Answered step by step

Verified Expert Solution

Question

1 Approved Answer

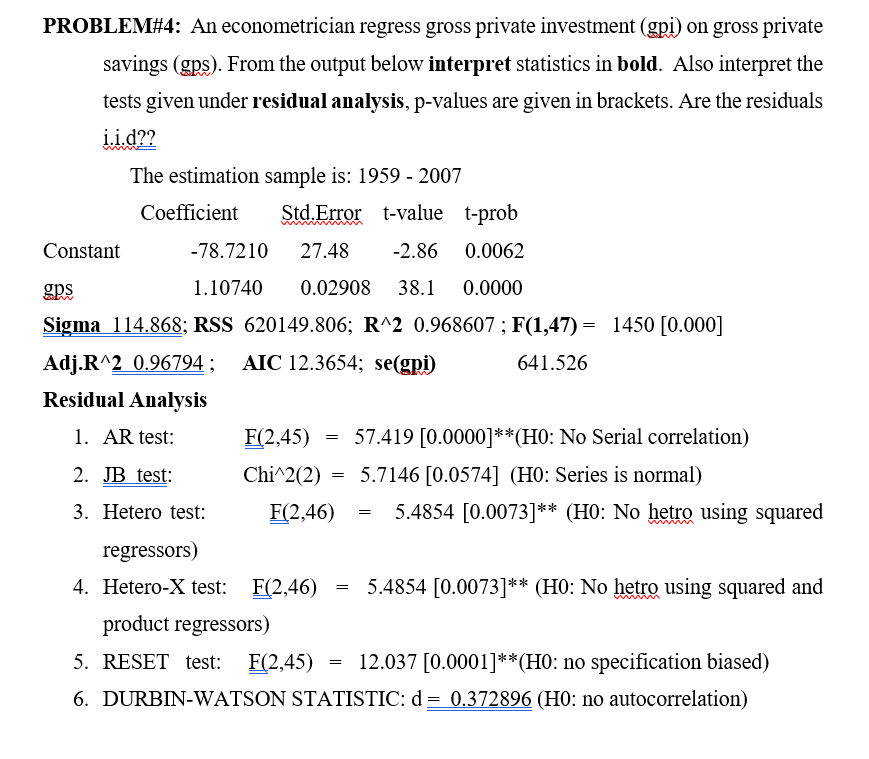

PROBLEM#4: An econometrician regress gross private investment (gpi) on gross private savings (gps). From the output below interpret statistics in bold. Also interpret the tests

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mastering Islamic Finance

Authors: Faizal Karbani

1st Edition

1292001445, 978-1292001449