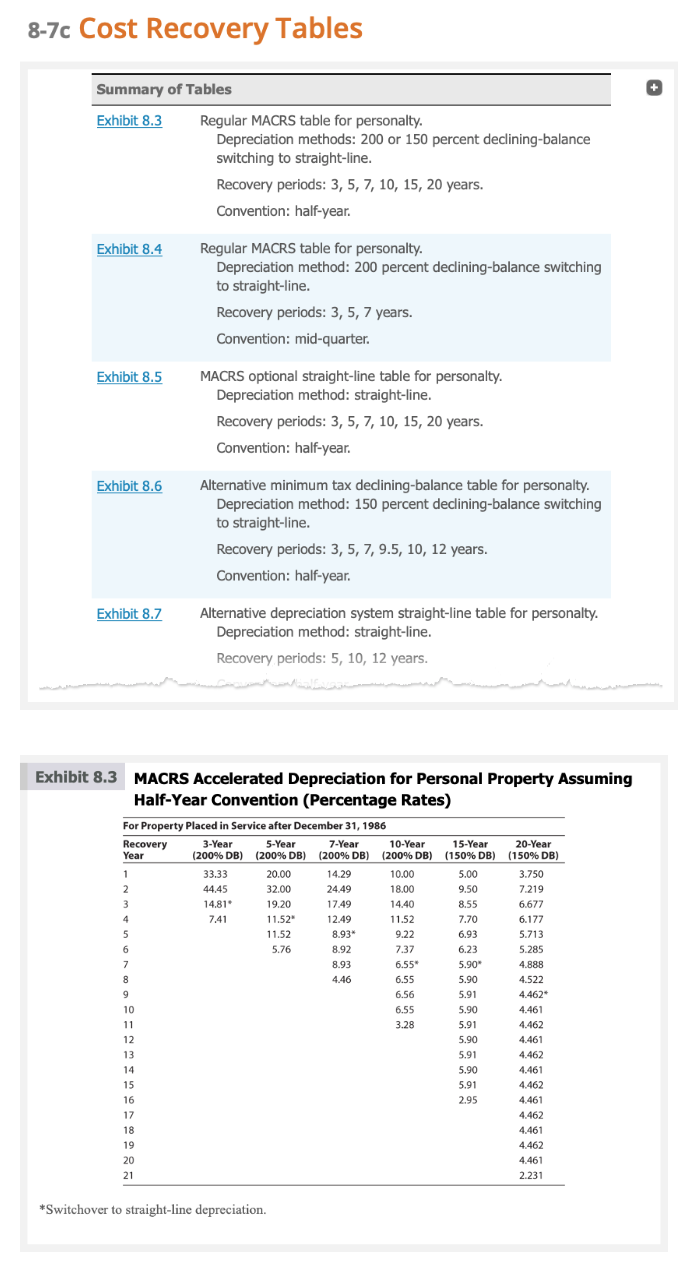

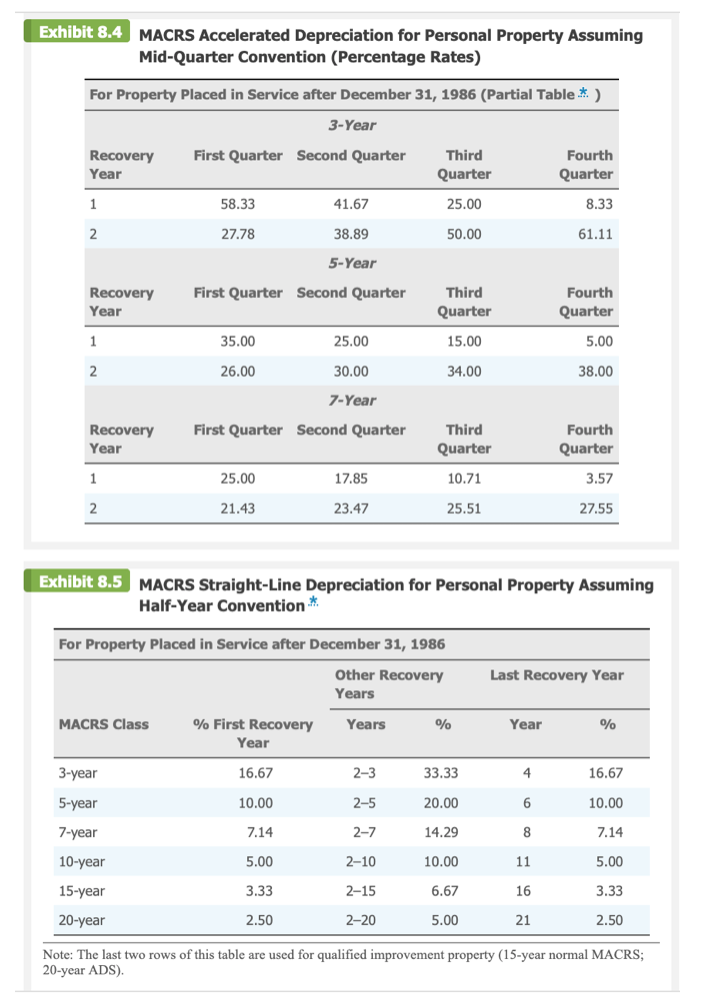

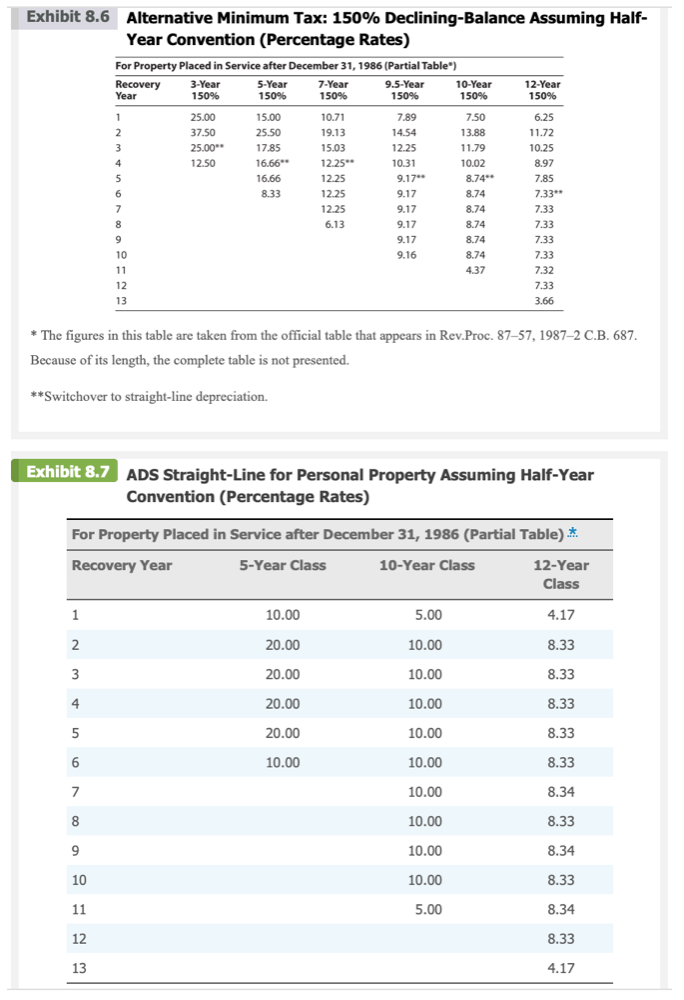

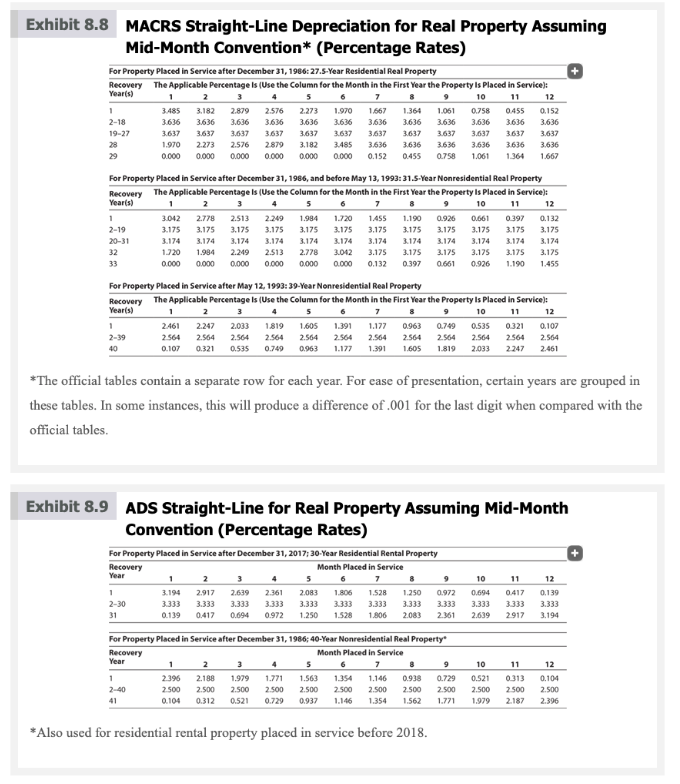

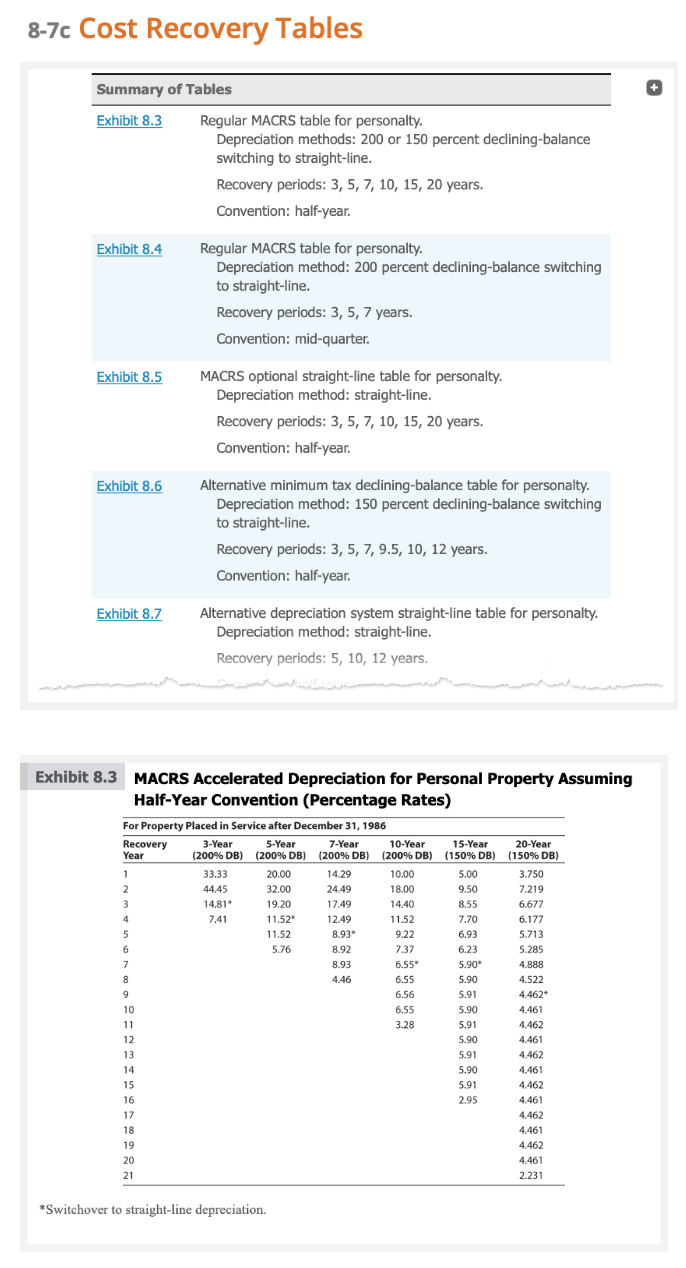

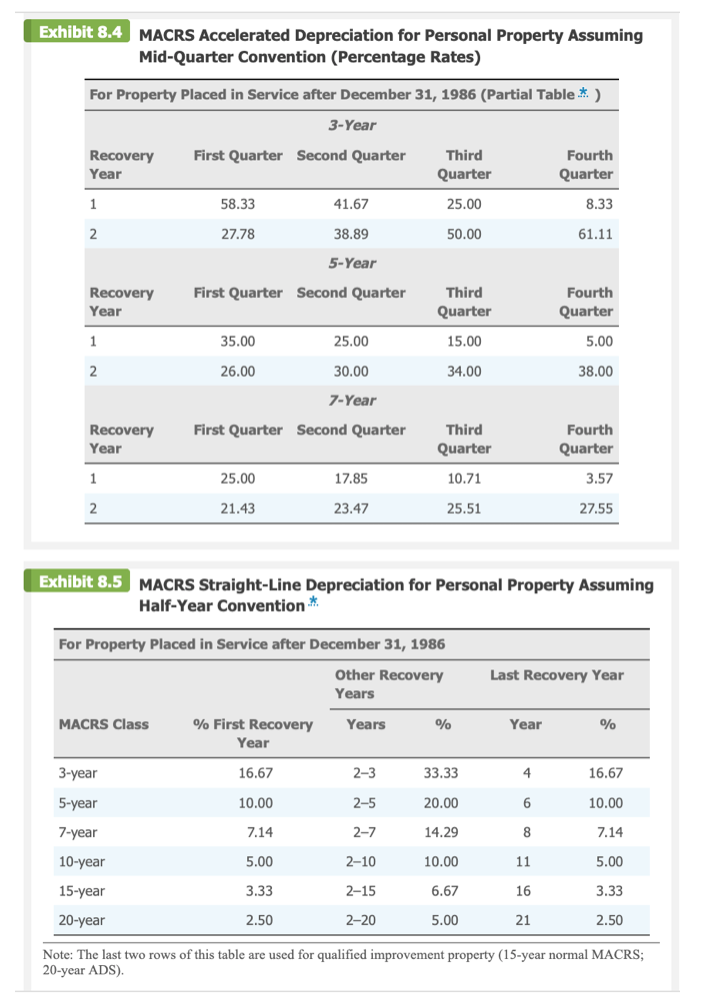

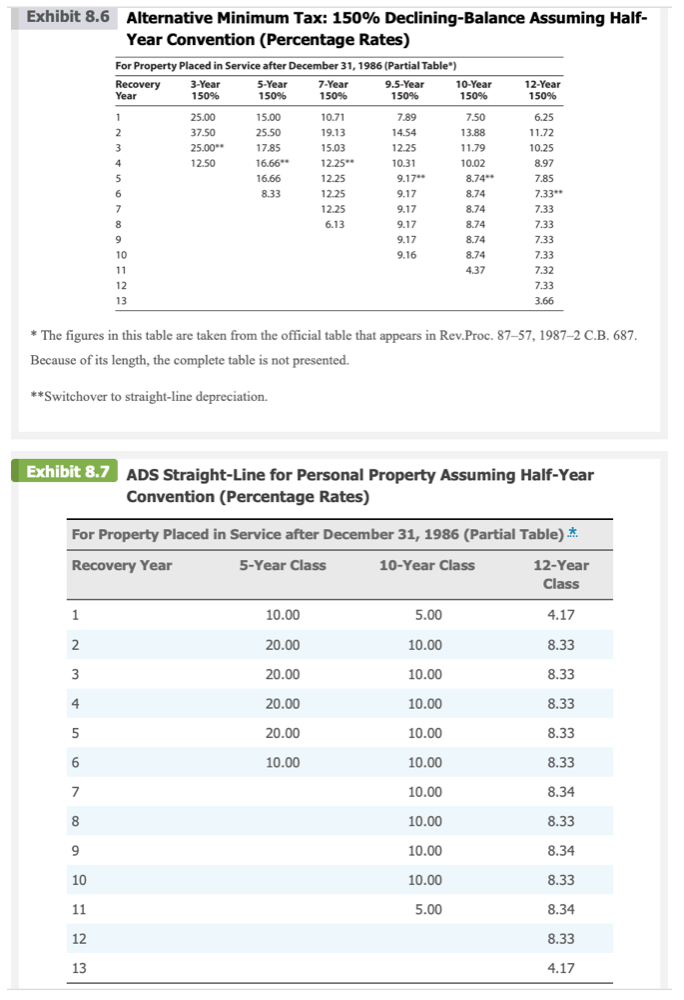

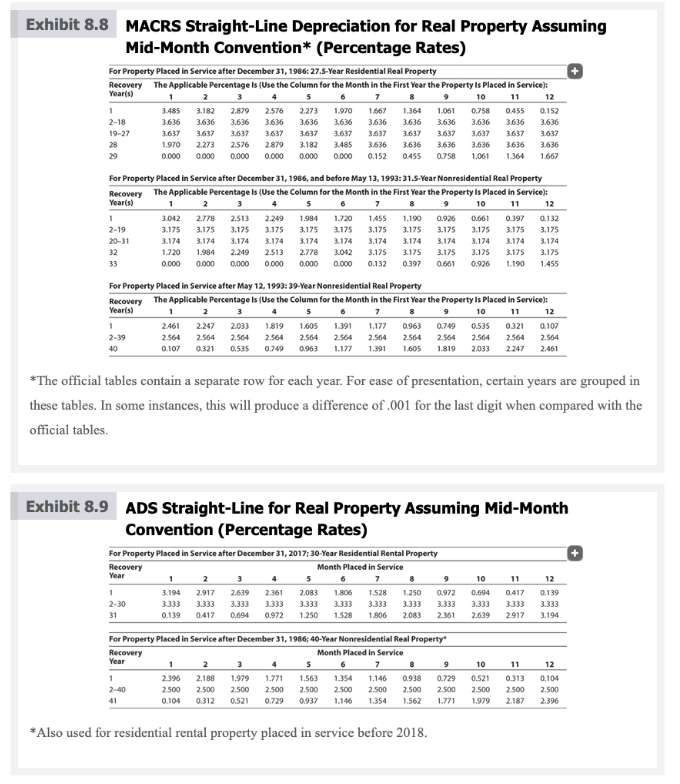

8-7c Cost Recovery Tables Summary of Tables + Exhibit 8.3 Regular MACRS table for personalty. Depreciation methods: 200 or 150 percent declining-balance switching to straight-line. Recovery periods: 3, 5, 7, 10, 15, 20 years. Convention: half-year. Exhibit 8.4 Regular MACRS table for personalty. Depreciation method: 200 percent declining-balance switching to straight-line. Recovery periods: 3, 5, 7 years. Convention: mid-quarter. Exhibit 8.5 MACRS optional straight-line table for personalty. Depreciation method: straight-line. Recovery periods: 3, 5, 7, 10, 15, 20 years. Convention: half-year. Exhibit 8.6 Alternative minimum tax declining-balance table for personalty. Depreciation method: 150 percent declining-balance switching to straight-line. Recovery