Question

Q6. Given the following information, please find The optimal hedging ratio based on the S&P 500 index. The effectiveness of the hedging; The number of

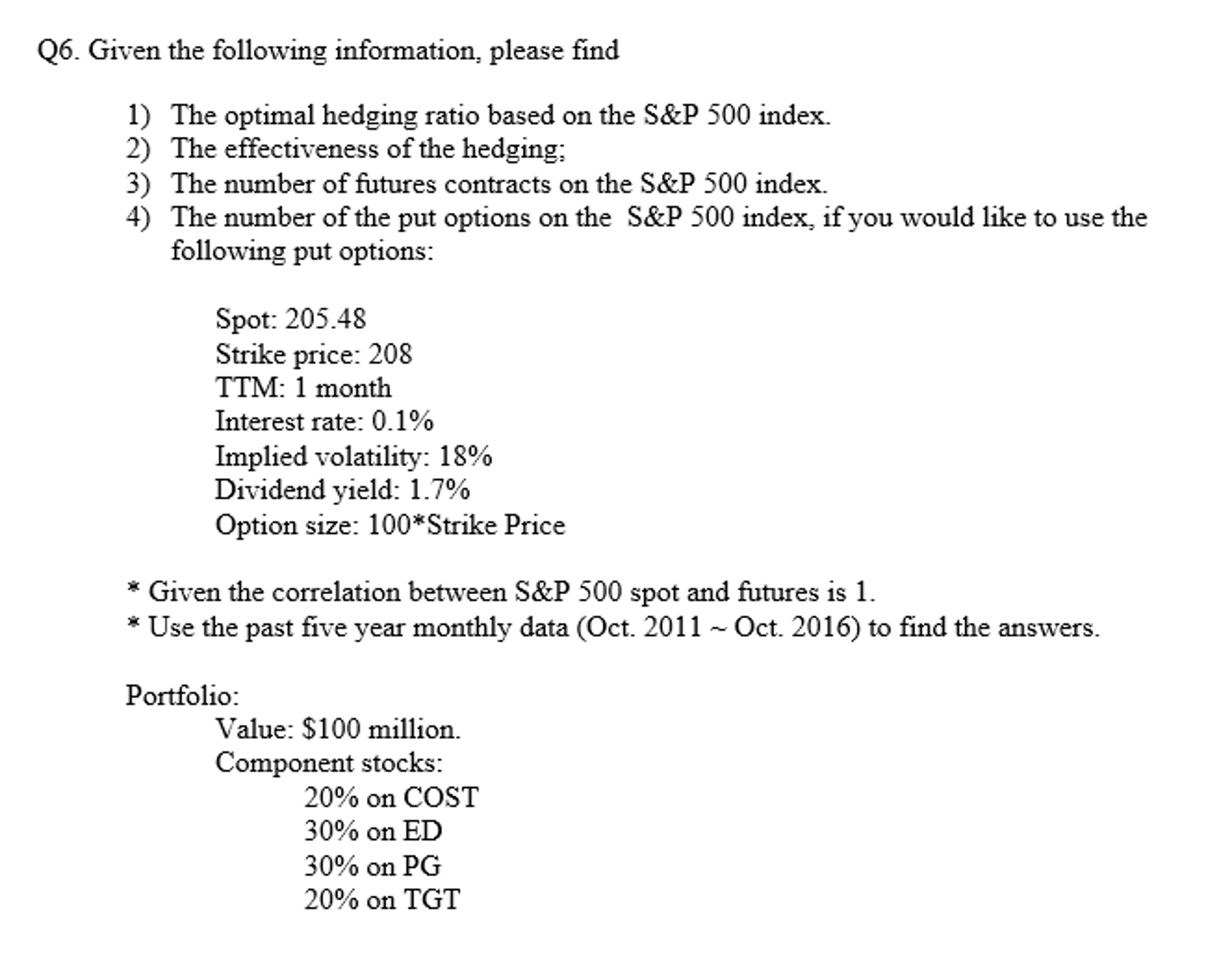

Q6. Given the following information, please find

The optimal hedging ratio based on the S&P 500 index.

The effectiveness of the hedging;

The number of futures contracts on the S&P 500 index.

The number of the put options on the S&P 500 index, if you would like to use the following put options:

Spot: 205.48

Strike price: 208

TTM: 1 month

Interest rate: 0.1%

Implied volatility: 18%

Dividend yield: 1.7%

Option size: 100*Strike Price

* Given the correlation between S&P 500 spot and futures is 1.

* Use the past five year monthly data (Oct. 2011 ~ Oct. 2016) to find the answers.

Portfolio:

Value: $100 million.

Component stocks:

20% on COST

30% on ED

30% on PG

20% on TGT

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Agricultural Finance

Authors: Charles Moss

1st Edition

0415599075, 978-0415599078