Question

Q. 36 36. Zeus Ltd owns 100% of the issued capital of Ares Ltd. On 1 July 2015, Zeus Ltd purchased an item of equipment

Q. 36

36. Zeus Ltd owns 100% of the issued capital of Ares Ltd. On 1 July 2015, Zeus Ltd purchased an item of equipment from Ares Ltd for $800 000. Ares had owned the equipment for 2 years. It originally cost $890 000 and the accumulated depreciation was $178 000 at the time of sale. The equipment has been depreciated over this time, but not written down or revalued. The remaining useful life of the equipment at 1 July 2015 is estimated to be 8 years. Zeus Ltd expects the benefits to be obtained from the equipment to be evenly received over its useful life. The tax rate is 30%. What are the consolidation journal entries required for this inter-company transaction for the period ended 30 June 2016?

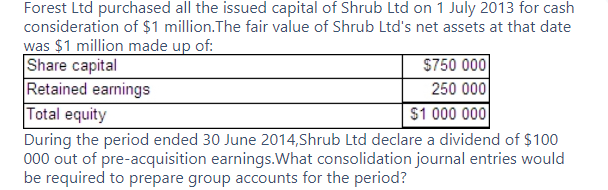

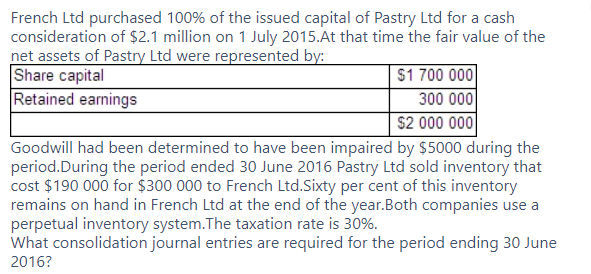

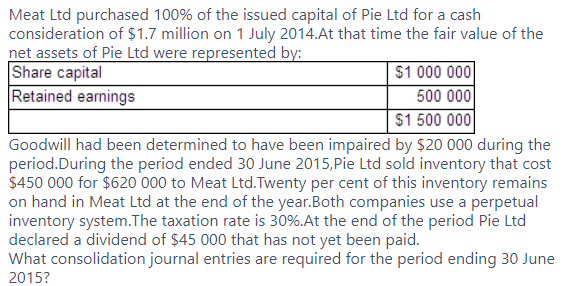

Forest Ltd purchased all the issued capital of Shrub Ltd on 1 July 2013 for cash consideration of $1 million. The fair value of Shrub Ltd's net assets at that date was $1 million made up of: Share capital $750 000 Retained earnings 250 000 Total equity $1 000 000 During the period ended 30 June 2014, Shrub Ltd declare a dividend of $100 000 out of pre-acquisition earnings. What consolidation journal entries would be required to prepare group accounts for the period? French Ltd purchased 100% of the issued capital of Pastry Ltd for a cash consideration of $2.1 million on 1 July 2015.At that time the fair value of the net assets of Pastry Ltd were represented by: Share capital $1 700 000 Retained earnings 300 000 $2 000 000 Goodwill had been determined to have been impaired by $5000 during the period.During the period ended 30 June 2016 Pastry Ltd sold inventory that cost $190 000 for $300 000 to French Ltd.Sixty per cent of this inventory remains on hand in French Ltd at the end of the year.Both companies use a perpetual inventory system. The taxation rate is 30%. What consolidation journal entries are required for the period ending 30 June 2016? Meat Ltd purchased 100% of the issued capital of Pie Ltd for a cash consideration of $1.7 million on 1 July 2014.At that time the fair value of the net assets of Pie Ltd were represented by: Share capital $1 000 000 Retained earnings 500 000 $1 500 000 Goodwill had been determined to have been impaired by $20 000 during the period.During the period ended 30 June 2015, Pie Ltd sold inventory that cost $450 000 for $620 000 to Meat Ltd. Twenty per cent of this inventory remains on hand in Meat Ltd at the end of the year.Both companies use a perpetual inventory system.The taxation rate is 30%.At the end of the period Pie Ltd declared a dividend of $45 000 that has not yet been paid. What consolidation journal entries are required for the period ending 30 June 2015Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Why CISOs Fail Security Audit And Leadership Series

Authors: Barak Engel

2nd Edition

1032299258, 978-1032299259