periods: 3, 5, 7, 9.5, 10, 12 years. Convention: half-year. Exhibit 8.7 Alternative depreciation system straight-line table for personalty. Depreciation method: straight-line. Recovery periods: 5, 10, 12 years. Exhibit 8.3 MACRS Accelerated Depreciation for Personal Property Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 Recovery 3-Year 5-Year 7-Year 10-Year 15-Year 20-Year Year (200% DB) (200% DB) (200% DB) (200% DB) (150% DB) (150% DB) 33.33 20.00 14.29 10.00 5.00 3.750 44.45 32.00 24.49 18.0 9.50 7.219 14.81 19.20 17.49 14.40 8.55 6.67 7.41 11.52" 12.49 11.52 7.70 6.177 11.52 8.93* 9.22 6.93 5.713 5.76 8.92 7.37 6.23 5.285 8.93 6.55* 5.90* 4.888 4.46 6.55 5.90 4.522 5.56 5.91 4.462* 6.55 5.90 4.461 3.28 5.91 4.462 5.90 4.461 5.91 4.462 5.90 4.461 5.91 4.462 2.95 4.461 17 4.462 18 4.461 19 4.462 20 4.461 21 2.231 *Switchover to straight-line depreciation.Exhibit 8.4 MACRS Accelerated Depreciation for Personal Property Assuming Mid-Quarter Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 (Partial Table # ) 3-Year Recovery First Quarter Second Quarter Third Fourth