Answered step by step

Verified Expert Solution

Question

1 Approved Answer

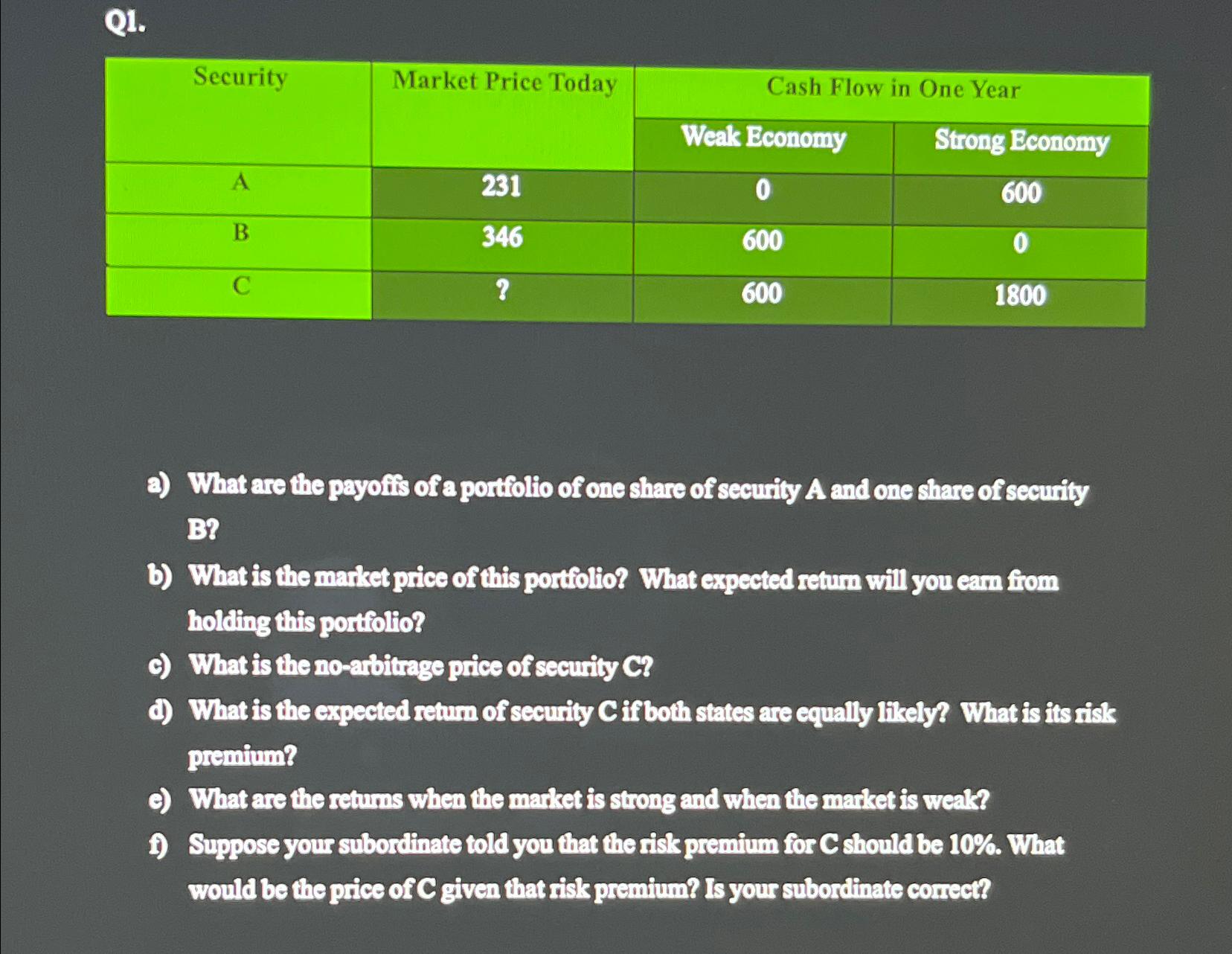

Q 1 . table [ [ Security , Market Price Today,Cash Flow in One Year ] , [ , Weak Economy,Strong Economy ] ,

Q

tableSecurityMarket Price Today,Cash Flow in One YearWeak Economy,Strong EconomyABC

a What are the payofis of a portiolio of one share of security A and one share of security B

b What is the market price of this portfolio? What expected retum will you cam from holding this portfolio?

c What is the noatbitrage price of security C

d What is the expected retum of security Cif both states are equally fikely? What is its riak premium?

What are the returns when the market is strong and when the market is weak?

if Suppose your subordinate told you that the risk premium for should be What would be the price of C given that risk premium? Is your subordinate correct?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The FinTech Book The Financial Technology Handbook For Investors Entrepreneurs And Visionaries

Authors: Susanne Chishti, Janos Barberis

1st Edition

111921887X, 9781119218876