Answered step by step

Verified Expert Solution

Question

1 Approved Answer

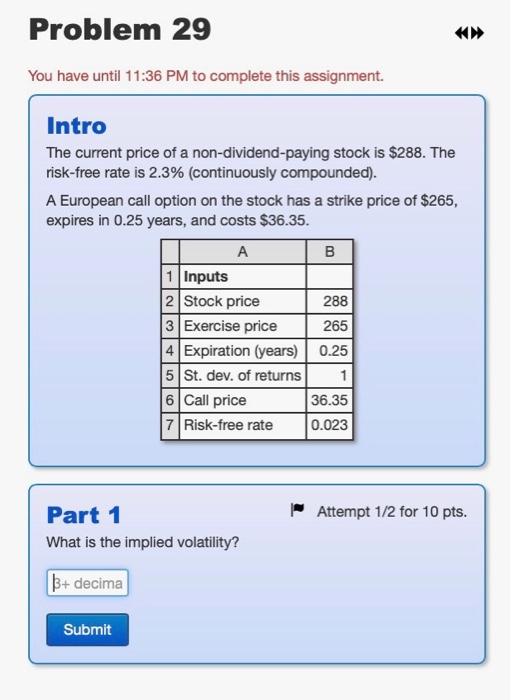

Q29. please show excel formulas. Problem 29 You have until 11:36 PM to complete this assignment. Intro The current price of a non-dividend-paying stock is

Q29. please show excel formulas.

Problem 29 You have until 11:36 PM to complete this assignment. Intro The current price of a non-dividend-paying stock is $288. The risk-free rate is 2.3% (continuously compounded). A European call option on the stock has a strike price of $265, expires in 0.25 years, and costs $36.35. A B 1 Inputs 2 Stock price 288 3 Exercise price 265 4 Expiration (years) 0.25 5 St. dev. of returns 1 6 Call price 36.35 7 Risk-free rate 0.023 Attempt 1/2 for 10 pts. Part 1 What is the implied volatility? b+ decima Submit Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial and Management Accounting

Authors: Pauline Weetman

7th edition

1292086599, 978-1292086590