Year Quarter Quarter 1 58.33 41.67 25.00 8.33 27.78 38.89 50.00 61.11 5-Year Recovery First Quarter Second Quarter Third Fourth Year Quarter Quarter 1 35.00 25.00 15.00 5.00 2 26.00 30.00 34.00 38.00 7-Year Recovery First Quarter Second Quarter Third Fourth Year Quarter Quarter 25.00 17.85 10.71 3.57 21.43 23.47 25.51 27.55 Exhibit 8.5 MACRS Straight-Line Depreciation for Personal Property Assuming Half-Year Convention* For Property Placed in Service after December 31, 1986 Other Recovery Last Recovery Year Years MACRS Class % First Recovery Years Year % Year 3-year 16.67 2-3 33.33 4 16.67 5-year 10.00 2-5 20.00 10.00 7-year 7.14 2-7 14.29 8 7.14 10-year 5.00 2-10 10.00 11 5.00 15-year 3.33 2-15 6.67 16 3.33 20-year 2.50 2-20 5.00 21 2.50 20-year ADS). Note: The last two rows of this table are used for qualified improvement property (15-year normal MACRS;Exhibit 8.6 Alternative Minimum Tax: 150% Declining-Balance Assuming Half- Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 (Partial Table") Recovery 3-Year 5-Year 7-Year 9.5-Year 10-Year 12-Year Year 150% 150% 150% 150% 150% 150% 25.00 15.00 10.71 7.89 7.50 5.25 37.50 25.50 19.13 14.54 13.88 11.72 25.00** 17.85 15.03 12.25 11.79 10.25 12.50 16.66"* 12.25"- 10.31 10.02 8.97 16.66 12.25 9.17" 8.74" 7.85 8.33 12.25 9.17 8.74 7.33*# 12.25 9.17 8.74 7.33 6.13 9.17 8.74 7.33 9.17 8.74 7.33 10 9.16 8.74 7.33 11 437 7.32 12 7.33 13 3.66 * The figures in this table are taken from the official table that appears in Rev.Proc. 87-57, 1987-2 C.B. 687. Because of its length, the complete table is not presented. **Switchover to straight-line depreciation. Exhibit 8.7 ADS Straight-Line for Personal Property Assuming Half-Year Convention (Percentage Rates) For Property Placed in Service after December 31, 1986 (Partial Table) * Recovery Year 5-Year Class 10-Year Class 12-Year Class 10.00 5.00 4.17 N 20.00 10.00 8.33 W 20.00 10.00 8.33 20.00 10.00 8.33 20.00 10.00 8.33 10.00 10.00 8.33 10.00 8.34 10.00 8.33 10.00 8.34 10 10.00 8.33 11 5.00 8.34 12 8.33 13 4.17Exhibit 8.8 MACRS Straight-Line Depreciation for Real Property Assuming Mid-Month Convention* (Percentage Rates) For Property Placed in Service after December 31, 1986: 27.5-Year Residential Real Property Recovery The Applicable Percentage Is (Use the Column for the Month in the First Year the Property Is Placed in Service]: Year(s) 10 13 3.485 3.182 2.879 2.576 2.273 1.970 1.667 1.364 1.061 0.758 0455 0.15 2-18 3.636 3.636 3.636 3.636 3.636 3.636 3.636 3.636 3.636 3.636 3636 3.636 19-27 3.637 3.637 3.637 3.637 3.637 3.637 3.637 3.63 3.637 3.637 1637 3.635 .970 2.273 2.576 2 879 3.182 3.485 3.636 3.636 3.636 3.636 3636 3.630 5.00 0.000 0.000 0.090 0.00 0.000 0.152 0.45 0.758 1.061 1.364 1.667 For Property Placed in Service after December 31, 1986, and before May 13, 1993: 31.5-Year Nonresidential Real Property Recovery The Applicable Percentage Is (Use the Column for the Month in the First Year the Property Is Placed in Service]: Yearis 12 3.042 2.778 2.513 2.249 1.984 1.720 1.455 1.190 0.920 0.641 0 397 0.132 2-19 3.175 3.175 3.175 3.175 3.175 3.175 3.175 3.175 3.175 3.175 3.175 3.175 20-31 3.174 3.174 3.174 3.174 3.174 3.174 3174 3.174 3.174 3.174 32 1.J20 1.984 2.249 2.513 2.778 3.042 3.175 3.175 4175 3.175 3175 3.175 0.000 0.133 0.30 01926 1.190 1.455 For Property Placed in Service after May 12, 1993: 39-Year Nonresidential Real Property Recovery The Applicable Percentage Is (Use the Column for the Month in the First Year the Property Is Placed in Service): Year(s) 12 2461 2.247 2.083 1.819 1.605 1.391 1.177 0.963 0.749 0.535 0 321 0.107 2-39 256 2.564 2.564 2.564 2.564 2.564 2.564 2.564 2.564 2.564 2564 2.564 0.107 0.321 0.535 0.740 0.963 1.177 1.301 1.605 1.819 2.033 2347 2.461 *The official tables contain a separate row for each year. For case of presentation, certain years are grouped in these tables. In some instances, this will produce a difference of .001 for the last digit when compared with the official tables. Exhibit 8.9 ADS Straight-Line for Real Property Assuming Mid-Month Convention (Percentage Rates) For Property Placed in Service after December 31, 2017: 30-Year Residential Rental Property + Recovery Month Placed in Service Year 10 11 12 3.194 2.917 2.639 2.361 2.083 1.806 1.528 1.250 0.972 0.694 0417 0.139 2-30 3.333 3.333 3.333 3.333 3.333 3.333 3.333 3.333 3.333 3.333 3.333 3.333 0.139 0.417 0.694 0.972 1.250 1.806 2043 2639 2917 3.194 For Property Placed in Service after December 31, 1986; 40-Year Nonresidential Real Property" Recovery Month Placed in Service Year 12 2 396 2.188 1.979 1.771 1.564 1354 1.146 0.94 0.729 0.521 0313 0.104 2-40 2.500 2.500 2.500 2.500 2.500 2.500 2.500 2.500 2.500 2.500 2.500 2.500 0.104 0.312 0.521 0.720 0,937 1.146 1.354 1.562 1.771 1.979 2.187 2.306 *Also used for residential rental property placed in service before 2018.If required, round your answer to the nearest dollar. Click here to access the depreciation tables to use for this problem. a. What is the amount of the depreciation deduction if the computer is used 100% for business? b. If Sally allows 55% personal use of the computer by her family, then the amount of the depreciation deduction is $- x . c. What is the tax cost to Sally, in the year of acquisition, of allowing her family to use the computer? .* Feedback v Check My Work No depreciation deduction is allowed for a personal-use asset. Only depreciation related to the business use of the asset may be deducted